")

Housing affordability isn’t just a Gen Z or Millennial conundrum—it’s hitting those entering their golden years, too.

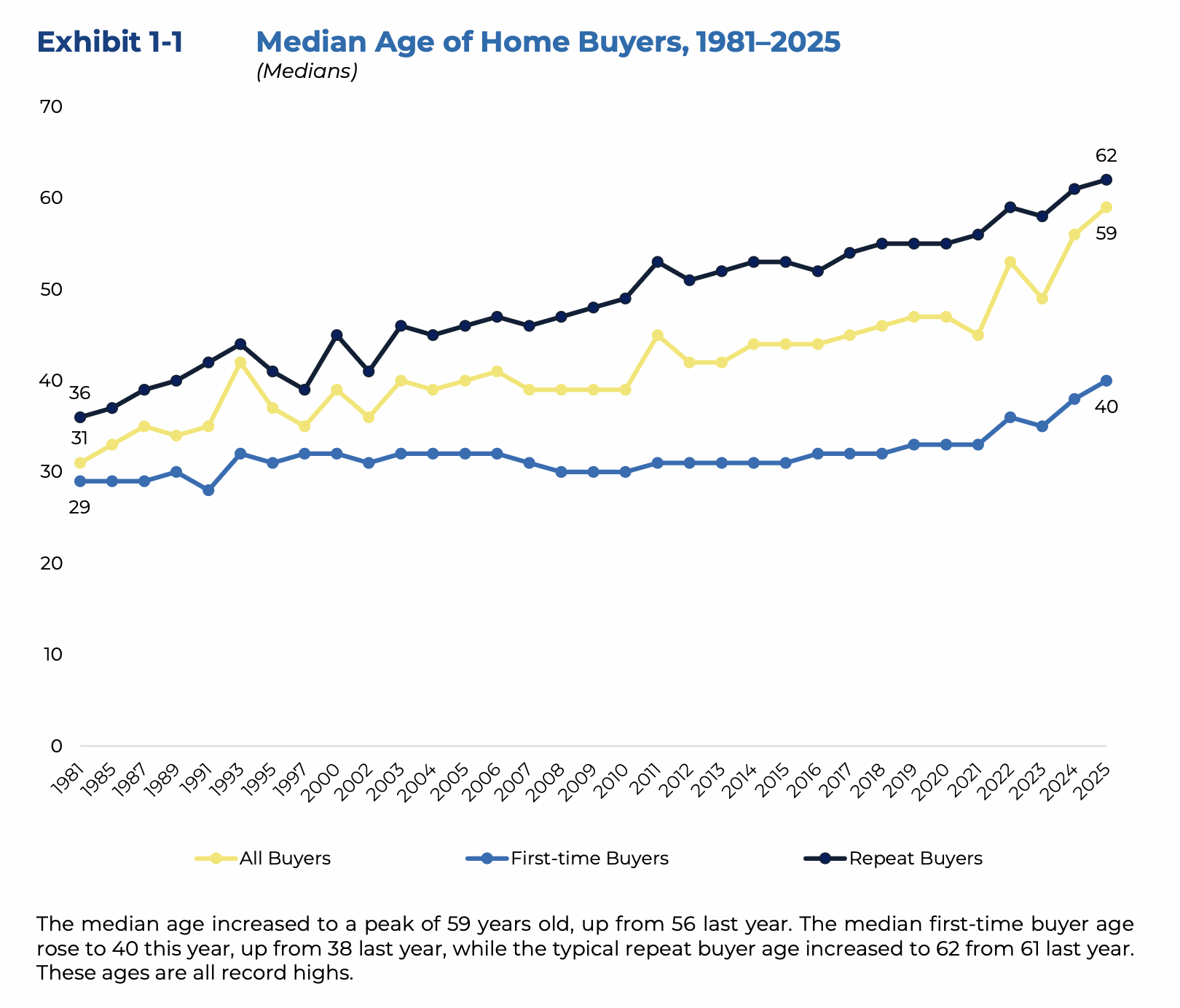

“The median age of a repeat buyer in this country, now, is 62,” Jessica Lautz, deputy chief economist and vice president of research at the National Association of REALTORS® said while speaking at the National Institute on Retirement Security’s Annual Retirement Policy Conference in Washington, D.C.

That’s the highest median age for repeat home buyers since NAR began recording in 1981. What’s more, many of these nearly-retirement eligible buyers are taking on debt to finance their purchase.

Related:

- Similar Homeownership Rate, Much Older Homeowners

- Americans Have Just $1K Saved for Retirement: Home Equity May Be Their Lifeline

“What we also see in the data is that half of [repeat] home buyers who are in their 70s are taking out a mortgage,” Lautz said. “When we look at those who are in their 60s—so, younger baby boomers—what we see is that [about] 40% of those are paying cash, which means the majority, 60%, are taking out a mortgage.”

The conference brought together policy experts to discuss how to bolster retirement security in America.

Lautz spoke on a panel moderated by Marketplace correspondent Nancy Marshall-Genzer, also featuring labor economist Kathryn Edwards and Washington Post personal finance columnist Michelle Singletary.

Edwards, who has amassed 300,000 followers across social media platforms like TikTok, focused on childcare costs and a flawed unemployment system as two barriers preventing people from investing in retirement savings.

“Getting out of the low-wage emergency job is impossible,” she said. “The low-wage labor market in the U.S. is about a fourth of our total employment, and it is an absolute trap. Once you fall into it, you rarely get out of it.” Edwards suggested public policy reforms are needed to prevent workers from falling into economic instability if they lose a job.

Singletary, who also runs financial literacy programming at her church and for those leaving the prison system, emphasized rising healthcare, student loans and raising financially savvy children. Singletary encouraged her children to move home after college—and it paid off.

“One of the agreements was [dad and I] aren’t going to charge you any rent, but almost all of your paycheck has to be saved,” she said. “And they saved 80% of their paycheck during that time. And they bought their first home. My youngest was 24 and my oldest was 28. They bought a home together.”

As the number one driver of wealth for most Americans, homeownership and home equity were hot topics. Last year, the share of first-time home buyers plummeted to NAR’s lowest recorded level, and first-time buyers on average are the oldest they’ve ever been at 40 years old.

Some are taking extreme steps to get there, Lautz explained, with more than one-fourth of first-time buyers cashing out or taking out loans against their 401ks and IRAs to buy a home.

She laid out some solutions to housing constraints like building more houses that meet the missing middle demand and highlighted low-down payment programs like Federal Housing Administration and U.S. Department of Agriculture loans, combatting the idea that you need 20% a down payment to buy a house.

“It’s a great goal, but I think it’s really far out of reach [for] a typical home in America,” she said.