")

Quick Takeaways

- Homeowners insurance protects you from unexpected losses at your home, covering repairs, replacements, and certain legal/medical fees.

- If you have a mortgage, your lender will require it. If you own your home outright, it's not legally required but highly recommended.

- The cost varies based on your disaster risk and other factors like your home's age, size, condition, and location.

What Is Homeowners Insurance?

A homeowners insurance policy covers a homeowner for unexpected losses at their home or property. It can include provisions to repair or rebuild the property, replace assets within the home, cover accidents that happen to the homeowner or someone else on the property, or even pay for living expenses if a covered incident forces them to live elsewhere temporarily.

Is Homeowners Insurance Required?

Homeowners insurance is a crucial step in your client’s journey to home ownership. In fact, they may not be able to buy the home without it. The mortgage lender will require a borrower to have a home insurance policy as long as they have a mortgage. If their mortgage is paid off, or if they've paid for the home outright, no laws require them to maintain insurance but it is still a good idea to consider buying home insurance.

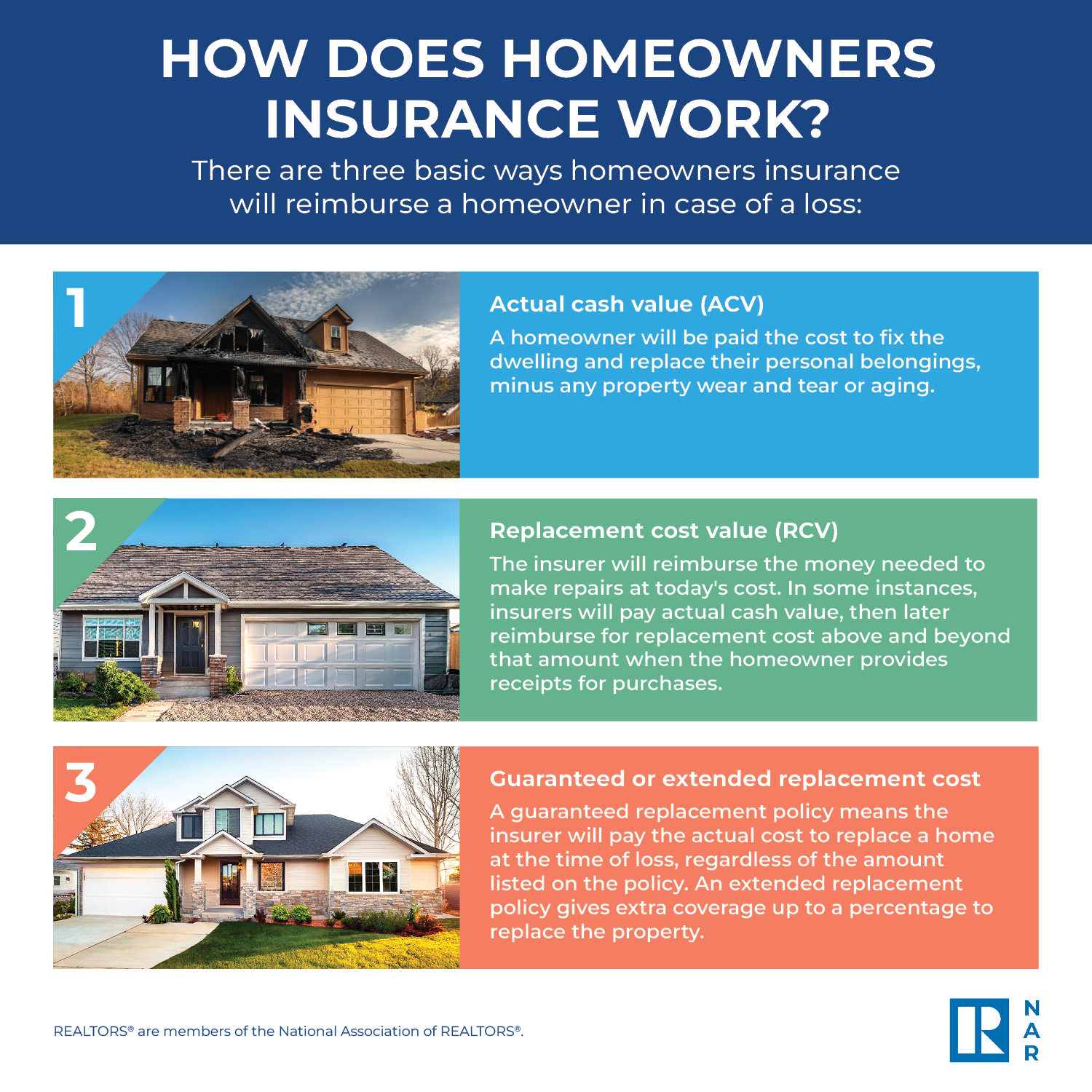

How Does Homeowners Insurance Work?

In the event of a loss, there are two common types of reimbursement. Find out how much your insurer will pay you by visiting the NAR Consumer Guide: Homeowners Insurance.

What Are Homeowners Insurance Premiums?

The cost of homeowners insurance depends on several factors, such as the house’s age, square footage, condition of the property, and location. You may have the option to pay your premium on a monthly, quarterly, or annual basis. Some lenders collect the insurance premium as part of your monthly mortgage payment, place it in an escrow account, and pay the insurer on your behalf.

It is important that home buyers talk to insurance agent when comparing insurance policies for coverage and price. Make sure your client asks questions about the particulars of their coverage and what it does and does not cover – for example, home insurance usually does not cover floods and other natural disasters.

See the References section below for more information to assist buyers with the basics of homeowners insurance, how to estimate the cost of a policy, and ways to lower homeowners insurance costs.

Is Homeowners Insurance Tax Deductible?

If the property in question is your main home, then your home insurance is generally not deductible. However, people who run a business from their home or those intending to rent out their property may be able to claim a deduction. Additionally, if you suffered a loss to your property caused by a presidentially declared disaster, you may be able to claim a casualty loss deduction. Discuss your unique needs with a tax professional.

What to Know About HO3 Insurance

There are different types of insurance policies depending on how many “perils” they cover. “Peril” is an insurance term for a specific risk or reason for a loss. Your insurance will cover a loss only if it is caused by a peril that your policy covers. Policies can vary in which perils are covered, but the most common policy type, HO-3 or the “Special Form,” covers the home structure and personal belongings for disasters including fire, hail, lightning, freezing, theft, and vandalism. Most policies also exclude floods and earthquakes.

Home Warranty vs. Home Insurance

Home warranty covers the repair or replacement of home systems and appliances due to normal wear and tear, while home insurance protects against damage or loss from unexpected events like fire, theft, and natural disasters. Home warranties are optional and focus on maintenance, whereas home insurance is typically required by mortgage lenders and provides broader protection, including liability coverage. Both can be valuable depending on your needs.