As the foreclosure moratorium1 for federally-guaranteed (FHA, VA, USDA) and GSE-backed (Fannie Mae, Freddie Mac) mortgages is about to end on June 30 (unless extended), there are still 2.7 million homeowners who are not caught up on their mortgage payment and 1.8 million loans that are seriously delinquent (90 days or more past due and in foreclosure). How will this impact the housing market and homeownership?

The analysis below shows the impact on housing prices is likely to be minimal, with 77% of loans in forbearance having a debt repayment plan and with a housing shortage of 5 million single-family homes. However, the foreclosures will likely widen the already alarming homeownership gap among income groups and racial groups, with low income and minority groups twice as likely to face foreclosure than higher income and non-minority groups, and homeowners of FHA-insured loans three times as likely to face foreclosure. A repayment scheme where households pay no more than 5% of income is typically affordable for homeowners.

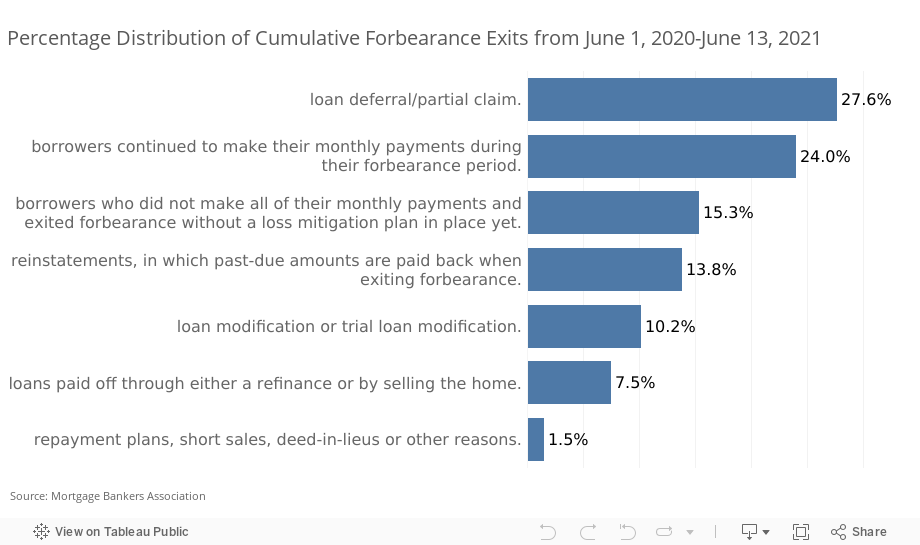

77% of homeowners in forbearance exit with a loss mitigation repayment plan in place

The majority of homeowners in forbearance have workout options, and only small fraction exit forbearance by selling their home. According to Mortgage Bankers Association, 77.1% of homeowners that exit forbearance had a workout (loss mitigation) plan: loan deferral or partial claim (27.6%), continuation of monthly mortgage payment (24%), reinstatement (15.3%), and loan modification (10.2%).

From September 2020 through June 13, 2021, only about 1 in 10 homeowners opted to exit forbearance by selling their home (7.5%) or by a deed-in-lieu or short sales (2%), totaling an estimated 250,000 homes.2

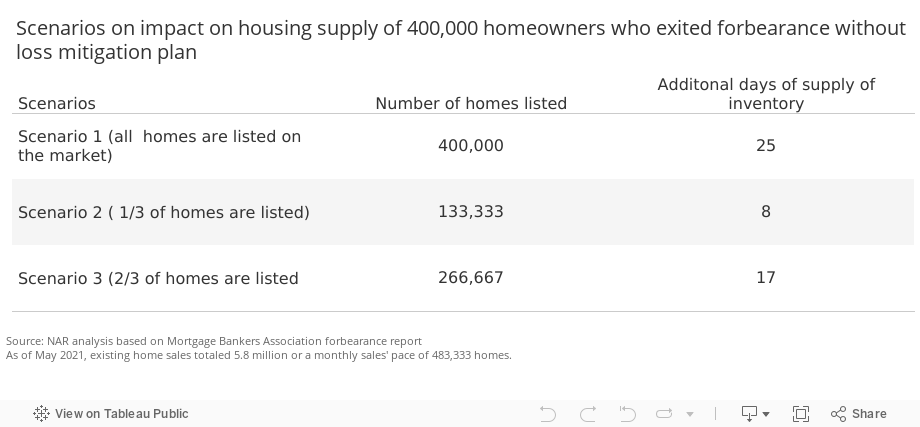

However, 15.3% homeowners exited the forbearance period without a workout plan, totaling about 400,000 homes.3 There is no data on whether these homeowners exited forbearance without a loss mitigation plan in place because they can affordably pay the mortgage, or whether they will likely end up in foreclosure and on the market. If all these 400,000 homes go into foreclosure and get listed, that will add about 24 days of supply to the housing market given the current monthly sales pace of 483,333 existing homes. If only 1/3 of these homes end up on the market, that's 133,200 homes, which will add just 8 days of additional supply. If 2/3 of these homes end up on the market, that's about 268,000 homes, which will add 17 days of supply. Given that only 1 in 10 borrowers are opting to list their homes, the more likely scenario is that 1/3 or even less of the 400,000 that exited forbearance could end up as listed homes, adding some relief to the tight supply — not a glut that could depress prices.

5 million shortage of single-family homes compared to 1.8 million seriously delinquent mortgages

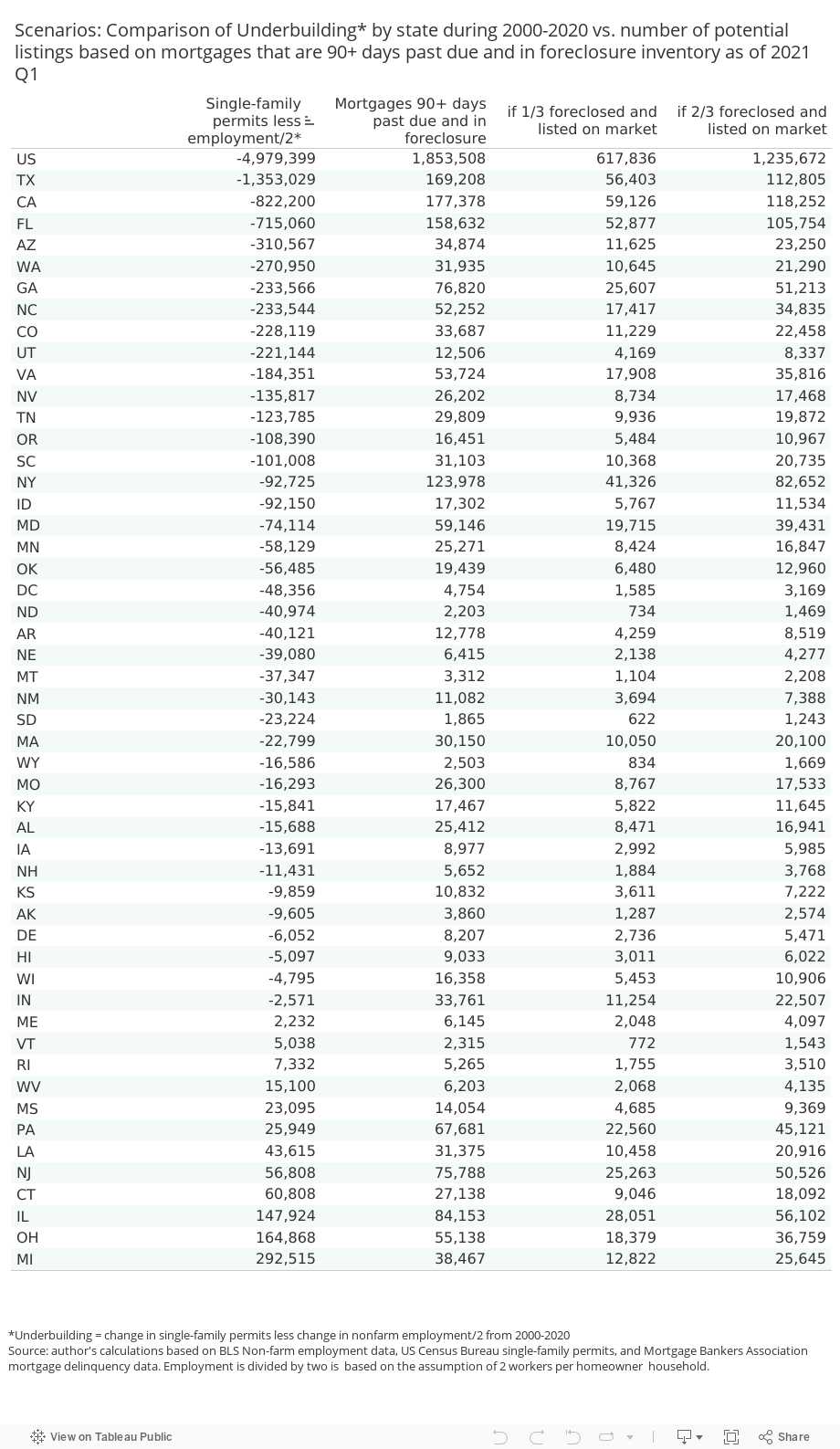

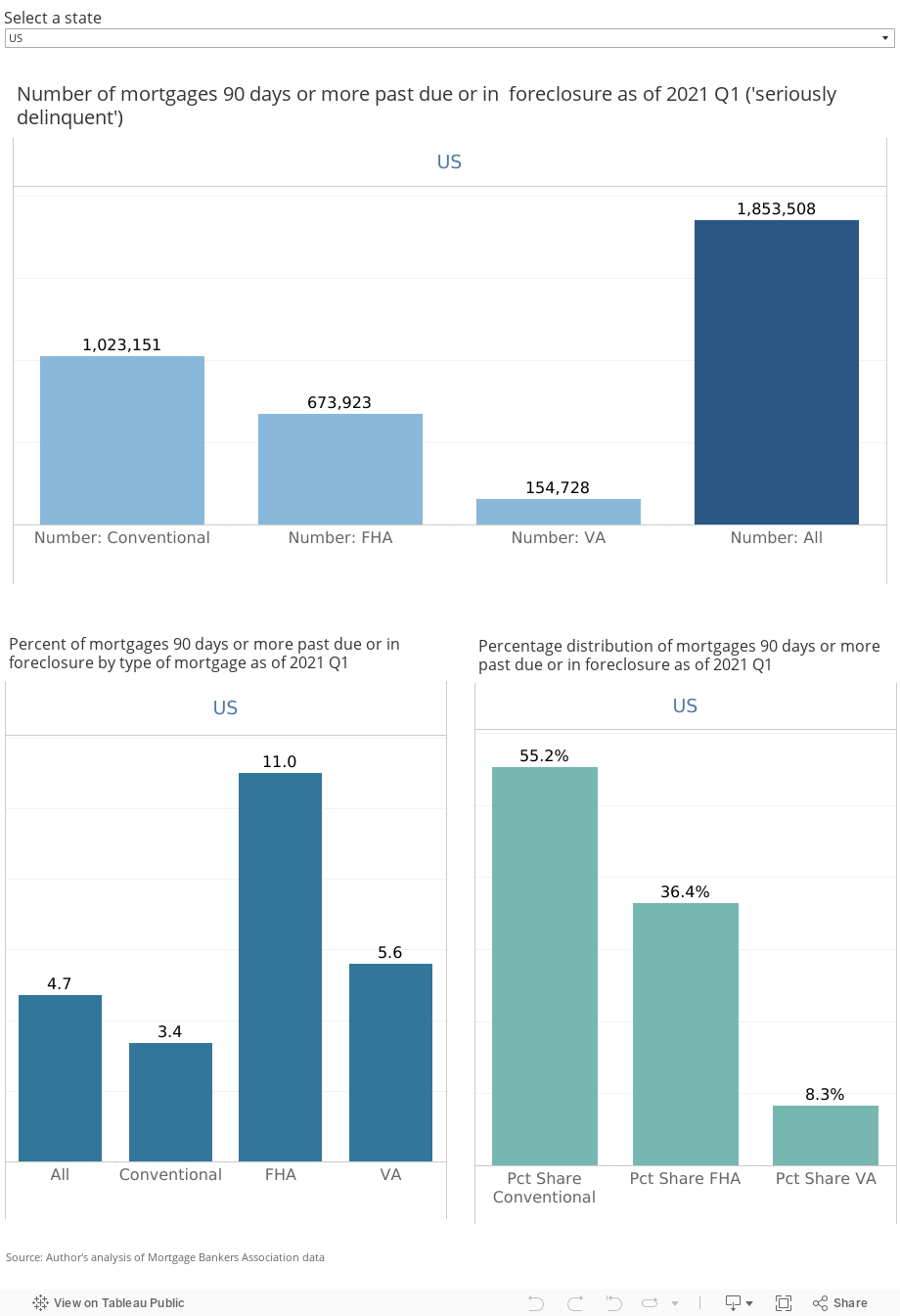

Over the 20-year period of 2000–2020, the underbuilding of single-family homes nationally totaled nearly 5 million.4 This underbuilding far outstrips the 1.85 million mortgages that are 90 or more days past due and that are in the foreclosure inventory ("seriously delinquent") as of 2021 Q1.5 In 38 states, there is an underbuilding of single-family homes compared to the level of employment during 2000–2020.

Again, not all mortgages that are in serious delinquency will end up in foreclosure, so these foreclosed homes coming into the market will not cause a glut and price declines but will help alleviate the tight housing supply and lead to slower price appreciation. The table below compares the housing underbuilding of single-family homes with mortgages in foreclosure and if 1/3, 2/3, or all get foreclosed and end up on the market. The most likely scenario is that no more than 1/3 could end up on the market given the current trend where homeowners in forbearance are using loss mitigation options to work out the repayment. Nationally, 1/3 of 1.8 million loans that are seriously delinquent amounts to about 618,000 homes or 1.3 months of supply of the current monthly sales pace of 483,333 homes.

Additional supply will slightly ease price appreciation

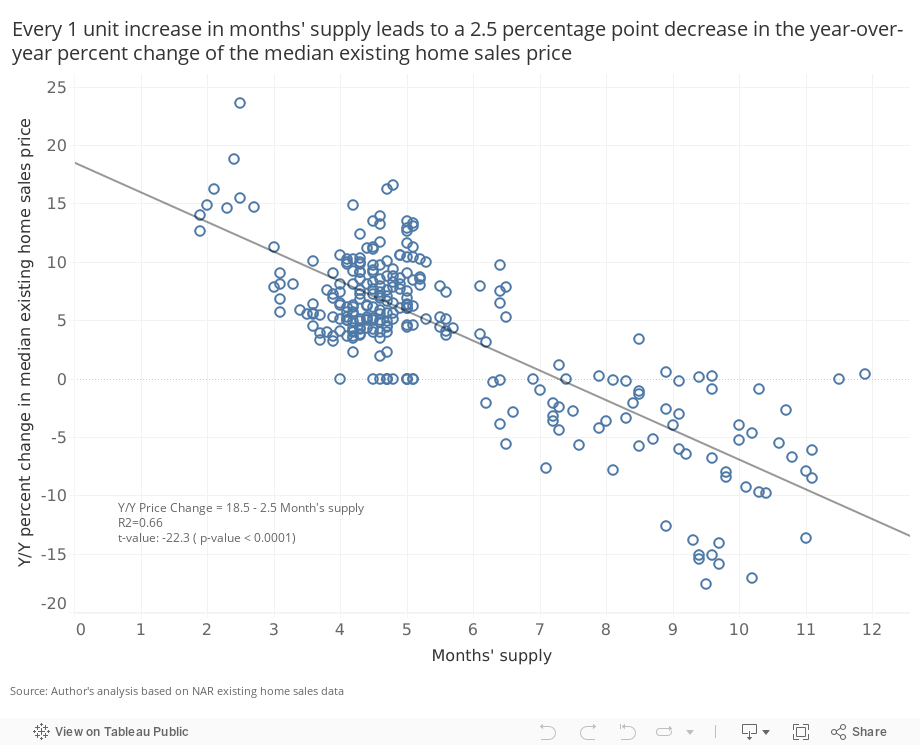

Any increase in supply from home sales will help temper some of the pressure on home sales. Based on the relationship between months' supply and the year-over-year median existing-home sales price, since 2000 every additional month of inventory relative to demand (months' supply) lowers the year-over-year price change by 2.5 percentage points.

The additional 8 days of supply (from the likely scenario that 1/3 of the 400,000 homes that are past due but not in forbearance could end up on listed) will slightly cool down prices by no more than 1 percentage point and up to as much as 2.5 percentage points if all homes are listed.

Lower income and minority groups are twice as likely to face foreclosure

While the impact of the end of the forbearance period and potential foreclosures will not likely have negative impact on supply and prices, any foreclosures will widen the already dismal homeownership gap and the wealth divide between higher and lower income groups and between minority and non-minority (White, non-Hispanic groups).

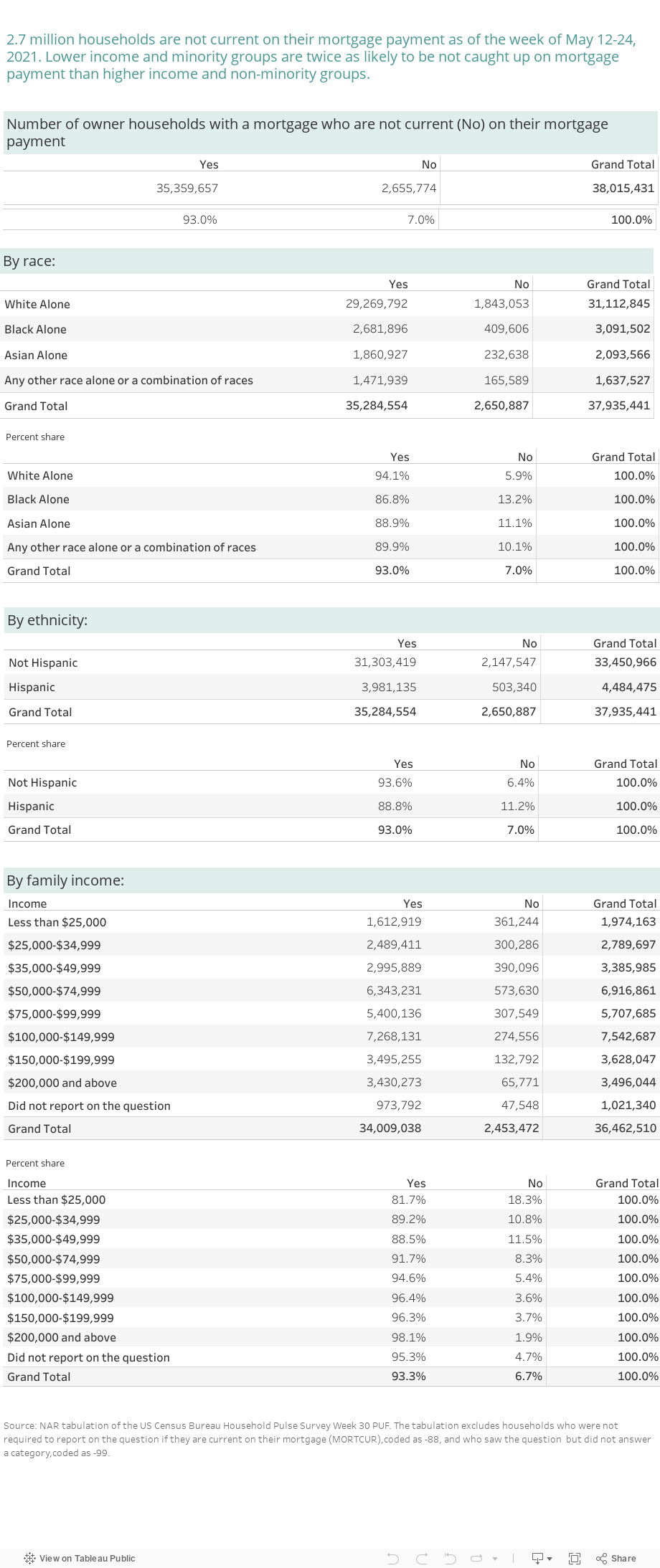

During the period May 12-24, there were 2.7 million households that were not caught up on their mortgage payment (7% of owner households with a mortgage).6 The fraction of low-income and minority groups who are not caught up on mortgage payments is twice the rate of those of higher income and the White or non-Hispanic groups which means the former face a higher risk of foreclosure. By race, 13% of Black-only households are not caught up on their mortgage compared to 7% among all households. By ethnicity, 11% of Hispanic households are not caught up on their mortgage. By income group, nearly 1 in 5 households with an income of less than $25,000 is not caught up on their mortgage payment. Across all income groups, households earning less than $50,000 account for 43% of households not caught up on mortgage payment.

FHA borrowers are thrice as likely to face foreclosure than conventional loan borrowers

By type of mortgage, homeowners with FHA and VA financing are at higher risk of foreclosure. Nationally, 11% of FHA borrowers are seriously delinquent compared to only 3.4% among conventional loan borrowers. FHA borrowers tend to be the lower-income borrowers with less than excellent credit scores, and it will be harder for them to get back into homeownership if they lose their home. As of 2021 Q1, FHA- and VA-insured mortgages accounted for nearly 45% of the 1.85 million borrowers who are seriously delinquent.

An Affordable Repayment Term for Missed Mortgage: 5% of Family Income

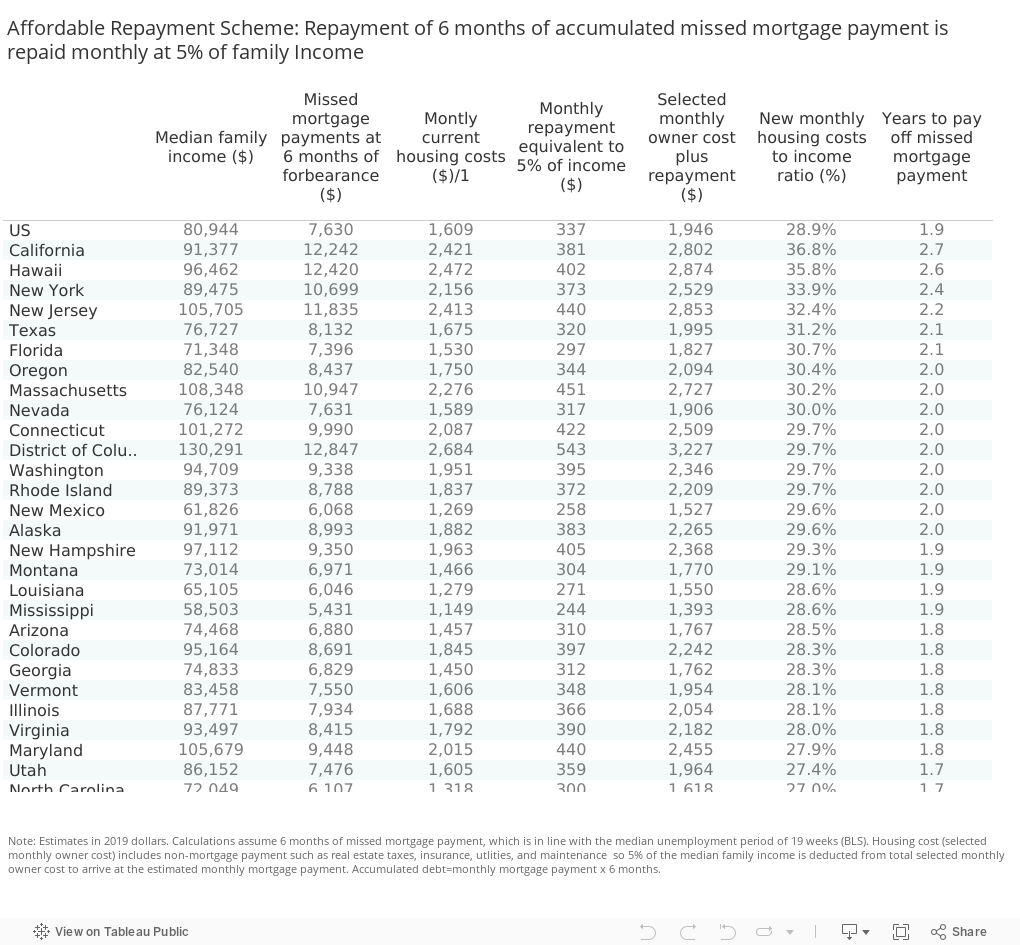

Over a 6-month period, I estimate the missed mortgage payment per household is $7,630 ($14.1 billion among the 1.8 million seriously delinquent mortgages).

To estimate the accumulated unpaid mortgage, I assumed that the mortgage payment is equal to the selected monthly owner cost7 of homeowners with a mortgage in 2019 and deduct 5% of median family income to account for non-mortgage payment expenses.8 The selected monthly owner cost among households with a mortgage in 2019 was $1,609, which yields an estimated current monthly mortgage payment of $1,272 once non-mortgage expenses (5% of family the median family income of $80,944) are deducted.

A reasonable assumption is that a borrower is likely going to seek forbearance during the period he/she is unemployed. According to the Bureau of Labor Statistics, the median duration of unemployment as of May 2021 is 19 weeks. So, over a 6-month period, the missed mortgage payment is $7,630.9

Homeowners have several options they can work out with their lenders to successfully get back on track to paying their mortgage.10 A repayment plan where the homeowner spends no more than 5% of income to catch up with the missed mortgage payment is typically affordable for homebuyers. It results in a new total housing cost of $1,946 ($1,609 + additional repayment of $337). This is equivalent to 28.9% of the median family income, which is still below the 30% threshold that will make the repayment plan a cost burden.

However, homeowners will typically pay more than 30% of their income on housing costs in California (36.8%), Hawaii (35.8%), New York (33.9%), New Jersey (32.4%), Texas (31.2%), Florida (30.7%), Oregon (30.4%), and Massachusetts (30.2%). The debt repayment will be more affordable for homeowners in these states if the repayment is less than 5% of family income.

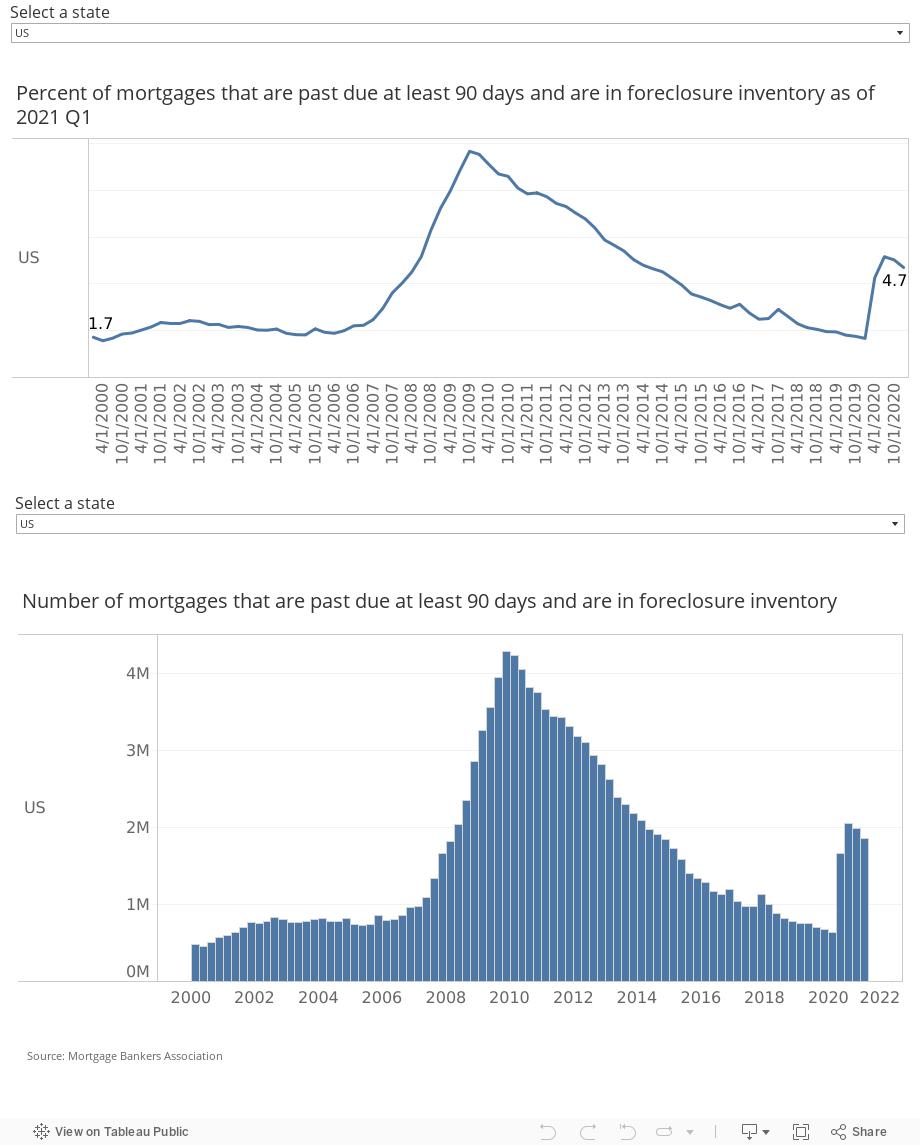

The fraction of seriously delinquent mortgages at 4.7% is not likely to surpass Great Recession rate of nearly 10%

As of 2021 Q1, the national mortgage delinquency rate11 stood at 4.7% and is just about half the peak rate of 9.7% in 2009 Q4 during the Great Recession. Only the states of Wyoming and Alaska have higher serious delinquency rates during this pandemic period than during the Great Recession. The risk of foreclosure is diminishing as the economic and job recovery continues, with 15 million of the 22 million lost non-farm payroll jobs already recovered as of May 2021.

The author thanks Lawrence Yun, NAR Chief Economist, for his suggestions on the first draft of this report.

1 The FHA eviction moratorium for all homeowners with an FHA-insured forward or Home Equity Conversion Mortgage (HECM) loan and the GSE eviction moratorium for single-family mortgages also expires on June 30, 2021.

2 From September 2020 through May 2021, the average number of mortgages in forbearance was 2.65 million, so the sales through foreclosures, short sales, or deed-in-lieu amounted to nearly 251,750 homes, or 5.7% of the 4.42 million existing-home sales during Sept 2020–May 2021.

3 15.3% of the 2.65 million average number of mortgages in forbearance from September 2020 through May 2021.

4 Underbuilding = (Change in single-family permits, 2000–2020) – (Change in non-agricultural employment/2)

5 Downloaded via Haver Analytics. Haver calculates a serious delinquency rate, which is the share of mortgages that are over 90 days past due and in the foreclosure inventory as a proportion of serviced mortgages.

6 Based on tabulation of the U.S. Census Bureau Household Pulse PUF by housing weight.

7 Selected monthly owner costs are the sum of payments for mortgages, deeds of trust, contracts to purchase, or similar debts on the property (including payments for the first mortgage, second mortgages, home equity loans, and other junior mortgages); real estate taxes; fire, hazard, and flood insurance on the property; utilities (electricity, gas, and water and sewer); and fuels (oil, coal, kerosene, wood, etc.). It also includes, where appropriate, the monthly condominium fee for condominiums and mobile home costs (installment loan payments, personal property taxes, site rent, registration fees, and license fees). U.S. Census Bureau https://www.census.gov/quickfacts/fact/note/US/HSG650219

8 The median real estate taxes (2,869) already account for 3.5% of median family income ($80,944), so I assumed that real estate taxes and other household expenses account for 5% of income. The 5% share is the same assumption that NAR uses in calculating the Housing Affordability Index. It uses 25% ratio of mortgage payment to income so that accounting for other expenses, total housing expenses will not exceed 30% of income.

9 On an aggregate basis, there were 1.8 million seriously delinquent homeowners as of the first quarter of 2021, so the estimated aggregate total debt accumulated among homeowners in forbearance totals $14.1 billion.

10 In a repayment plan, a portion of the amount owed will be added to the amount paid each month. In a deferral or partial claim, the missed payments will be paid at the end of the loan when the homeowner refinances, sells, or terminates the mortgage. In a loan modification, the payment will be reduced to an affordable amount by increasing the length of time to pay the loan. In a reinstatement, the amount is paid lump-sum but services will not require the borrower to pay lump sum; and short sales is when the homeowner sells the property for less than the mortgage amount to avoid foreclosure. Consumer Financial Protection Bureau, https://www.consumerfinance.gov/ask-cfpb/if-i-cant-pay-my-mortgage-loan-what-are-my-options-en-268/

11 Downloaded via Haver Analytics. Haver calculates a serious delinquency rate, which is the share of mortgages that are over 90 days past due and in the foreclosure inventory as a proportion of serviced mortgages.