")

A home’s title may be a lesser-known detail of the real estate transaction, but it can cause a home sale to fall apart. Ask any real estate agent whose client has tried to close on a home without a “free and clear” title—meaning the property doesn’t have any liens or other ownership disputes. As the American Land Title Association points out, even President Abraham Lincoln’s family lost two homes due to title issues.

It can happen to anyone.

Title insurance is like an extra safety net protecting homeowners from potential property issues that could arise over the course of ownership. This could include claim disputes or unpaid liens from previous owners, or even clerical errors in public property records.

Title companies estimate that 36% of real estate transactions involve complex title issues that need to be resolved prior to closing, according to NDP Analytics, an economics research firm.

Real estate professionals can play a critical role in educating their clients about what title insurance is and why it’s essential to a smooth and secure transfer of a property.

How Much Does Title Insurance Cost?

Lenders typically require a buyer to purchase title insurance during the mortgage process. Title insurance protects the lender’s investment in case any issues arise that could affect their ability to collect on the loan later.

Title insurance is often an added cost when purchasing a home, and real estate professionals can help their clients plan ahead. Title insurance costs can vary, but the average is 0.42% of the property’s purchase price, according to Fannie Mae. (To estimate costs, First American Title offers a title insurance calculator.) This one-time payment can typically be rolled into closing costs.

In some areas, it may be customary for home sellers to pay for title insurance on the buyer’s behalf. Title insurance can be a point of negotiation in a real estate transaction.

Real estate professionals should be prepared to respond to buyers’ questions and present title insurance as an important financial piece of a secure real estate transaction, which also includes managing escrow accounts, earnest money deposits and more.

How to Shop for Title Insurance

- Gather quotes from multiple companies. There are several websites to begin a search for title insurance, including Closing.com, EasyTitleQuote.com and FreeTitleQuote.com. Also, buyers may ask their lender or real estate agent for recommendations.

- Ask about any extra fees as well as discounts that may be offered. Companies may offer discounts if the home has been resold within only a few years of the last purchase.

- Check that the title insurance company has a favorable Financial Stability Rating® with Demotech, Inc., the leading title insurance rating company.

Understanding Title Insurance: What It Is and How It Works

Title insurance is a key component of a real estate transaction, and it’s important to be aware of common terms.

Title Insurance Glossary

- Abstract of Title: This is a summary of the public records detailing the property’s ownership history. It could include past owners, mortgages, liens and any legal issues attached to the property over the years.

- Chain of Title: This shows the sequence of ownership for the property, tracing the transfer of title from the original owner to the current owner.

- Title defect: Also called “cloud on title,” this refers to any issue or problem uncovered in the property’s ownership records that could potentially impact the buyer’s right to purchase the home. Title defect issues could include unsettled claims from previous owners, forged signatures on documents, or unresolved liens and unpaid taxes.

- Lein: This refers to a claim or legal right that is brought against the property. It’s often used to describe a collateral for a debt. A lien can delay a home sale if it isn’t paid off to settle the previous debt prior to closing.

- Title search: This is the process of examining public records to verify the chain of title and identify any potential ownership issues, claims or disputes against the property. This will be conducted prior to a home sale.

- Escrow account: This is a neutral third-party account where funds—such as the buyer’s earnest money deposit, closing costs or loan funds—are held during a real estate transaction. The escrow account helps ensure all the finances involved in the transaction are securely handled before the property’s title is transferred to a new owner.

- Indemnity: This is a legal agreement that protects the title insurance policyholder from financial loss if title defects are found. Indemnity could be for the buyer or the lender, depending on the type of title insurance.

- Survey: This is a formal measurement of a property’s boundaries. A survey of the property can uncover issues like encroachments on property lines or easements (rights others have to use part of the property). Boundary disputes can lead to title issues.

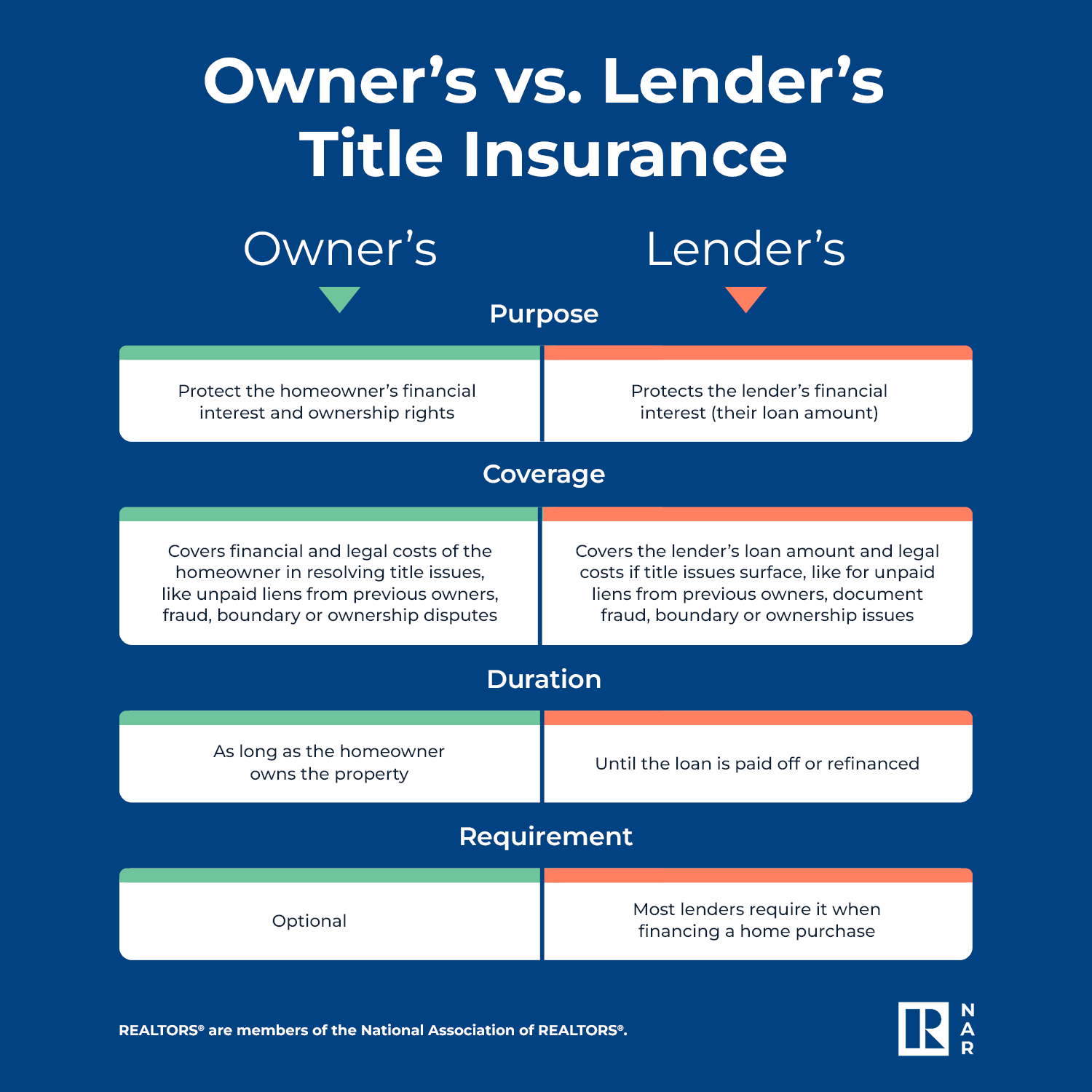

Types of Title Insurance

There are two main types of title insurance: Owner’s title insurance and lender’s title insurance. They offer two distinct benefits that home buyers should carefully consider before purchasing.

Lender's Title Insurance

Lender’s title insurance protects the lender—the bank or financial institution that is funding the buyer’s mortgage—in case any title disputes or defects are discovered after a transaction closes. It’s a way for lenders to protect their investment. Lenders typically require buyers to purchase this type of title insurance when approving a mortgage.

Lender’s title insurance only covers the lender’s financial interest in the property (aka the loan balance); it does not cover the homeowner’s full investment. Lender’s title insurance gives the lender the ability to recover the balance of the loan or extra costs when resolving title disputes.

Benefits of lender’s title insurance:

- Protects the lender’s investment from any potential title disputes for the duration of the loan;

- Safeguards the lender’s investment up to the loan amount;

- Allows the lender to proceed with foreclosure more easily if needed. If the borrower defaults on the loan, the lender may proceed without title issues getting in the way.

Owner's Title Insurance

Owner’s title insurance protects the buyer of the home from possible title issues or disputes that could arise after the home purchase. It protects the owner’s financial investment for the entire length of ownership. Owner’s title insurance, however, will not cover issues that buyers were aware of prior to the sale.

Owner’s title insurance is optional in a real estate transaction. But buyers may opt to purchase it for greater protection from financial losses if title issues arise. Owner’s title insurance also provides coverage to the homeowner for as long as they own the home, unlike lender’s title insurance–which will last only for the duration of the loan.

Benefits of owner’s title insurance:

- Provides assurance that homeowners are protected from financial losses if title issues surface, including potential legal costs;

- Protect owners if issues arise from previous owners, such as unpaid liens or hidden ownership claims;

- Offers coverage from title issues for the duration of ownership.