The 2021 spring market is starting off at the lowest level of inventory of homes on the market in nearly 40 years, with job growth ramping up amid an aggressive fiscal policy and continued low mortgage rates. Homebuyers are likely to face the most competitive spring market in years. Here are the latest indicators on inventory, pending sales, home prices, job growth, and mortgage rates that are pointing to a hot spring market in a broad swath of metro areas.

Shortage of 2.4 million homes for sale to meet 6 months of supply

The inventory of existing and new single-family homes for sale is the lowest since 1982.1 As of the end of February 2021, the inventory of homes for sale stood at a historic low of 1.07 million (1.03 million of existing homes, 42,000 new single-family homes), which is equivalent to just 1.8 months of the average monthly sales of 582,917 (518,333 of existing homes, 64,583 of new single-family homes), a near historic low (1.7 months in December 2020 and January 2021 were the historic lows).

Historically, six months of the average monthly demand has kept home prices from overheating. At six months of inventory, there should be 3.49 million homes on the market, but as of February, only 1.07 million homes are on the market, resulting in a gap of 2.4 million homes for sale.

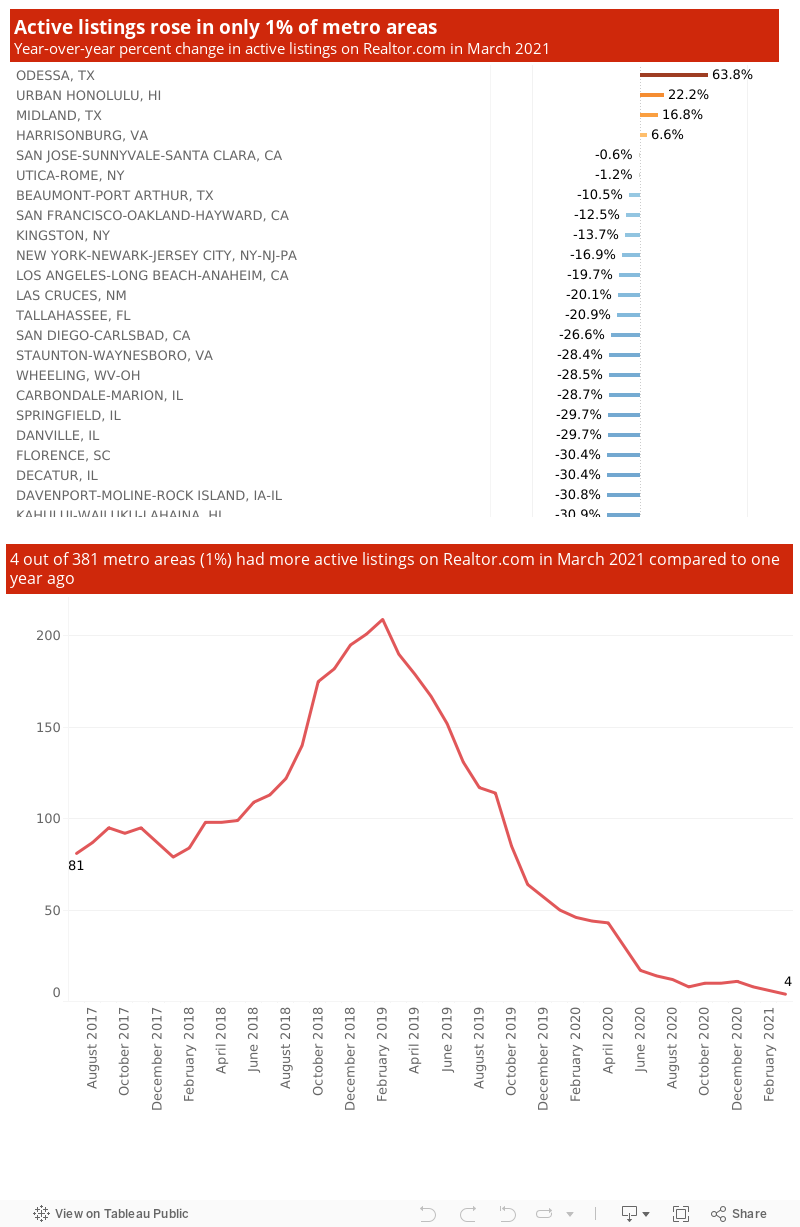

There's a dire lack of inventory across all metropolitan areas. Realtor.com reported that only 4 out of 381 metro areas or just 1% of metropolitan areas had more active listings in March 2021 compared to one year ago (Odessa, Texas, Urban Honolulu, Midland, Texas, and Harrisonburg, Virginia). The decline in active listings are mind-boggling, with 375 out of 381 metro areas posting double-digit declines.

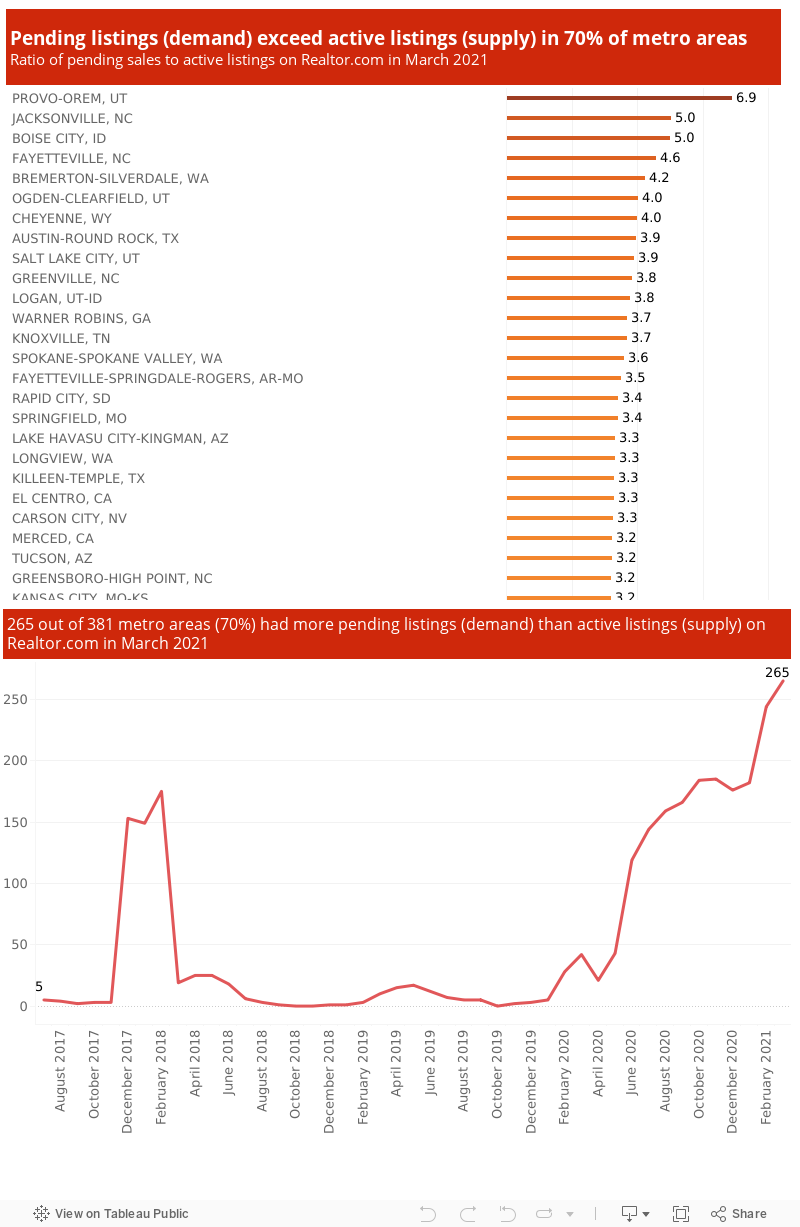

Demand (pending listings) is outstripping supply (active listings) in 70% of metro areas

A leading indicator of home sales and a good indicator of the demand for homes is pending listings. Most pending listings will turn into sales, and based on NAR's Realtors® Confidence Index Survey, 6% of contracts are terminated (latest data as of February 2021).

In 70% of metro areas (265 out of 381 metro areas tracked by realtor.com®), the number of pending listings that can be expected on a given day in the month was higher than the number of active listings that can be expected on any given day in the month.

The ratio of pending sales to active listings is an indicator of how hot the market is. The top 5 metro areas with the largest ratios were Provo-Orem, Utah (6.9); Boise City, Idaho (5.0); Jacksonville North Carolina (5.0); Fayetteville North Carolina (4.6); and Bremerton-Silverdale, Washington (4.2).

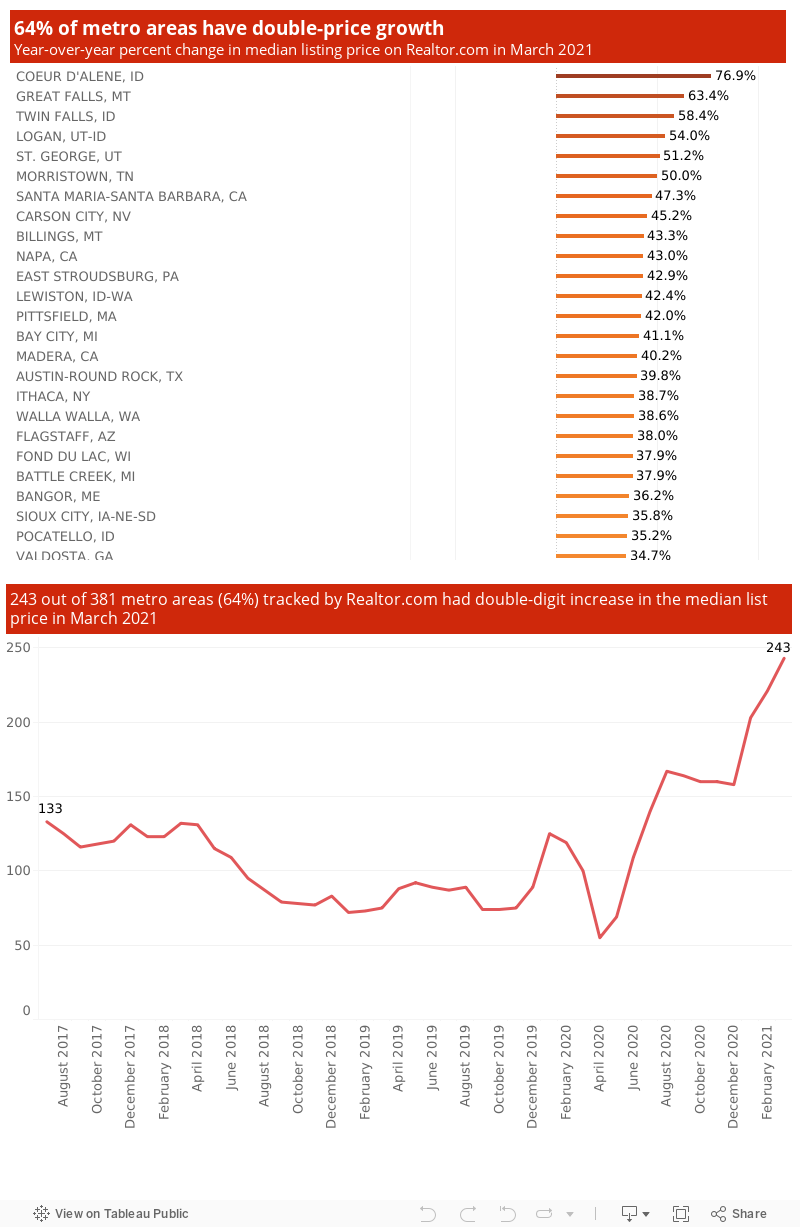

Listing prices are rising at double-digit rates in 64% of metro areas

Prices are the best indicator of demand and supply fundamentals. As of March, 64% of metro areas are posting double-digit year-over-year price appreciation, based on realtor.com® listings. The strongest price appreciation is occurring in the metro areas of Utah, Idaho, and Montana: Coeur D' Alene, Idaho (76.9%); Great Falls, Montana (68.4%); Twin Falls, Idaho (58.4%); Logan, Utah, Idaho (54%), and St. George, Utah (51.2%). Idaho and Utah are the only states where non-farm payroll employment is higher as of March 2021 compared to one year ago.

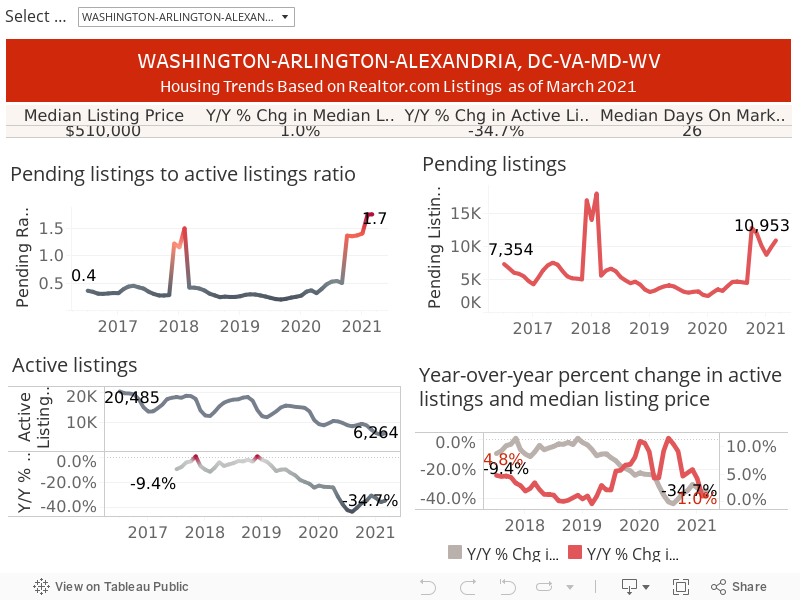

Explore housing market trends across metro areas using this tool:

Expectation of higher mortgage rates in the future will drive demand now

Mortgage rates are still trending at historic lows, with the 30-year fixed rate mortgage falling to 3.13% in the week of August 8, still a tad lower than 3.33% one year ago (April 10). NAR's Chief Economist Lawrence Yun expects mortgage rates to hover at below 3.5% in 2021. Mortgage rates are likely to go up, not down. Inflation rates are still trending at below 2% and with the average inflation targeting adopted by the Federal Open Market Committee, the federal funds rate can remain at 0 to 25% in 2022. However, the 30-year fixed mortgage rate is driven by the 10-year Treasury Note, and as the economy continues to improve, current bond investors will tend to shift away from lower-yielding Treasury Notes and move into the higher-yielding equities (stocks) market, which will lead to lower demand for bonds and higher interest rates. Buyers expecting higher mortgage rates will tend (and should) get into the homebuying market now, pushing up demand.

Sustained employment growth will tend to increased home demand

Employment continues to recover under highly accommodating monetary policy and a strong dose of fiscal expansion (hovering at $5 trillion with the passage of the $1.9 trillion 2020 CARES Act, $900 billion 2020 Consolidated Appropriations Act of 2021, and the $1.9 trillion 2021 American Rescue Plan).

In March, the economy created 916,000 jobs. Since May 2020, the economy has created 13.9 million nonfarm payroll jobs, with the number of lost jobs now at just 8.5 million. Counting the self-employed, 17.5 million jobs have been created, with the unemployment rate falling to 6%.

The job recovery is broad-based, with all industries showing jobs gains since May (although only the finance and insurance industry and federal government have higher nonfarm employment in March 2021 compared to peak employment in February 2020).

1 NAR started tracking single-family and condominium existing home sales in 1999 but collected data on single-family homes starting in 1982.