")

The housing market is increasingly split between extremes: equity-rich, all-cash buyers are at an all-time high, while cash-strapped first-time buyers are at a record low. Affordability challenges are keeping newcomers on the sidelines, while buyers with stronger finances continue to dominate, according to the National Association of REALTORS®’ newly released 2025 Profile of Home Buyers and Sellers report.

“Unfolding in the housing market is a tale of two cities,” says Jessica Lautz, NAR deputy chief economist and vice president of research. “We’re seeing buyers with significant housing equity making larger down payments and all-cash offers, while first-time buyers continue to struggle to enter the market.”

The dynamic is prompting the housing market’s composition to evolve. Here are 10 trends from NAR’s 2025 Profile of Home Buyers and Sellers report, reflecting a survey of home buyers and sellers’ transactions between July 2024 and June 2025.

1. First-time buyers sink to an all-time low

First-time buyers now make up just 21% of the market—the lowest share since NAR began tracking in 1981. Before 2008, they consistently accounted for about 40% of home sales. Limited inventory and affordability challenges have pushed many out of the market. “The historically low share of first-time buyers underscores the real-world consequences of a housing market starved for affordable inventory,” Lautz says.

Those who do buy are older, too. The median age of first-time buyers has climbed to a record 40—up from the late 20s in the 1980s. High rents and student loan debt make saving for a down payment increasingly difficult. “For generations, access to homeownership has been the primary way Americans build wealth and the cornerstone of the American dream,” says Shannon McGahn, NAR executive vice president and chief advocacy officer. “Delayed or denied homeownership until age 40—instead of 30—can mean losing roughly $150,000 in equity on a typical starter home.”

FHA and VA loan usage have dipped (FHA loans alone have fallen from 55% in 2009 to 28% in 2025, NAR’s report shows). But McGahn says these low- or zero-down payment programs have long helped millions of Americans achieve homeownership. She says tackling affordability will require addressing the root issue: housing supply.

NAR is urging for government policymaking that would help unlock existing inventory, enable more new home construction, streamline local zoning and permitting, and modernize construction methods to build more homes faster and more affordably—to help loosen the constraints on first-time home buyers.

2. Record high of all-cash home buyers

All-cash home purchases have reached an all-time high, averaging 26% over the last year. By comparison, between 2003 and 2010, fewer than one in 10 buyers paid all cash on a home sale. Cash buyers may be leveraging the equity from a previous sale, but with rising interest rates and tight lending conditions, they’re finding a distinct advantage in the market by being able to bypass mortgages.

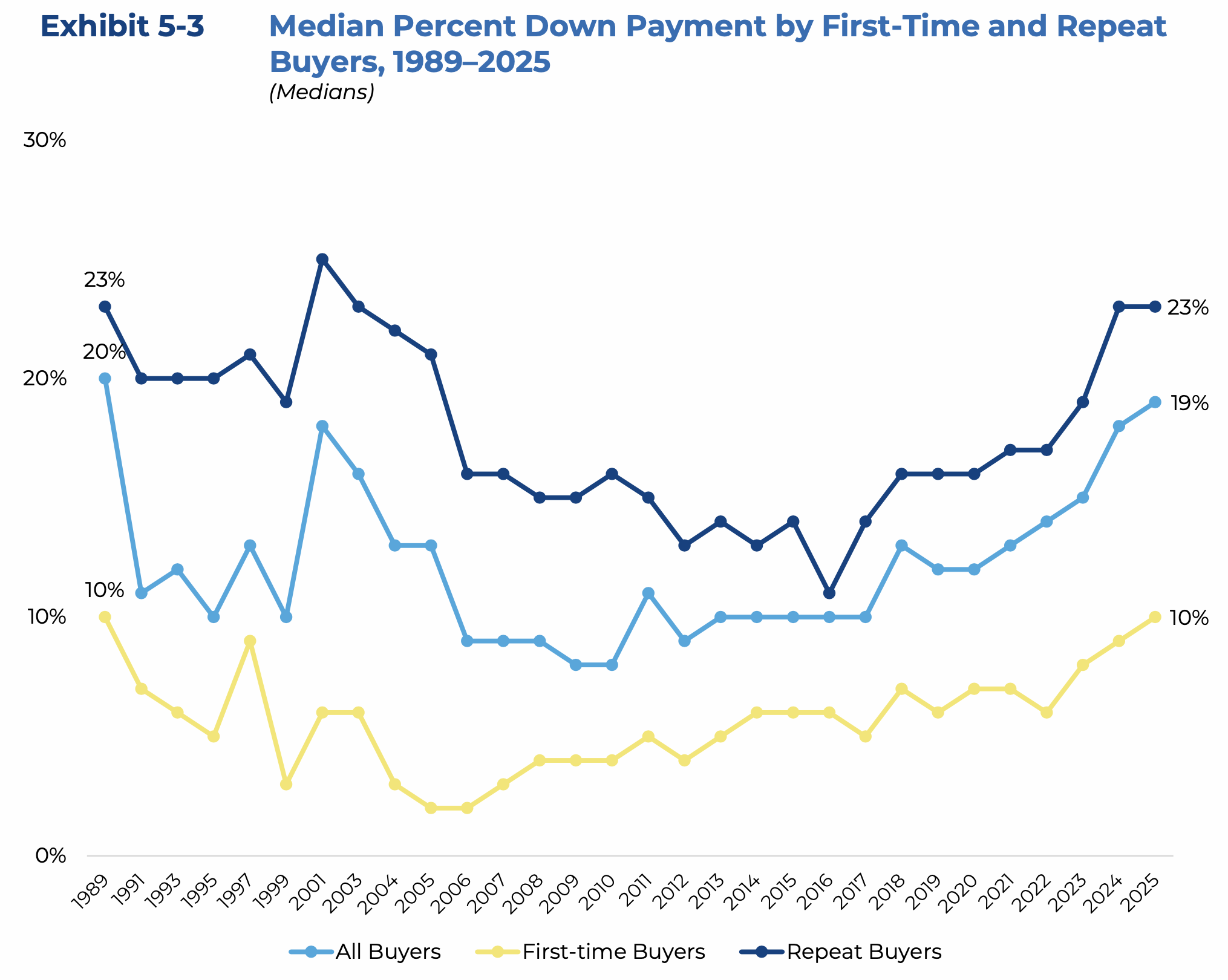

3. Higher down payments

Down payments continue to rise for both first-time and repeat buyers, reaching levels not seen in decades. In 2025, the median down payment among all buyers was 19%—10% for first-time buyers and 23% for repeat buyers. That marks the highest median down payment for first-time buyers since 1989 and the highest for repeat buyers since 2003.

Personal savings remain the most common source for down payment funds among first-time buyers—with 59% relying on savings—while 26% tapped into financial assets such as 401(k)s, IRAs or stocks, and 22% received help from relatives or friends through a gift or loan. Among repeat buyers, more than half—54%—used proceeds from the sale of a previous home to finance their next purchase.

© 2025 National Association of REALTORS®

4. Real estate agents remain essential

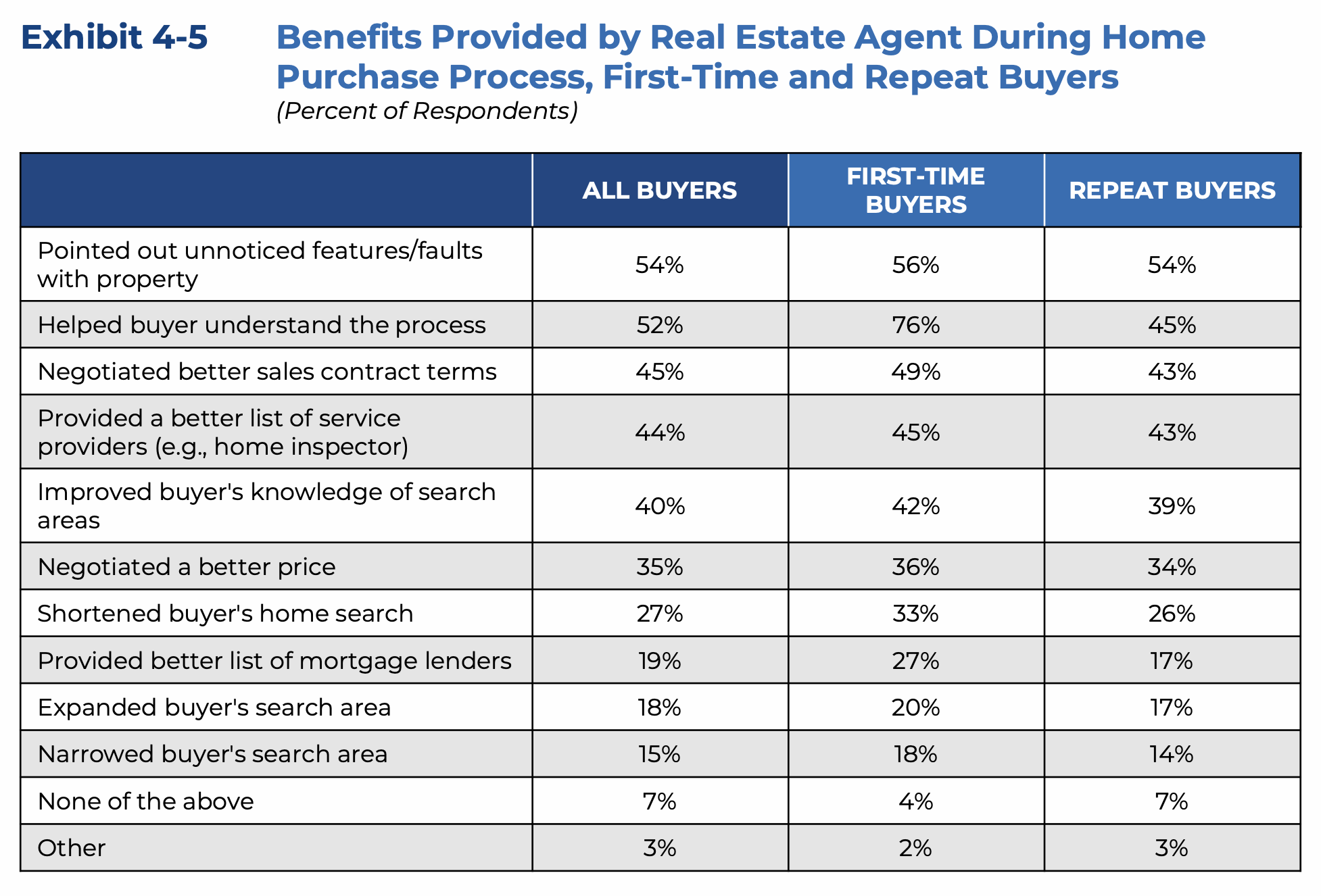

Real estate professionals continue to play a central role in buying and selling homes. Eighty-eight percent of buyers purchased their home through an agent or broker, making agents the most trusted and frequently used information source—well ahead of online listings. Buyers primarily sought help finding the right home, negotiating terms and navigating paperwork. More than half of buyers said they valued that their agent pointed out property features or flaws they hadn’t noticed, and 76% of first-time buyers credited their agent with helping them understand the process.

Sellers also placed a high value on their agents’ expertise: 91% used a real estate agent—matching the highest percentage on record. The top priorities when choosing an agent include getting help to market the home to potential buyers, pricing the home competitively and selling within a specific timeframe.

“Real estate agents remain indispensable in today’s complex housing market,” Lautz says. “Beyond guiding buyers and sellers through what is often the largest financial decision of their lives, agents provide critical expertise, negotiation skills and emotional support during an increasingly challenging process.”

© 2025 National Association of REALTORS®

5. FSBOs hit record low

Only 5% of homes over the past year sold as For Sale By Owner, an all-time low, while a record 91% of sellers used a real estate agent, NAR’s data shows. FSBOs don’t typically fare as well, selling for significantly less than agent-assisted homes—a FSBO median price of $360,000 versus $425,000 for agent-assisted homes. The most common motivations for homeowners to sell by owner include selling to a friend or relative or avoiding paying agent commission fees.

6. Repeat buyers are flexing their financial power

The median down payment among this group climbed to 23%, and nearly one in three repeat buyers are paying all cash—sidestepping financing altogether. Years of equity growth have supercharged their buying power. With home values steadily rising, long-term owners have built substantial wealth: The typical seller has owned their home for a record 11 years, giving them a deep equity cushion to tap for their next move. In just the last five years alone, homeowners have gained an average of $140,900 in wealth, according to NAR’s research.

7. Fewer households with children are buying homes

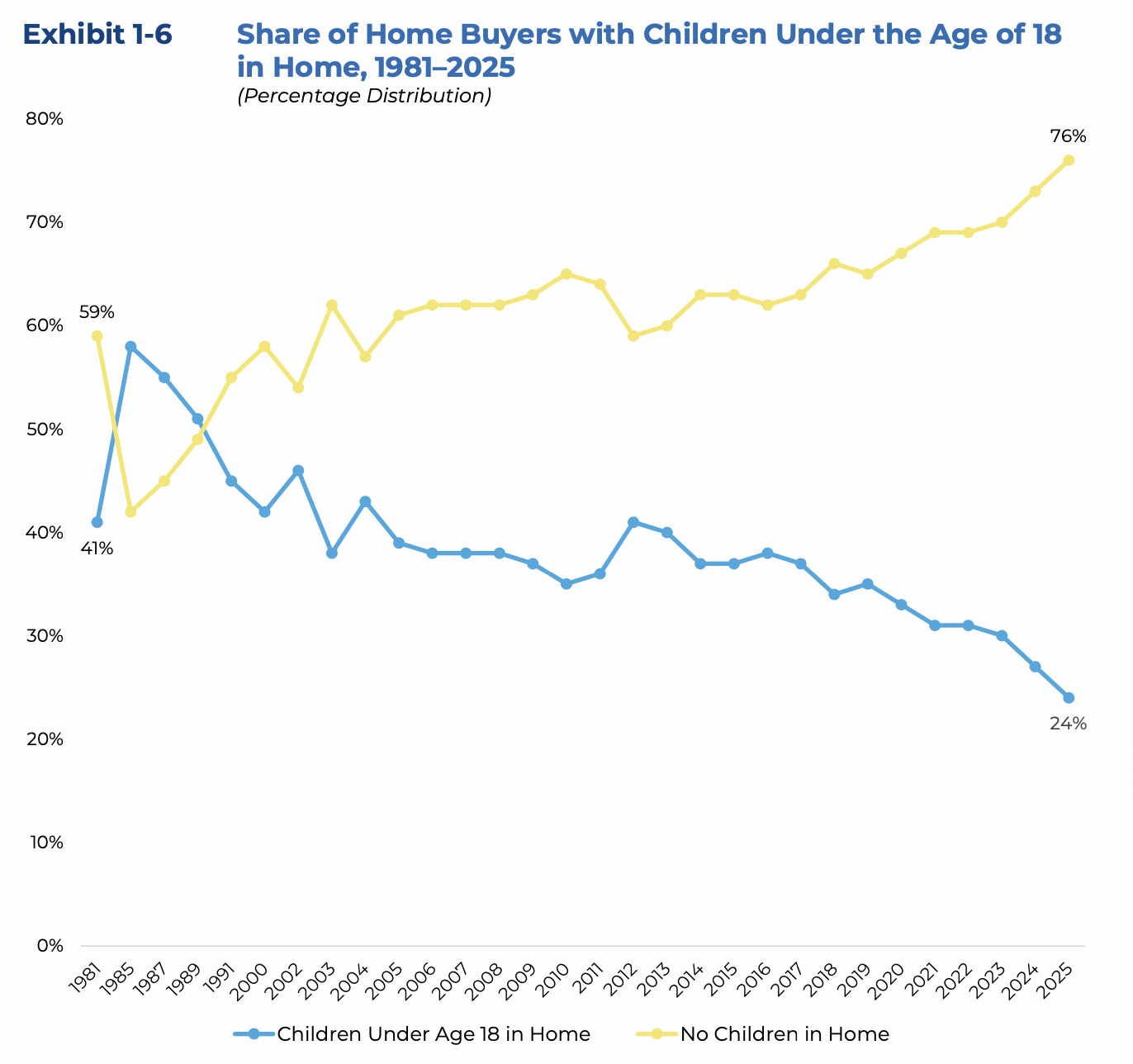

The share of buyers with children under 18 has dropped to a historic low—just 24% of recent buyers compared to 58% in 1985. Among those households, 11% had one child, 9% had two and only 5% had three or more. “A reduction of home buyers with children is likely being shaped by a reduction in birth rates and a rise in older repeat buyers,” NAR’s report notes. Steep childcare costs also are taking a toll, limiting families’ ability to save for a down payment.

As households with children decline, the makeup of home buyers is shifting. Married couples also fell to 61% of all buyers as singles gained ground—single women comprised 21% of buyers and single men accounted for 9%. Together, these trends point to a clear move away from the traditional family household and toward a more diverse range of home buyers.

© 2025 National Association of REALTORS®

8. Home buyers and sellers are getting older

The median age of first-time buyers is 40—a record high—while repeat buyers rose to a median age of 62. Sellers are following the same trend—the typical age of home sellers this year is 64, the highest ever recorded. The findings coincide with a separate NAR report earlier this year that showed baby boomers, those between the ages of 60 and 78, are the largest share of both home buyers and sellers—moving markets more than younger generations often due to their better financial position.

Read more: The ‘Silver Tsunami’ in Real Estate Is Here: Are You Ready?

9. Buying for the long haul

Home buyers are planning to stay put longer than ever. The median expected tenure in a purchased home is now 15 years, with 28% of buyers declaring it’ll be their “forever home” and that they never intend to move. This marks a significant increase from 2000 to 2008 when sellers typically stayed in their homes for just six years. Already, the median time over the last year a homeowner stayed in their home before selling was 11 years—a record high. Both first-time and repeat buyers share this longer-term outlook, proving the “starter home” mentality for new buyers has faded.

10. New home purchases tick up

More buyers are tempted to buy new, with the share of new home purchases rising slightly to 16%, matching a level that hasn’t been seen since 2006. Meanwhile, existing-home purchases decreased slightly to 84%. Builders over the last year have been ramping up incentives such as price reductions and mortgage rate buydowns to attract more buyers. Buyers drawn to new construction say it’s to avoid renovations or major repair issues and to have the ability to customize design features. For buyers favoring existing homes, they point to perceptions of better overall value, lower price, and greater charm and character of the housing stock.