The Effect of Eliminating the State and Local Real Estate Tax Deduction on a Typical Homeowner

Undoubtedly, all eyes in Washington are focused on the “Big 6” and the release of the tax reform framework some weeks ago. Under this framework, standard deduction will be doubled while mortgage interest and charitable contributions will be the only remaining deductions. This means that state and local real interest deduction will be eliminated among other existing deductions. But how a typical homeowner will be affected by this elimination?

Most state and local governments charge an annual tax on the value of real property. Statewide, the real estate tax varies between 0.27% and 2.35%. New Jersey has the highest effective rate at 2.35% and is followed closely by Illinois (2.30%), New Hampshire (2.15%), and Connecticut (1.97%). On the other end of the spectrum, Hawaii has the lowest effective rate at 0.27%, and is followed closely by Alabama (0.43%), Louisiana (0.49%), and Delaware (0.54%).

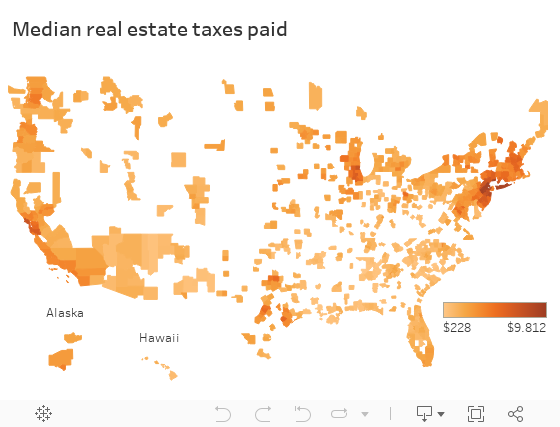

Since all real estate is local, we looked at the median amount of real estate taxes paid at county level in 2016. As the data shows, among 815 counties[1], Passaic County, NJ had the highest median real estate taxes paid ($9,812), followed by Union County, NJ ($9,594) and Putnam County, NJ ($9,447). In contrast, homeowners in Walker County, AL and St. Landry Parish, LA paid less than $300 for real estate taxes in 2016. See below how your county compares to other 815 counties:

Under the current tax framework, homeowners choose to itemize when the sum of itemized deductions are higher than the standard deduction which is currently at $12,700. If individual deductions like mortgage interest and property tax are less than $12,700, they would take the standard deduction. A deep look into the data above reveals that real estate tax deduction helps homeowners in many counties to itemize while real estate taxes can represent up to 80% of the standard deduction. Especially, homeowners who reside in areas with affordability challenges and high real estate taxes can save money using the mortgage interest and real estate tax deductions.

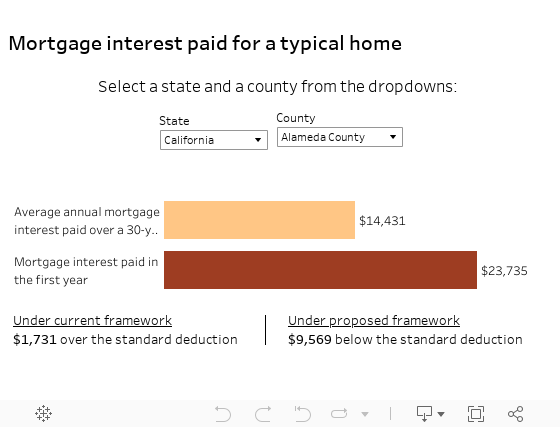

However, under the proposed framework, the standard deduction is expected to rise to $24,000 and state and local tax deductions to be eliminated. Then, some homeowners will not claim the mortgage interest deduction since mortgage interest deduction will not be enough to make it advantageous for them to continue itemizing. If owners don’t have enough in deductions to exceed the standard deduction amount, it is not worth doing so. As a result, homeowners will stop itemizing and instead take the standard deduction. Because of the large standard deduction, most renters will benefit. The new enlarged benefit for renters also lessen the incentive to become homeowners. It is noteworthy that the new tax reform will hurt new home buyers while mortgage interest is higher during the first years of the mortgage and they would save substantially if they could use the mortgage interest deduction. See below how much mortgage interest[2] a homeowner pays for a typical home at the following counties: