")

Please note: The data visualization embeds on this page are best viewed on a laptop or desktop computer.

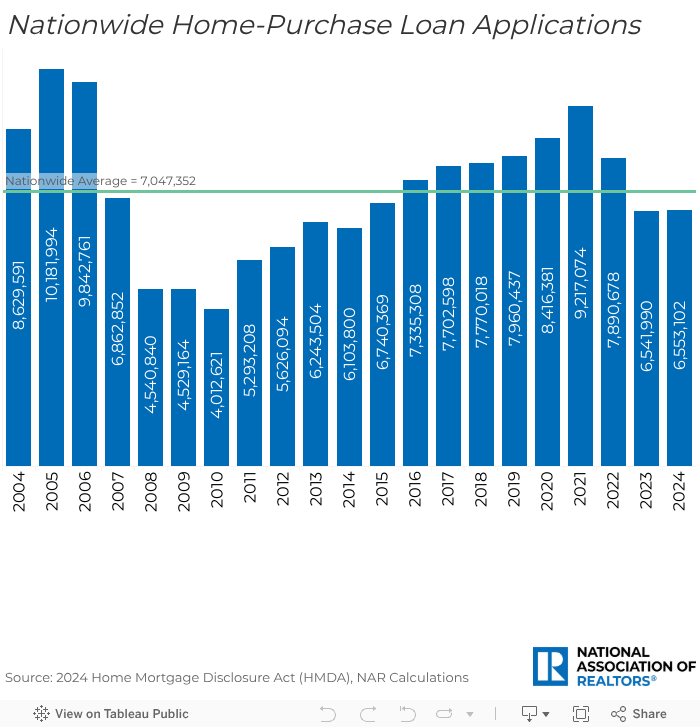

Following a historic low in home-purchase mortgage applications in 2023, new data from the Home Mortgage Disclosure Act (HMDA) suggests that demand for home buying is on the rise again.

Between 2023 and 2024, the number of home-purchase loan applications increased by 0.2%, rising from 6.54 million to 6.55 million nationwide. This growth resulted in 3.5 million loans originating in 2024, up from 3.4 million in 2023. In comparison, the U.S. lost 1.3 million home-purchase loan applications between 2022 and 2023, leading to over 900,000 fewer originations in 2023. Although the increase in 2024 is modest compared to the national average of approximately 7 million over the last two decades, it provides hope for market recovery. This is especially promising given that mortgage rates have remained stable since the end of 2023 and housing inventory has been increasing.

In 2024, the typical applicant had a median income of $107,682, sought a median loan amount of $296,871, and aimed to buy a property with a median value of $365,324.

Home-Purchase Loan Applications

The number of applications can provide insight into whether housing demand is strong or weak in a specific area. In 2024, about 65% of the major metropolitan areas experienced growth in the number of loan applications:

- The most notable improvement was seen in Appleton, WI, where the number of applications grew by 19%.

- Rounding out the top three, Appleton was followed by two other areas in Wisconsin: Oshkosh-Neenah with a 16.3% increase in applications and Fond du Lac with 14.5% growth.

- San Luis Obispo-Paso Robles, in California, experienced a 13.7% increase in applications (sixth highest), after experiencing a decrease of approximately 30% in 2023.

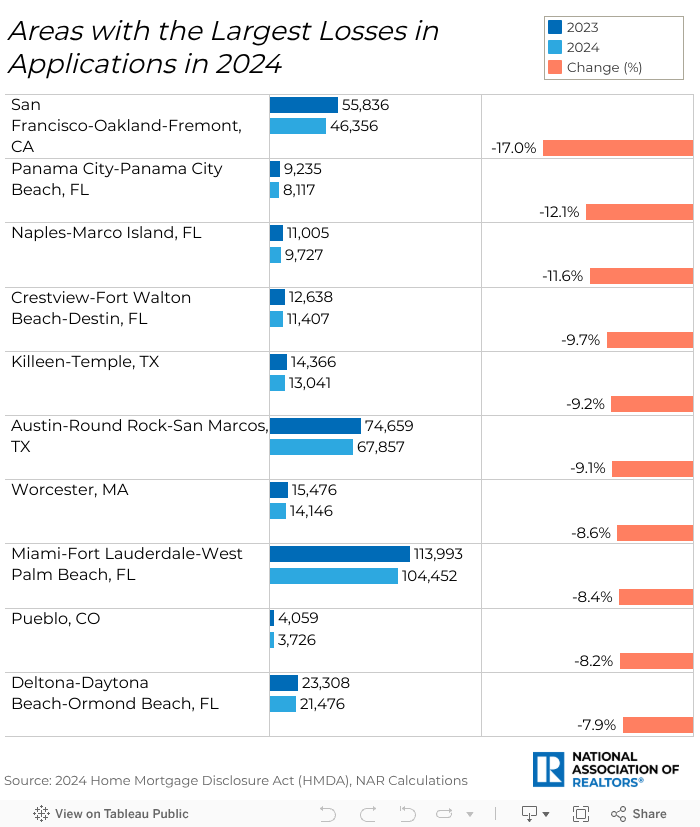

Despite the notable improvements in many areas, 76 of the 216 major metropolitan areas still experienced declining application rates:

- The largest loss was a 17% decrease in the San Francisco-Oakland-Fremont area in the Bay Area.

- Other notable declines were seen in Florida: a 12.1% decrease in applications in Panama City; a 11.6% decrease in the Naples-Marco Island area; and a decrease of 8.4% in applications in Miami-Fort Lauderdale-West Palm Beach.

- Overall, five of the top 10 areas with the largest losses were in Florida.

Mortgage Interest Rates

Mortgage rates have been steady at 6.5%-7% since December 2023, with the 2024 average interest rate for a home-purchase loan at 6.6%. Information on interest rates across metropolitan areas can provide insight into the local economy and identify emerging markets.

- The largest rate increase occurred in San Francisco-Oakland-Fremont, CA, where rates rose by 0.9 percentage points (from 5.7% to 6.6%), potentially explaining the significant decline in applications in the area.

- It was followed by San Jose-Sunnyvale-Santa Clara, CA, where mortgage interest rates increased by 0.5 percentage points.

- In Boston-Cambridge-Newton, MA-NH, Pittsfield, MA, and Bridgeport-Stamford-Danbury, CT, mortgage rates increased by 0.4 percentage points each.

- In large areas—such as Los Angeles-Long Beach-Anaheim, CA, and New York-Newark-Jersey City, NY-NJ—rates decreased by 0.4 and 0.3 percentage points, respectively.

- The largest rate decrease occurred in Kennewick-Richland, WA, and in Albuquerque, NM, where the average interest rate decreased by 0.24 percentage points in each.

- Mortgage interest rates in Lakeland-Winter Haven, FL, declined by 0.17 percentage points, which may have contributed to the area becoming the third fastest-growing metropolitan area in the country in 2024.

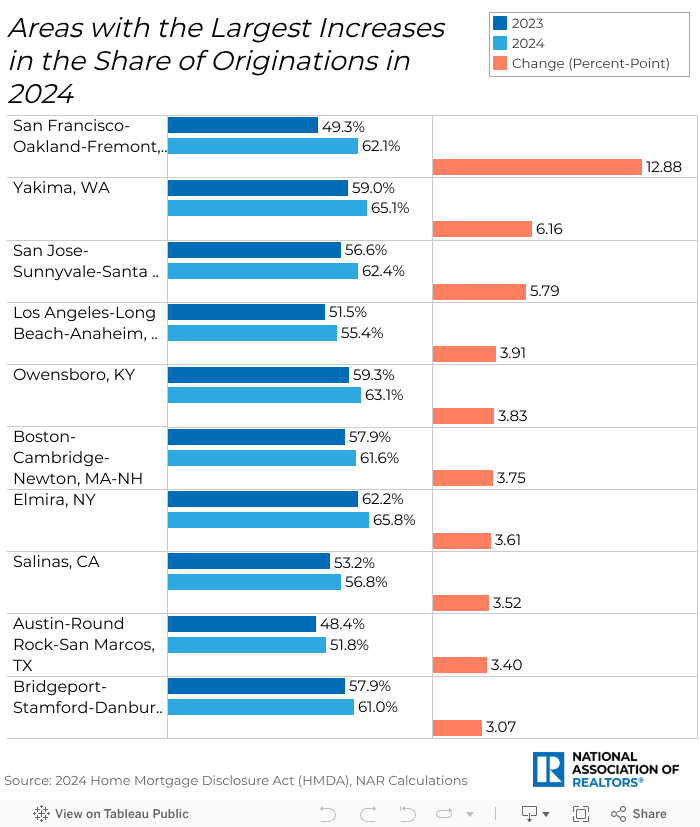

Share of Applications Turning Into Home Purchase Loans

Not all applications result in mortgages; in 2024, approximately 54% of applications were converted into home-purchase loans. The share of loan originations reflects households' ability to secure financing in a specific area.

- The San Francisco-Oakland-Fremont area in California saw the largest increase in the share of home-purchase loan originations between 2023 and 2024, at 12.9 percentage points.

- Following the Bay Area were Yakima, WA, with an increase of 6.2 percentage points, and San Jose-Sunnyvale-Santa Clara, CA, with an increase of 5.8 percentage points.

- Notably, four metro areas in California saw a significant rise in originations in 2024: San Francisco-Oakland-Fremont (12.9), San Jose-Sunnyvale-Santa Clara (5.8), Los Angeles-Long Beach-Anaheim (3.9), and Salinas (3.5).

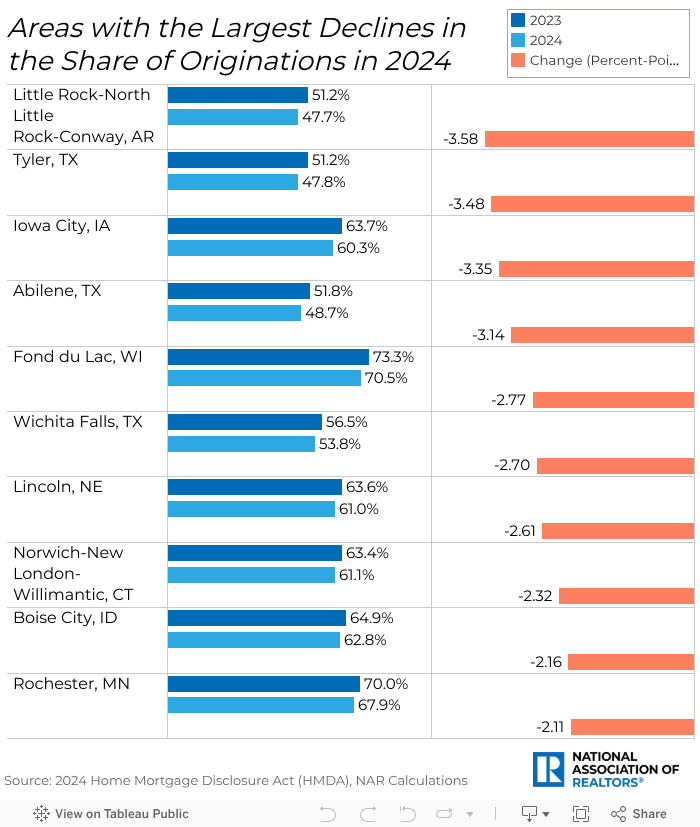

Last year, 112 of the metropolitan areas we observed experienced a rise in the share of originations. However, some areas experienced a decline in the share, most notably:

- Little Rock-North Little Rock-Conway, AR, whose share of originations declined by 3.6 percentage points, from 51.2% in 2023 to 47.4% in 2024.

- It was followed by Tyler, TX (-3.5), Iowa City, IA (-3.3), and Abilene, TX (-3.1).

Between 2022 and 2023, rising mortgage rates and increasing property prices made it challenging for many potential buyers to enter the market. As mentioned earlier, 2023 saw a historically low number of home-purchase mortgage applications, slightly above the levels observed in 2014. Nevertheless, NAR predicted that if mortgage interest rates remain below the 7% benchmark, we will see an increase in both applications and origination rates. Indeed, 2024 marked a turning point for households seeking a loan. Mortgage interest rates have been relatively stable, remaining in a consistent range for over a year now. This gave many home buyers the opportunity to plan, shop, and apply for a loan without surprises or fear of missing out on a lower rate. Now that rates are steady, potential buyers will watch out for other factors, such as median home prices and job availability in their desired areas.

For a more detailed breakdown of HMDA data by metropolitan area, visit NAR's Metro Market Statistics Dashboard (member login required): https://www.nar.realtor/research-and-statistics/housing-statistics/metro-market-statistics

Advertisement

Anat Nusinovich

Anat Nusinovich is an economist for the National Association of REALTORS®.