")

An FHA loan is a mortgage offered by private lenders and backed by the Federal Housing Administration (part of the U.S. Department of Housing and Urban Development). These loans make homeownership accessible to more Americans, including buyers with poorer credit and those who haven't had the opportunity to save up a large down payment.

Knowing how FHA loans work is important for real estate professionals to ensure a smooth and streamlined homebuying experience. So, let’s review vital FHA eligibility criteria, minimum credit score requirements, income requirements, and property standards.

What Is an FHA Loan?

Insured by the Federal Housing Administration (FHA), FHA loans are designed to help individuals with lower credit scores, limited savings, or financial challenges become homeowners. The FHA doesn’t lend money directly but provides insurance to lenders, reducing their risk and enabling them to offer more flexible terms to borrowers who might not qualify for conventional mortgages.

FHA loans aim to make homeownership more attainable, particularly for first-time buyers or those with limited financial means. By offering this loan, the FHA plays a crucial role in expanding access to the housing market and promoting economic stability for buyers ineligible for conventional mortgages. In 2023, the FHA increased the price threshold for large multifamily loans from $75 million to $120 million, indicating their commitment to making housing and homeownership accessible to buyers.

Advantages of FHA Loans

FHA loans offer borrowers benefits that aren't always possible with conventional mortgages, such as:

- Lower down payment: FHA loans allow borrowers to make a down payment as low as 3.5%, making homeownership more affordable, especially for first-time buyers or those with limited savings.

- Flexible credit requirements: FHA loans are more lenient regarding credit scores. Borrowers with FICO® credit scores as low as 580 can qualify with a 3.5% down payment, and those with scores between 500 and 579 may still qualify with a 10% down payment.

- Government backing: Since FHA loans are insured by the Federal Housing Administration, lenders are protected against defaults. This government backing encourages lenders to offer better terms to borrowers who might not meet the stricter criteria of conventional loans.

FHA Loan Requirements

FHA loans aren't suitable for everyone, and the requirements may be more stringent than conventional mortgages for some buyers. They're also not ideal for buyers with good to excellent credit, as these buyers may be able to secure better rates and terms with a conventional mortgage. Here are the main requirements for FHA loans.

Basic Eligibility Criteria

Minimum eligibility requirements for FHA loan borrowers are as follows:

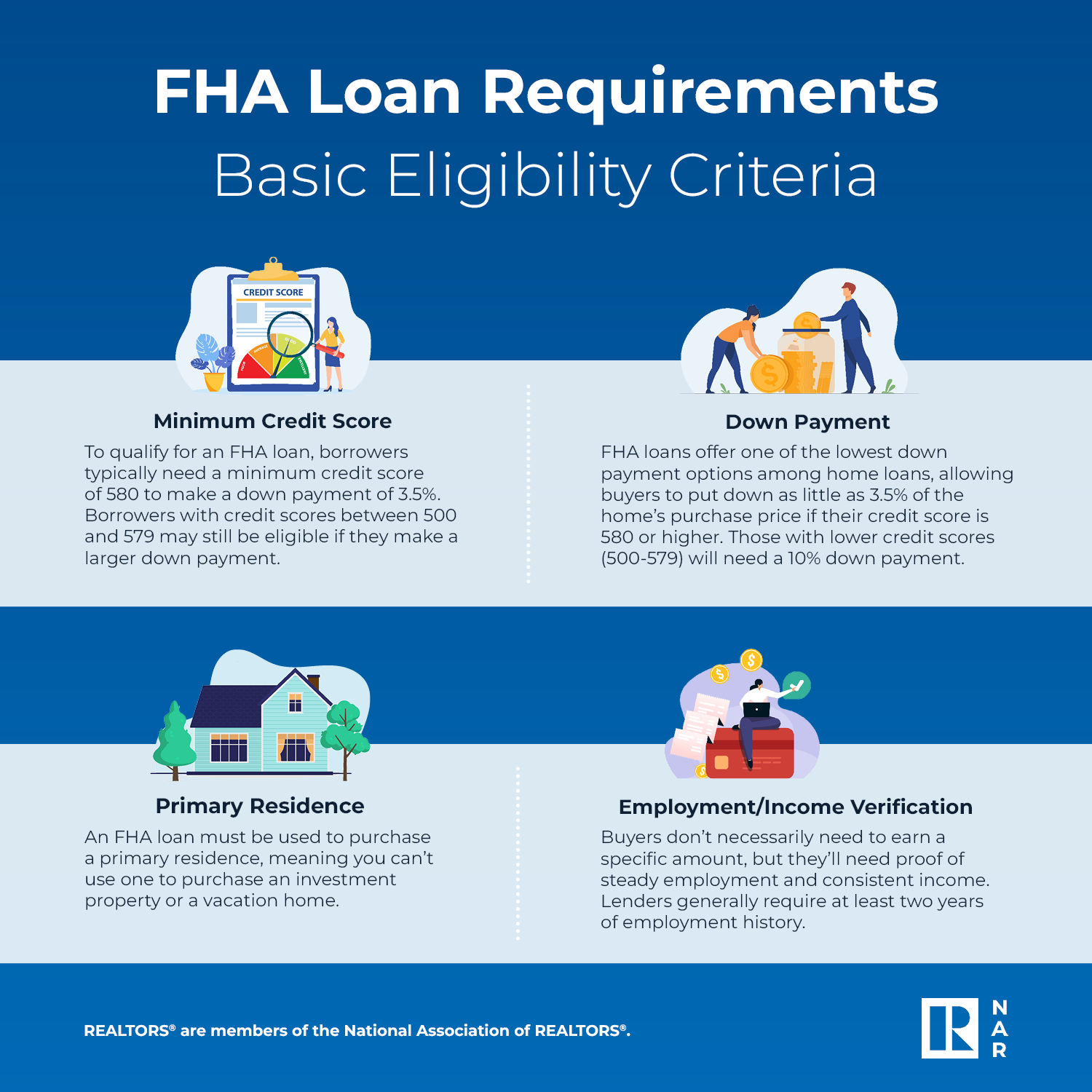

- Minimum credit score: To qualify for an FHA loan, borrowers typically need a minimum credit score of 580 to make a down payment of 3.5%. Borrowers with credit scores between 500 and 579 may still be eligible if they make a larger down payment.

- Down payment: FHA loans offer one of the lowest down payment options among home loans, allowing buyers to put down as little as 3.5% of the home’s purchase price if their credit score is 580 or higher. Those with lower credit scores (500-579) will need a 10% down payment.

- Employment and/or income verification: Buyers don't necessarily need to earn a specific amount, but they'll need proof of steady employment and consistent income. Lenders generally require at least two years of employment history.

- Primary residence: An FHA loan must be used to purchase a primary residence, meaning you can’t use one to purchase an investment property or a vacation home.

Downloadpdf (59 KB) | png (251 KB)

{kind=link}

Property Types

Buyers can purchase different types of properties with FHA loans. These are the accepted options:

- FHA 203(b) is the standard FHA loan used to purchase primary residences.

- FHA one-time close construction loans enable borrowers to build their dream houses instead of purchasing existing homes. Borrowers may be limited to building single-unit residences and need higher credit scores.

- FHA 203(k) rehab loans are ideal for buyers seeking fixer-uppers. Also available as a refinance loan, this mortgage includes the funds buyers need to renovate their home.

- FHA condo loans allow borrowers to purchase a condo unit in an approved condominium project. These loans may have specific requirements for the property.

- FHA mortgages for mixed-use property are for homes with at least 51% of space dedicated to the residence.

The FHA's minimum property standards require homes to be safe, secure, and structurally sound. An FHA-approved appraiser evaluates the home's adherence to these standards and value.

Debt-to-Income Ratio

Lenders pay close attention to the borrower’s debt-to-income (DTI) ratio, which is their total monthly debt payments divided by their gross monthly income. DTI is expressed as a percentage. A low DTI is beneficial for any mortgage applicant; but, for an FHA loan, it should be no higher than 43%. DTI is critical because it helps lenders assess a borrower’s ability to manage monthly payments and repay the loan. A lower DTI suggests that the borrower has more disposable income and is less likely to default on the mortgage. Some lenders may make exceptions for borrowers with higher credit scores or larger down payments.

Helping Clients Apply for an FHA Loan

These are the steps clients will take when applying for an FHA loan. The exact steps/process may differ by lender, so it’s a good idea for buyers to discuss the application process with different lenders as part of their research.

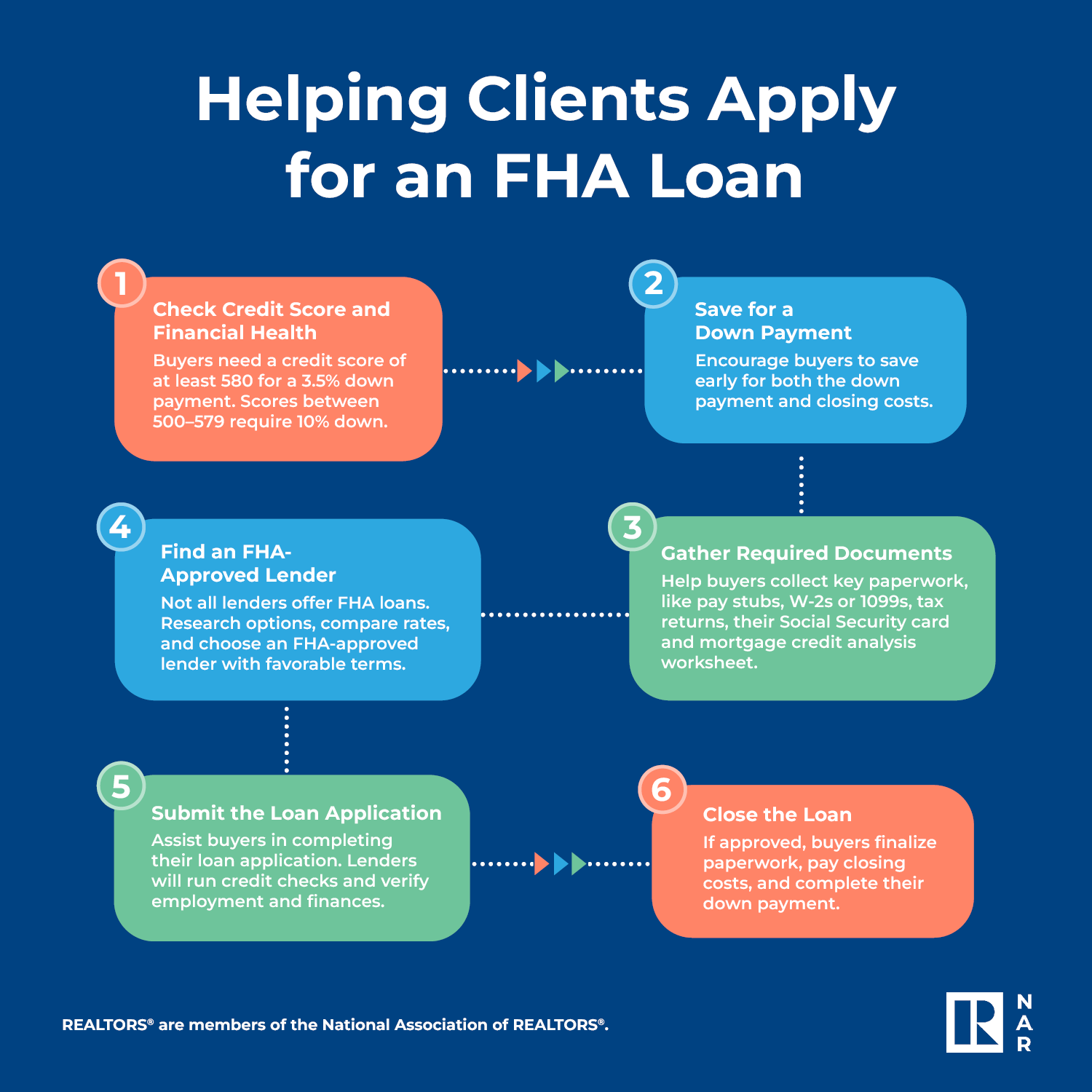

- Check credit score and financial health: Buyers need a minimum score of 580 for a 3.5% down payment. If their score is between 500 and 579, they can qualify with a 10% down payment. If buyers have a low credit score or their debt is too high to meet the 43% DTI requirement, recommend that they consult with a financial advisor to improve their credit score and finances.

- Save for a down payment: Buyers must start saving for their down payment before beginning their mortgage application. Recommend saving early to ensure they have enough for both the down payment and potential closing costs.

- Gather required documentation: Work with buyers to help them gather the necessary paperwork. This includes their mortgage credit analysis worksheet, pay stubs, W-2 or 1099 forms, tax returns, and social security card.

- Find an FHA-approved lender: Not all lenders offer FHA loans, so it’s important to choose one that is FHA-approved. Research different lenders, compare their terms, and choose one that offers favorable rates and terms.

- Submit the loan application: With the help of their lender, buyers must fill out the loan application, providing all necessary information and documentation. The lender will run a credit check, verify employment, and assess the applicant’s financial standing before approving or rejecting the application. They may request additional information or paperwork as they evaluate the application.

- Close the loan: If approved, borrowers move on to the closing phase. At this stage, they’ll finalize the paperwork, pay closing costs, and complete the down payment.

Downloadpdf (59 KB) | png (181 KB)

FHA Loan Requirement FAQs

How can you assist clients with low credit scores or high debt in qualifying for an FHA loan?

When a client is struggling with low credit or high debt, here are a few steps real estate professionals can take:

- Recommend working with a financial advisor to pay down debt and work on credit improvement strategies.

- Encourage buyers to consider financing early, including alternative financing options.

- Use effective negotiation methods and creative financing to help buyers and sellers meet in the middle.

Where is the latest FHA loan limit info, and how can you use it to benefit your clients?

Agents can easily find the latest information on FHA loan limits. HUD further offers a tool to help agents identify FHA mortgage limits in specific areas by state, county, or metropolitan statistical area (MSA). Understanding loan limits can help real estate professionals provide clients personalized property recommendations based on their needs and FHA loan eligibility.

How can you guide your clients through finding an FHA-approved condominium, and what resources can support this search?

FHA loans can be used to purchase condos, and HUD's condo search tool is an easy way to find FHA-approved condos in your client's desired area. However, it's important to note that even if the building your client is considering isn't FHA-approved, their lender can request FHA approval for the specific condo the buyer wants.