")

Homeowners who encounter financial trouble may not know where to turn when they can no longer afford their monthly mortgage payments. Mortgage relief through forbearance may help.

What Is Mortgage Forbearance?

Mortgage forbearance is when a borrower can temporarily postpone or reduce loan payments with their lender for a set period of time. For homeowners who face a job loss, unexpected illness or even property damage from a natural disaster, forbearance allows them to temporarily pause or lower their mortgage payments while they get back on solid financial footing.

The rate of mortgage forbearance grew during the COVID-19 pandemic due to the sudden economic downturn and the urgent need to help many homeowners avoid foreclosure. A special mortgage forbearance program—part of the 2020 Coronavirus Aid, Relief, and Economic Security (CARES) Act—enabled about 8 million homeowners to temporarily suspend their mortgage payments.

Following the end of their forbearance period, most homeowners resumed their mortgage payments and avoided defaulting on their loans or going into foreclosure. That’s a stark contrast to the 2008 financial crisis, when mortgage forbearance wasn’t readily available to homeowners.

Since the pandemic, the rate of forbearance has dropped significantly. Only 180,000 homeowners were in forbearance by the end of March 2025, representing 0.36% of the mortgage market, according to the Mortgage Bankers Association. The majority of those cases were related to a temporary hardship (like a job loss, divorce or injury); 21% of cases were due to homeowners facing a natural disaster.

As more studies point to the potential for mortgage forbearance to have a positive impact on the housing market, policymakers are urging lenders to promote forbearance programs. It could help prevent tens of thousands of foreclosures each year, according to a study from the Urban Institute.

In this guide, learn more about forbearance and how it can impact real estate markets, including home sales, property values and more.

Qualifying for Mortgage Forbearance

Borrowers who qualify for mortgage forbearance through their loan servicer or lender can temporarily pause their mortgage payments or make smaller payments for a set period of time—typically, a year or less. Forbearance is usually an option lenders extend only to homeowners who experience a sudden, short-term setback, such as a job loss, unexpected illness or natural disaster. Borrowers must request forbearance from their lender before stopping mortgage payments.

Forbearance is not loan forgiveness. Borrowers still have to pay back delayed payments and interest accrued during their forbearance period. Lenders will set up a repayment plan, and borrowers will be responsible for those payments in addition to their monthly mortgage payment.

Not every homeowner with a financial hardship will qualify for forbearance. Lenders may choose to deny forbearance to a borrower who has an inconsistent payment history or low credit score. Ineligible homeowners may need to explore other options, such as loan modification or selling the property.

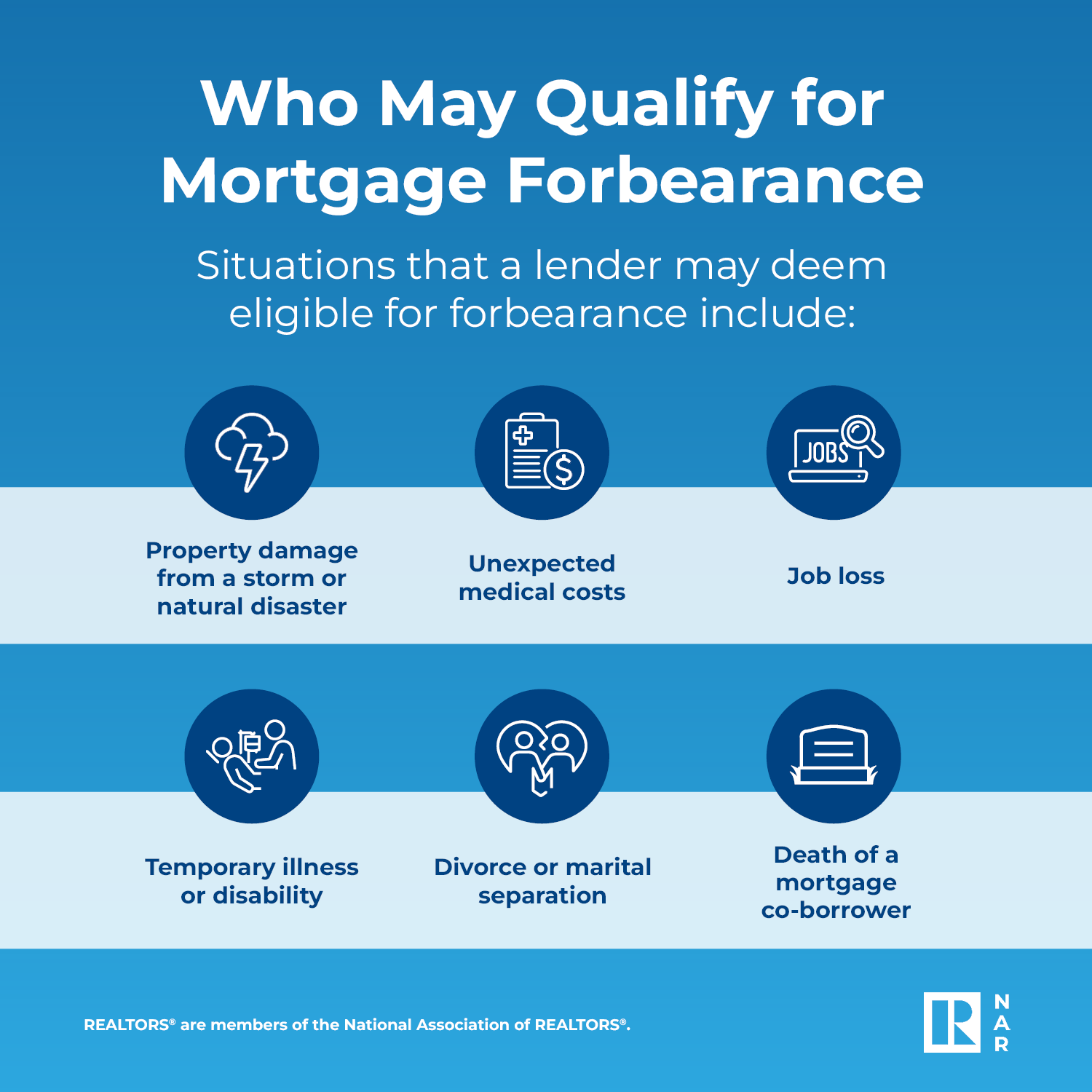

Who May Qualify for Mortgage Forbearance

Situations that a lender may deem eligible for forbearance include:

- Property damaged from a storm or natural disaster

- Unexpected medical costs

- Job loss

- Temporary illness or disability

- Divorce or marital separation

- Death of a mortgage co-borrower

Downloadpdf (55 KB) | png (132 KB)

How to Apply

- Contact the mortgage servicer, which is the company that receives the monthly mortgage payment, before missing any payments. Failure to do so could jeopardize approval and affect the borrower’s credit score.

- Have a copy of the most recent mortgage statement.

- Be able to explain and provide any supporting evidence of the financial hardship and demonstrate that it’s temporary.

- Have a copy of estimated monthly income and expenses.

- Discuss how repayment will be structured when forbearance ends.

Types of Forbearance Programs

As the Consumer Financial Protection Bureau notes, there’s no “one-size-fits-all” approach when it comes to forbearance. Mortgage relief options can depend on a borrower’s personal situation as well as their mortgage servicer. For example, forbearance offerings may differ between conventional lenders and government agencies, such as the Department of Veterans Affairs or the Federal Housing Administration.

Special forbearance programs may be initiated due to broader economic hardships or natural disaster events. For example, mortgage financing giants Fannie Mae and Freddie Mac offer forbearance programs for borrowers with government-backed mortgages who have been affected by a natural disaster. Under these special forbearance programs, borrowers will not incur late fees or foreclosure, and other legal proceedings will be suspended. Additional assistance or extensions may be available at the end of the forbearance period, if needed.

During the COVID-19 pandemic, the forbearance program created by the CARES Act allowed millions of borrowers with federally backed mortgages to postpone their payments without fees or penalties for up to 18 months. In some cases, borrowers were granted extensions. After forbearance ended, homeowners were often provided the option to defer delayed payments to the end of their mortgage term or take out a second-lien loan.

While forbearance can help homeowners get through difficult times, it comes with potential drawbacks. In particular, repayment could put some homeowners at risk of foreclosure if they are unable to afford higher monthly mortgage payments or a lump sum.

Forbearance Questions to Ask a Lender

In weighing the pros and cons of forbearance, borrowers may want to ask their lender the following questions:

- What is the length of the forbearance period? Is there potential for any extensions?

- What am I required to pay each month? Will my payments be completely suspended during forbearance, or do I still need to pay a certain amount?

- Will the forbearance be reported to the credit bureaus? If so, how could this affect my future credit eligibility?

- How will I be expected to resume monthly mortgage payments and pay back the forbearance amount? Will the repayment plan be in installments, a lump sum or another agreement?

Downloadpdf (58 KB) | png (144 KB)

Forbearance Repayment Options

Following forbearance, borrowers will not only have to resume their normal mortgage payments but also pay back any delayed payments and interest accrued during that period. However, there may be some repayment options, such as:

- Reinstatement: After forbearance ends, borrowers pay back all delayed payments in one lump sum. Borrowers will need to be prepared for a significant bill at the end of forbearance, depending on how long they had suspended payments. Borrowers who expect to receive a sizable paycheck from an insurance reimbursement, for example, may prefer this form of repayment plan.

- Installments: A lender arranges for the repayment plan to be spread out in installments over a certain period. This may occur by increasing the total amount of a borrower’s regular monthly mortgage payments.

- Deferral payments: The sum of the delayed payments is added to the end of the mortgage term. Note: This can cause a significant amount of additional interest to be accrued over the life of the loan.

- Loan modification: Borrowers who have a longer-term financial setback may ask their lender if they qualify for a loan modification, which could include recasting the interest rate or stretching out the loan’s term. Lenders likely will not approve this unless they determine that a borrower is no longer able to afford their current mortgage payments.

- Sell the home: Homeowners who continue to struggle to make their mortgage payments may want to contact a real estate professional about selling their home. This will allow them to use any equity from the sale to pay off their mortgage—including the amount they still owe from forbearance. They can then relocate to a more affordable living arrangement. However, homeowners who owe more on their mortgage than their home is worth may need to explore additional options with their mortgage servicer, like approval for a short sale or a deed in lieu of foreclosure.

Mortgage Forbearance vs. Deferring a Mortgage

Mortgage forbearance and deferment reflect two different approaches for delaying payments. A mortgage forbearance allows borrowers to temporarily pause or reduce their mortgage payments—typically, for a year or less. Borrowers then set up a repayment plan to pay back the delayed payments. On the other hand, mortgage deferments allow borrowers to halt or defer their payments—possibly up to 36 months, depending on the loan—and repay at the end of their loan term or when they sell or refinance their home. A mortgage deferment could be one possible repayment option when a homeowner exits forbearance.

Can Mortgage Forbearances Affect Credit?

Mortgage forbearance is not likely to have a significant impact on a homeowner’s credit score, as long as the borrower complies with the repayment terms, according to Experian, a consumer credit reporting agency. However, some lenders may report a forbearance to the national credit bureaus—Equifax, Experian and TransUnion.

Experian notes that forbearance is a much better financial alternative than a foreclosure, which could significantly damage a person’s credit and affect his or her ability to qualify for a loan in the future.

The Effects of Mortgage Forbearance on Home Sales

Forbearances can have an impact on the housing market and affect home buyer confidence, property values and more. While forbearance indicates that a given homeowner is in distress, it’s not always a negative sign for the housing market as a whole. As made evident during the pandemic, the majority of homeowners in forbearance were able to remain in their homes, and only a small fraction chose to exit forbearance by selling their home.

What’s more, the elevated number of forbearances during the pandemic largely has been credited with helping to prevent a wave of foreclosures. A study that looked at forbearance during the first year of the pandemic estimated that about 500,000 borrowers likely avoided foreclosure during the fourth quarter of 2020 alone due to mortgage forbearance options.

Impact on Sellers

Homeowners in forbearance who face a prolonged financial setback may ultimately decide to sell their home and find a more affordable living situation. A homeowner who sells while in forbearance could avoid foreclosure by using the profits from the sale to cover repayment and close out the mortgage. Homeowners may be more likely to use this alternative if they have high amounts of equity in their home due to a rise in property values.

However, the decision to sell while in forbearance could present some unique challenges in a real estate transaction. Here are some factors homeowners will want to consider:

Understand What’s Owed

Sellers in forbearance are still responsible for repaying their home loan. So, they should make their real estate agent aware of their forbearance status, as the final loan payoff could be higher than expected because of fees or added interest. Plus, real estate professionals can help determine the home’s estimated value and potential equity. But if the home is worth less than the outstanding mortgage balance—accounting for the forbearance repayment, too—homeowners may need to explore other options with their lenders, such as a short sale or deed in lieu of foreclosure.

Weigh the Pros and Cons

Homeowners may find that selling will help them avoid foreclosure or obtain enough funds to cover forbearance repayment. But selling could also mean that homeowners will need to find an alternative living arrangement in order to ensure they can cover the costs of a sale, such as moving expenses.

Impact on Home Pricing and Inventory

Forbearance can affect housing inventory and home prices. A report conducted by the Federal Reserve found that the widespread availability of mortgage forbearance during the pandemic may have bolstered home prices 0.6 percentage points between April 2020 and August 2020 compared to the same four-month period in 2019.

“Forbearance allows liquidity-constrained households to defer mortgage payments and remain in their homes, potentially preventing a rise in unemployment from driving an increase in housing supply,” the Fed study notes.

“Forbearance may have contributed to house price growth by limiting the effect of labor market weakness on for-sale housing supply.”

Foreclosure Risk and Its Implications

Homeowners in forbearance may be at increased risk for foreclosure, particularly if their financial hardship extends beyond their forbearance period. Foreclosures not only affect homeowners’ livelihood and ability to obtain future credit but also can negatively affect the values of neighboring homes.

Still, forbearance doesn’t always end in foreclosure. Foreclosure rates during the pandemic were lower than previous years, despite widespread economic hardship. Researchers have concluded that forbearance, combined with growing home values at the time, helped real estate markets avoid a spike in foreclosures.

Also, most borrowers worked out additional solutions with their lender after forbearance, if needed, such as a loan modification or deferment.

Impact on Buyer Confidence

Widespread forbearance in a certain area could possibly shake home buyer confidence. Forbearance is indicative of a financial hardship, so elevated numbers in a particular housing market could be a sign of high unemployment, a natural disaster, or other location-specific economic hardship. Some wary home buyers may make lower offers on homes or even hesitate to make an offer, questioning whether the area is still a wise investment.

Home buyers also may judge a property after learning a seller is in forbearance and assume the owner’s financial troubles affected their ability to adequately maintain the property.

A real estate agent can help mitigate the potential impact on buyer confidence from forbearance by providing information on local real estate trends and home values, and encouraging buyers to complete a home inspection to evaluate the property’s condition prior to closing.

How Can Real Estate Professionals Handle Mortgage Forbearance?

Real estate professionals should refer clients to a mortgage servicer for financial advice regarding mortgages and loan workout options. Also, homeowners can find information on forbearance programs for government-sponsored loans, including:

Further, the Department of Housing and Urban Development offers housing counseling for borrowers who are struggling to pay their mortgage.

When real estate professionals encounter home sellers who are in forbearance, they will need to work with those sellers and their mortgage servicers to ensure the seller has sufficient proceeds to pay off the mortgage and forbearance amount. This can help avoid potential sales delays.

Mortgage Forbearance: The Bottom Line

Ninety-four percent of mortgage defaults occur when a homeowner loses income due to extenuating circumstances, according to research from the National Bureau of Economic Research. Mortgage default often leads to foreclosure, which not only hampers a homeowner’s financial future but also can negatively affect neighboring property values.

However, during the COVID-19 pandemic, for example, mortgage servicers and lenders increasingly offered mortgage forbearance to help cash-strapped homeowners remain in their home as they overcame a temporary financial setback, according to a study conducted by JPMorgan Chase Institute Research.

And as researchers found, millions of homeowners who used this kind of short-term mortgage relief were able to resume their payments, and a foreclosure spike was avoided. The situation was in stark contrast to the 2008 financial crisis, when an economic downturn had prompted a surge in mortgage defaults and foreclosures, which plummeted home values, researchers note.

According to the JPMorgan Chase Institute study, “the success of the mortgage forbearance policies themselves will depend critically on the results of exit options. Exit options will vary for different homeowners, depending on who owns their loan, who services the loan and their own financial circumstances at the end of the forbearance period. … [But we continue to see] evidence that mortgage forbearance helped families facing financial difficulty during a sudden and severe economic contraction get immediate payment relief.” The payment relief afforded by forbearance may help many homeowners avoid any larger real estate fallout.