One major impact of the coronavirus pandemic is on where people are deciding to live, work, and play. Housing affordability, the desire to live in less dense areas, and in larger homes with the opportunity to work from home, and the demand from millennials as they start to form households and raise families are important factors that play into the decision of where to live and buy a home.

As of August 2021, housing market indicators show outlying counties of metropolitan or micropolitan areas are experiencing more robust housing demand compared to central counties, an indication that housing demand is dispersing outwards from the central counties of metropolitan or micropolitan areas to outlying counties.

Market statistics in outlying and central counties of metropolitan areas

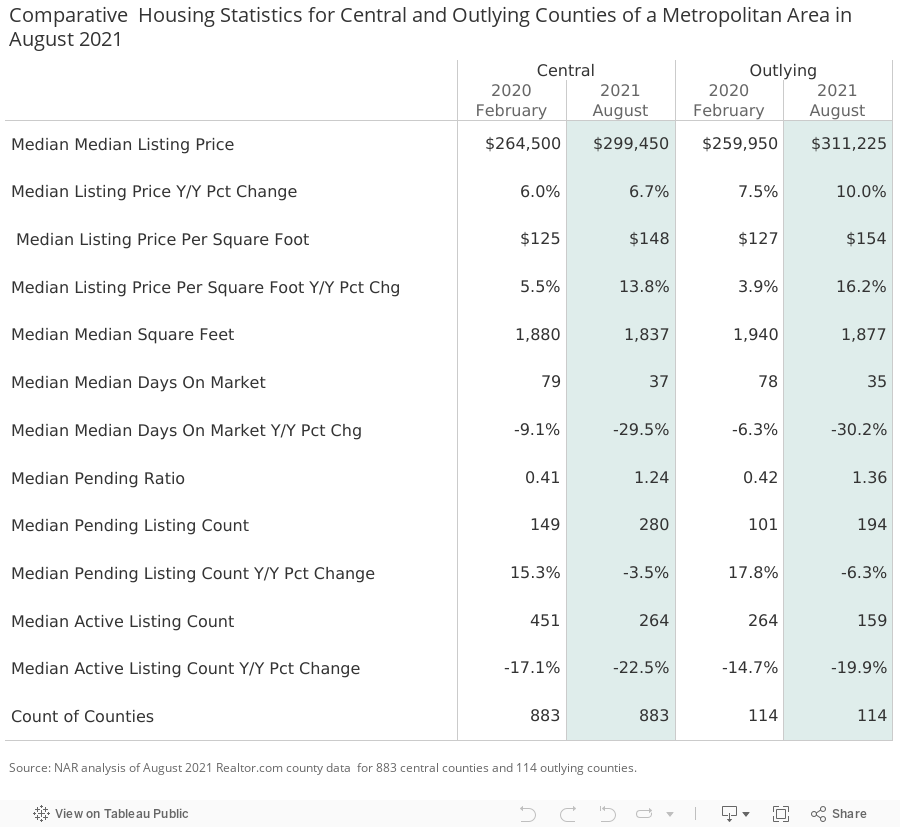

As of August 2021, home listings data on realtor.com® in 883 central counties and 114 outlying counties indicate stronger demand for housing in outlying counties than in the central counties of metropolitan areas. However, both outlying and central counties are performing remarkably well compared to pre-pandemic conditions (February 2020).

Faster price appreciation in outlying counties

In August, the median listing price in outlying counties rose 10% from one year ago, while the median listing price in central counties rose at a slower pace of 6.7%. In fact, the median listing price in the outlying counties was slightly higher at $311,225 compared to the median listing price of $299,450 in central counties. The median listing price per square foot is also higher in the outlying counties, at $154/sf compared to $148/sf in the central counties.

Faster days on market in outlying counties

Properties are selling faster in outlying counties, at 35 days, compared to 37 days in central counties. Days on market have decreased in both central and outlying counties; properties sold in 53 days in central counties and 52 days in outlying counties one year ago.

Higher ratio of pending listings to active listings in outlying counties

The ratio of pending listings to active listings is another indicator of demand relative to supply. In outlying counties, there were 1.4 pending listings per active listing compared to 1.2 pending listings per active listing in central counties.

Active listings are down in both central and outlying counties

Supply is running below year-ago levels in both outlying and central counties, with a stronger decline of 23% year-over-year in central counties compared to a 20% year-over-year decline in outlying counties.

Bigger square footage in outlying counties

One reason for the preference of a home in outlying counties is the availability of bigger homes and more yard space. In terms of home square footage, the median square footage of homes listed in outlying counties was 1,877 square feet, which is 40 square feet larger than the median square footage of 1,837 square feet in central counties. That 40 square feet gives extra storage space or can serve as a work area.

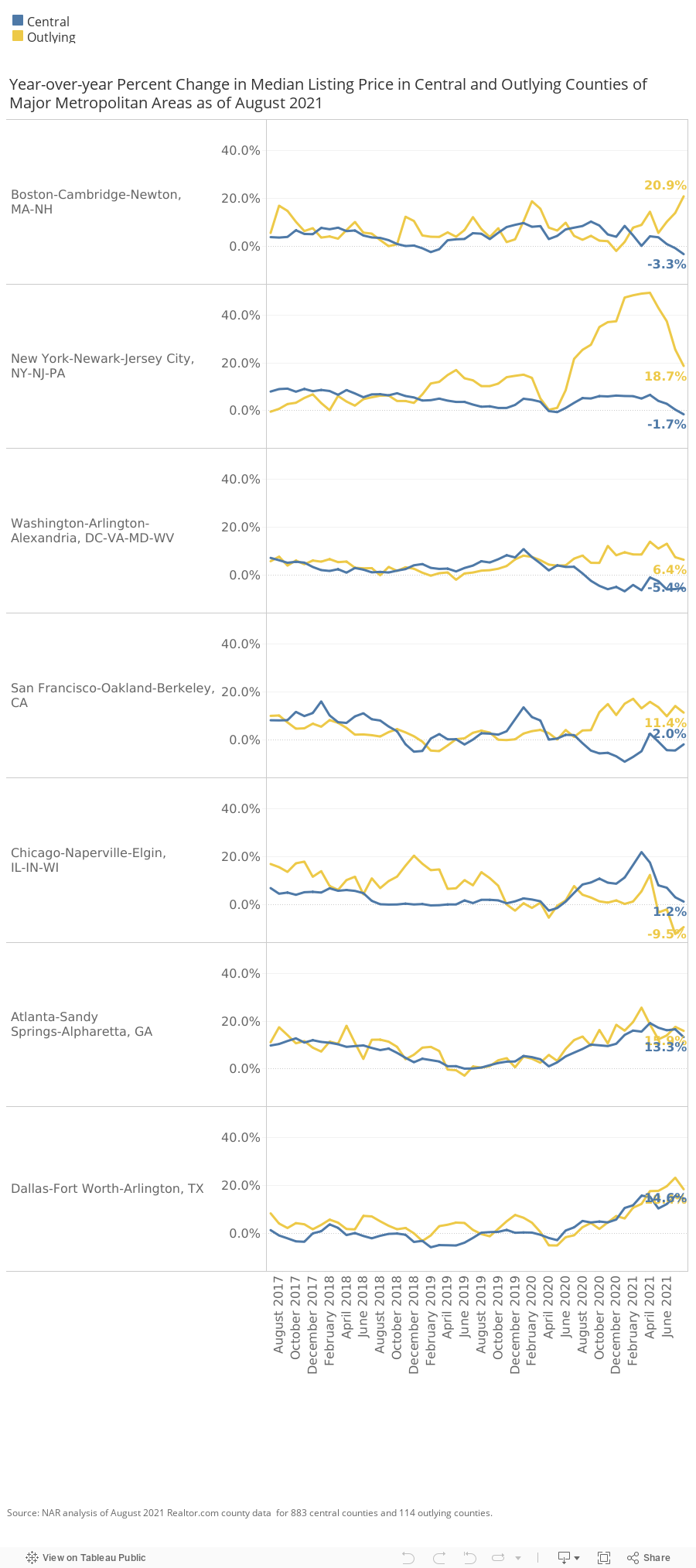

Median listing prices in selected metro areas

Affordability is clearly a driver of the demand for homes in outlying areas. Homes in outlying counties have been generally less expensive than in central counties. In August, the median list price in outlying counties has increased at a faster pace than in central counties, except in the metro area of Chicago.

Drilling down into the major metro areas for which there is at least one outlying or central county tracked by realtor.com®, median listing prices are rising at a faster pace in the outlying counties compared to the central counties.

In the New York-Newark-Jersey City area, the median list price in the central counties is down 1.7% year-over-year as of August 2021 due to price declines in central counties like Hudson (-11.9%), Kings (-11.8%), and Queens (-5%). However, prices are rising strongly in the central counties like Suffolk (12.3%), Sussex (11.9%), and Ocean, New Jersey (9.5%). The only outlying county for this metro area that is tracked by realtor.com® is Pike, Pennsylvania, where the median list price rose 18.7% year-over-year, the highest price growth in this metro area.

In the Washington-Arlington-Alexandria metro area, list prices in August 2021 were down in the District of Columbia (-14.3%) and the central counties of Fairfax (-14.5%) and Montgomery (-9.3%). However, list prices are rising strongly in the outlying counties of Stafford, Virginia (15.8%); Frederick, Maryland (11.4%); Spotsylvania (8.1%), and Jefferson (7.2%).

The Chicago-Naperville-Elgin metro area is bucking the trend where the median listing price has fallen in the outlying counties by 9.5% while the median list price among central counties is slightly up by 1.2% due to rising list prices in central counties such as Kendall (11.8%), Lake (11%), and Will (6.5%). However, in Cook County, where Chicago is, the median listing price is down 5.8%.

In the San Francisco-Oakland-Berkeley metro area, the median list price in outlying counties is up 11.4%, which is due to Contra Costa (11.4%). In San Francisco, the median list price is down (-7.4%) as well as in Marin (-6.4%). San Francisco is a county that has been taking a long time to recover because its workforce is heavily concentrated in technology jobs. Nationally, 50% of computer/mathematical workers are teleworking as of June 2021 compared to 14% among all occupations. However, the central counties of Alameda (8.4%) and San Mateo (2.6%), which are contiguous to San Francisco county, had higher median list prices as of August compared to one year ago.

In the Boston-Cambridge-Newton metro area, the median list price is down 3.3% year-over-year in the central counties, including in Suffolk County where Boston is located (-6%). The median list price is up 20.9% in the outlying county of Strafford, New Hampshire.

In the Dallas-Fort Worth-Arlington metro area, the median list price in central counties is up 14.6% while the median list price in outlying counties is up 18.4%. In the central county of Dallas, the median list price is down (-4.6%), while the median list price is up year-over-year in all other central and outlying counties.

Methodology and data source (realtor.com®)

For this analysis, I used realtor.com® home listings summary statistics in 1,000 counties, of which 883 are central counties and 114 counties are outlying counties of a metropolitan or micropolitan area based on the U.S. Census Bureau March 2020 delineation.1 According to the US Census Bureau, "a central county is a county or counties of a Core Based Statistical Area (metropolitan statistical area or micropolitan statistical area) containing a substantial portion of an urbanized area or urban cluster or both, and to and from which commuting is measured to determine qualification of outlying counties. An outlying county is a county that qualifies for inclusion in a core-based statistical area on the basis of commuting ties with the CBSA's central county or counties."2

1 I categorized the realtor.com® 1,000 metro areas as central or outlying counties based on the March 2020 US Office of Management and Budget Bulletin delineation; https://www.census.gov/geographies/reference-files/time-series/demo/metro-micro/delineation-files.html. The three counties that realtor.com® tracks that are not in the March 2020 OMB Bulletin and could not therefore be classified into central our outlying counties are Van Buren, Michigan; Barry, Michigan; and Le Flore, Oklahoma.

A central county is a county or counties of a Core Based Statistical Area containing a substantial portion of an urbanized area or urban cluster or both, and to and from which commuting is measured to determine qualification of outlying counties. An outlying county is a county that qualifies for inclusion in a Core Based Statistical Area on the basis of commuting ties with the Core Based Statistical Area's central county or counties. A county qualifies as outlying under the following circumstances: (1) one-quarter or more of the employed residents work in the central counties of the metropolitan or micropolitan statistical area, or (2) one-quarter or more of the employment is composed of workers who live in the central counties. Furthermore, outlying counties also include the counties of any smaller metropolitan or micropolitan statistical area that are adjacent to the metropolitan or micropolitan statistical area and merge with it. https://www.census.gov/programs-surveys/metro-micro/about/glossary.html

2 To note, outlying counties are not the same as "suburbs" which are popularly considered as places that border the cities or towns and have strong economic relationship (people live there but work in the city). For example, in the case of the Washington- Arlington-Alexandria metro area, both Fairfax County and the District of Columbia are considered central counties, although the popular notion is to consider Fairfax County as a suburb of Washington, DC.