")

The conversion of vacant office space for residential use is one way to increase the supply of housing, specifically multifamily rental housing. However, the low differential between Class B office rent and Class A residential rent and rising construction costs create headwinds for the conversion of vacant office space in major metro areas, particularly in San Francisco, Washington DC, and New York. Chicago has the best current potential for office-to-residential conversion.

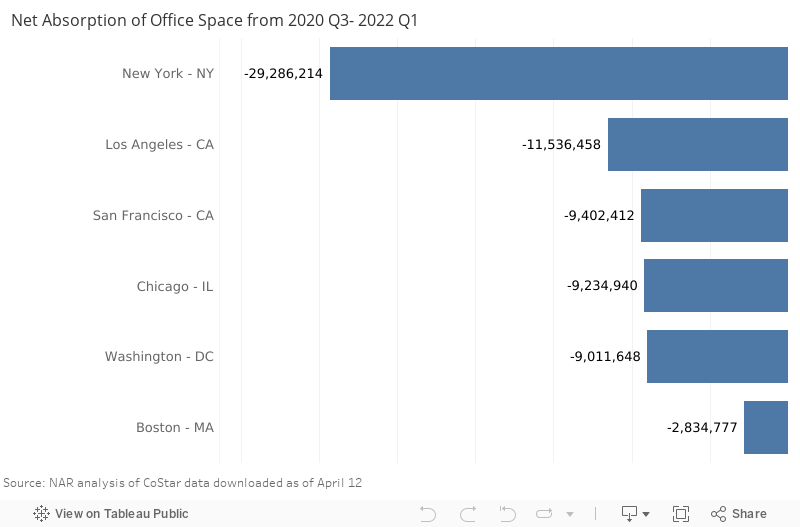

Major metro areas still have not recovered from the loss in office occupancy during 2020

As of the second quarter of 2022, office occupancy is down by nearly 115 million square feet (MSF) compared to 2020 Q1. The six major commercial metro areas are still suffering from severe losses in office occupancy: New York (-29.2 MSF), Los Angeles (11.5 MSF), San Francisco (9.4 MSF), Chicago (9.2 MSF), Washington, DC (9 MSF), and Boston (2.8 MSF).

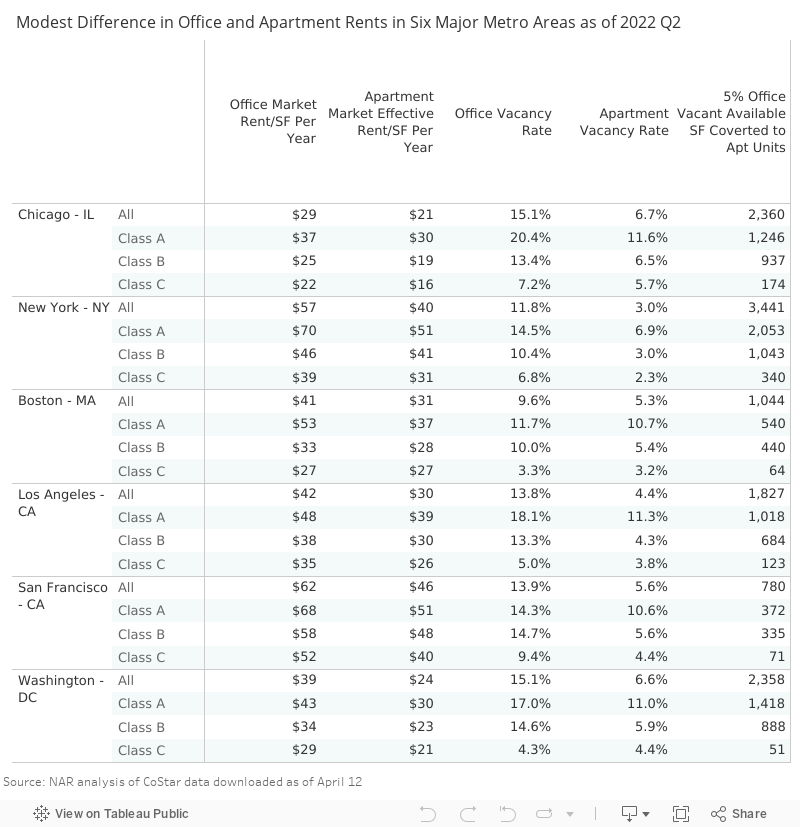

Modest office and apartment rent differentials in six major markets

Many factors determine the feasibility of converting from an office to a residential building1 but one key determinant is the difference between current office and apartment rents and the outlook for rents and vacancy rates, as documented in a NAR study.

The table below shows modest gains in rent from the conversion of office to residential use. These modest gains can be offset by the cost of construction, which is rising 17% year-over-year nationally.2

Compared to the other metro areas, Chicago has the best potential for office-to-residential conversion based on rent differentials. In the metro area in Chicago, the office rent on Class B is still higher at $25/SF compared to $30/SF for a Class A apartment building, or a 20% gain.

In New York, the asking rent/SF on Class B office units (we consider Class B because there is more vacant space for Class B than Class C) is $46, compared to $51/SF for a Class A unit, or 11% more for an apartment unit. However, rising construction costs of 17% can be a disincentive for an office-to-residential conversion as it increases the period to make a return on the investment.

In Boston, the office rent for Class C units is $33/SF, compared to $37/SF for an apartment unit, or a 12% gain for an office-to-residential conversion. This rent differential is also lower than the rising cost of construction. Moreover, Boston is experiencing strong demand for commercial space from life sciences companies, so the greater potential for conversion is from an office to a lab science facility.

Meanwhile, in both San Francisco and Washington DC, the office rents of Class B units are still higher than the rent on Class A residential units, which greatly discourages office-to-residential conversion.

In San Francisco, Class B office rents of $58/SF have to fall by 13% to be on par with the $51/SF of Class A apartment rent.

In the District of Columbia, Class B office rents of $34/SF also have to fall by 13% to be on par with the $30/SF of Class A apartment rent.

Financial support from state/local authorities can make office-to-residential conversions feasible

Because there is still a low market-driven incentive for office-to-residential conversion, such conversions—especially to provide affordable housing—are likely to need financial support from the state or local government or even the federal government. For example, as documented in NAR’s study on conversions, the conversion of an office building for use as a permanent homeless shelter (Cordell Place) received an $8 million loan from Montgomery County, MD. In the conversion of an office building into efficiency unit apartments (Octave 1320), Montgomery County invested $4.1 million.

1 Office buildings with deep floor plate are harder and costlier to convert than buildings as the interior space does not have access to natural light and windows. Older buildings also have more potential for conversion as they will need to be remodeled anyway to compete with newer stock.

2 Source: US Census Bureau Construction Price Index for a single-family house as of February 2022.