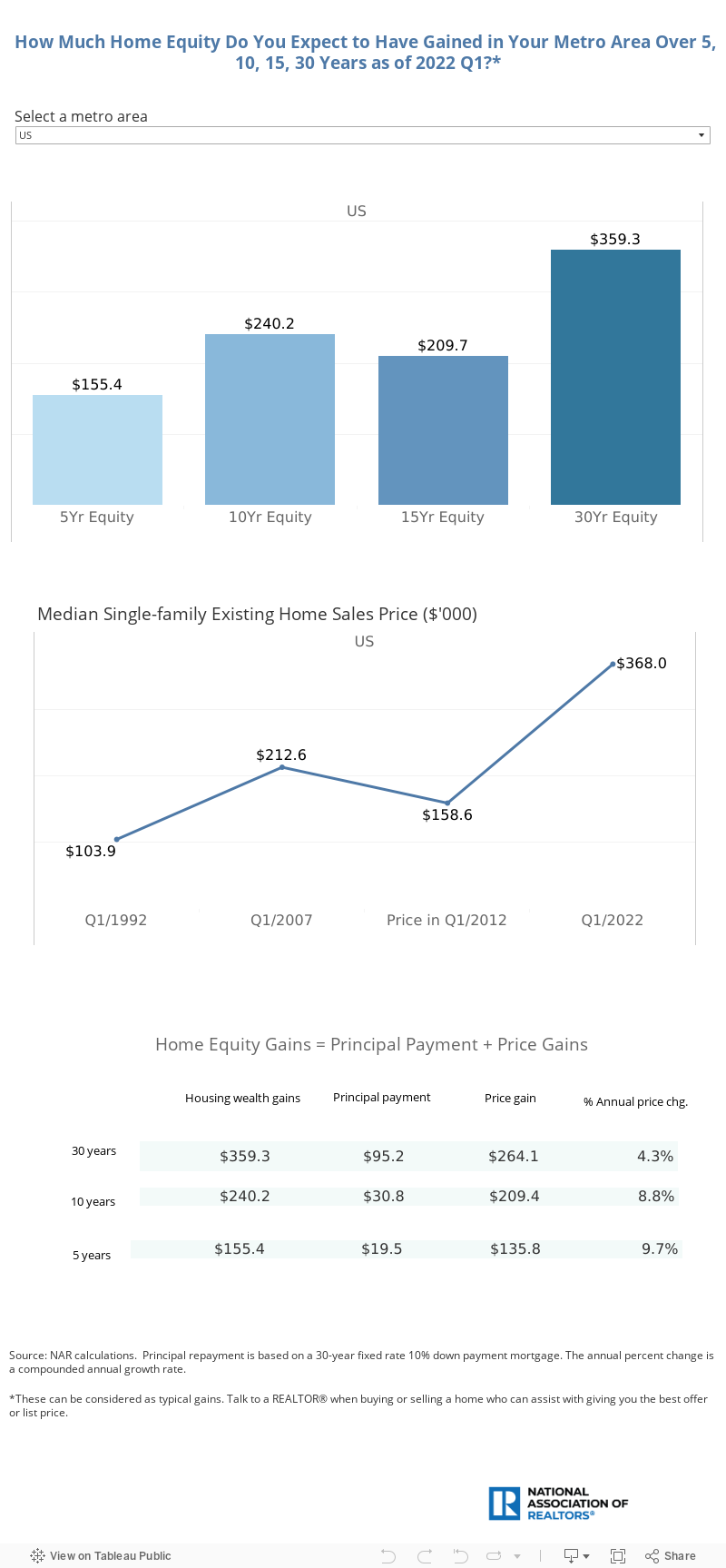

Homeowners Typically Built Housing Wealth of $240,200 Over 10 years

Homeownership is the largest source of wealth among families, with the median value of the primary residence worth about ten times the median value of financial assets held by families.1 Home equity gains are built up through price appreciation and by paying off the mortgage through principal payments.

Over the past 10 years, at the national level, a homeowner who purchased a single-family existing home would have gained $229,400 in home equity if the home were sold at the median sales price of $360,700 in 2021 Q4. Home prices rose at a strong annual pace of 8.8%, yielding a pure gain due to a price appreciation of $209,400.

Home prices rose have increased even more steeply over the past five years, at an annual pace of 9.7%. A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.

The equity gains will depend on the home's characteristics but over a 5- or 10-year period, the characteristics of a typical home will likely not have changed much, so the change in the median sales price is still a good indicator of the typical equity gains due to price appreciation. However, talk to a REALTOR® when buying or selling a home who can assist with giving you the best offer or list price on your home.

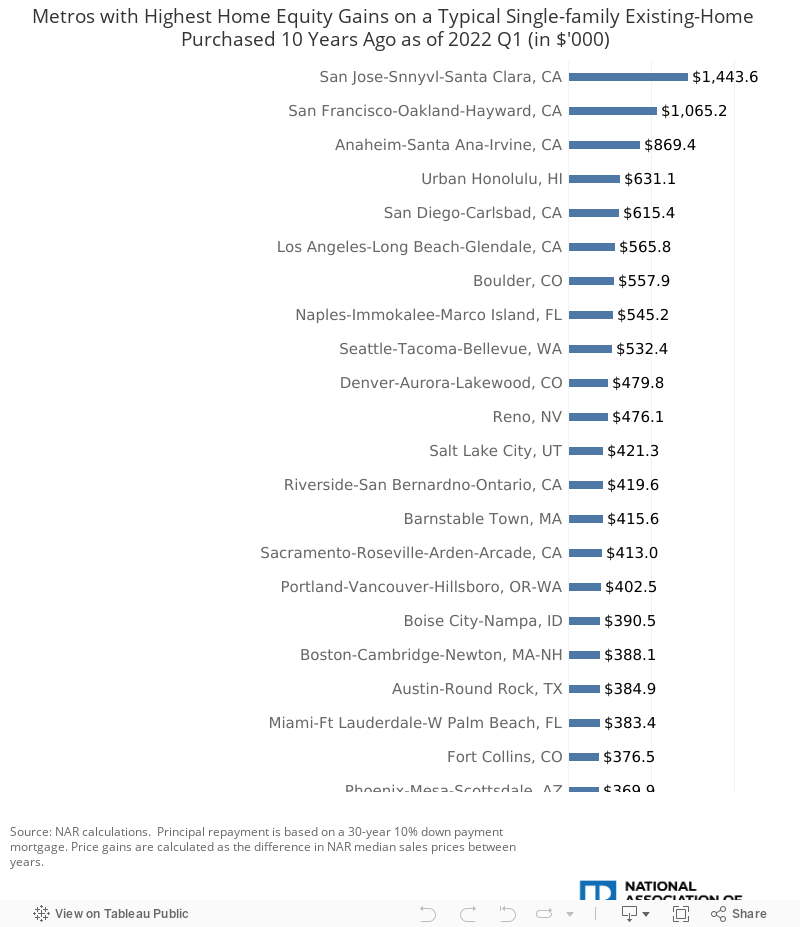

The West Region Had 15 of the Top 20 Metros With Largest Home Equity Gains

The West region had 15 of the top 20 metro areas where homeowners built up the largest home equity, mainly because of the strong price appreciation. Specifically, California had seven of the top 20 metros and had the top three metro areas with the largest home equity buildup: San Jose ($1.4 million), San Francisco ($1.1 million), and Anaheim ($869,400).

Large Home Equity Gains Not Likely to Be Dissipated Even as Mortgage Rates Rise

With mortgage rates rising, there is concern that demand and prices will fall. NAR expects home prices to continue rising, although at a slower pace of nearly 10% by the end of 2022 and about 5% for 2023.

Home prices are not likely to fall as they did during the Great Recession because there is no incentive for home sellers to sell their homes at a loss. The level of adjustable-rate mortgages is low, with ARMs accounting for less than 10% of mortgage applications since 2008 compared to as high as 35% during 2004-2005. Supply conditions are still very tight, with the inventory of homes for sale equivalent to 2.2 months as of April 2022. Home construction costs are also still rising, up 18% year-over-year as of April, according to the U.S. Census Bureau’s construction price index.

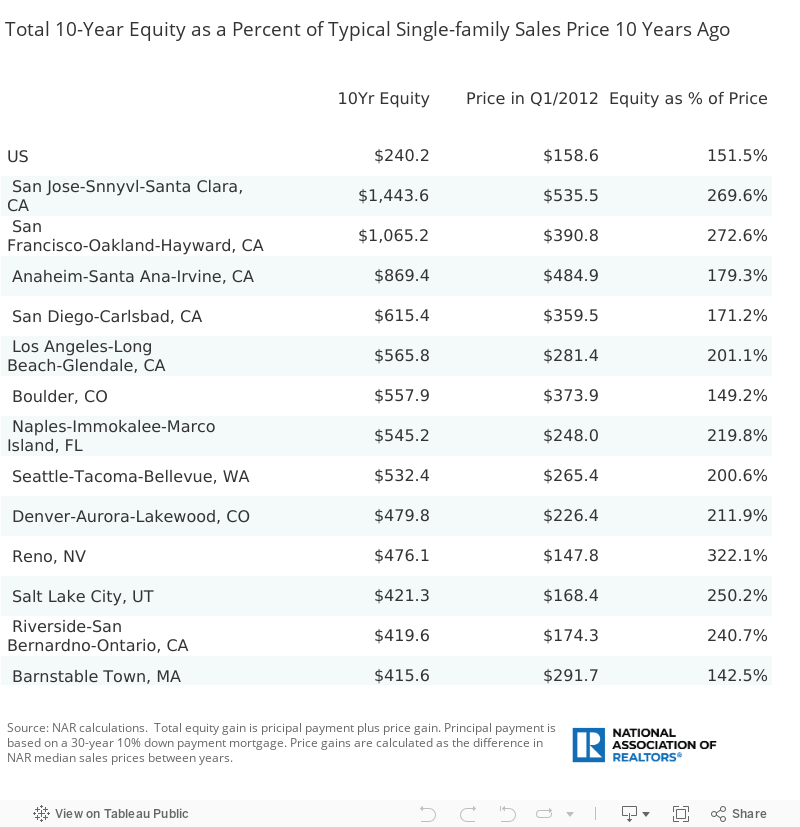

However, even if home prices were to fall, it will take a massive dip in prices to wipe out home equity gains. Nationally, homeowners have typically built up $240,200 in total home equity gains through paying down the debt and the home price appreciation gains. At the current median single-family sales price of 360,700 in 2022 Q1, that gain amount is equivalent to 1.5x the median single-family sales price 10 years ago of $158,600. In high-cost areas like San Jose, the gains in home equity of $1.4 million are 2.7x the price of $535,500 10 years ago. So even if home prices were to fall and sellers had to sell their homes, they will likely still not have to sell at a loss relative to the price at which they bought the home but will experience smaller gains.

1 Source: Federal Reserve Board of New York, Survey of Consumer Finances. In 2019, the median value of the primary residence was $225,000 and the median value of any financial asset held by families (renter or homeowner) was $25,700. Even among homeowners, the median value of their financial asset was just at $63,400.