")

Labor market conditions continued to lose momentum, as revised payroll figures and a gradual uptick in unemployment indicated further cooling. With inflation readings on pause and hiring activity moderating, the Federal Reserve will likely proceed to another cut in December to support economic conditions. In response, longer-term interest rates have edged lower, providing early financial relief. At the same time, the broader economy has remained on solid footing, supported by steady consumer spending and continued strength across the private sector.

Overall, commercial real estate conditions remained mixed in November. The office market showed tentative improvement, with demand pressures easing from last year, but conditions were still constrained by tenant caution and widespread use of incentives, while recovery remained uneven across property classes. Multifamily conditions were largely steady as the sector continued to work through prior oversupply, with softer seasonal leasing and cooling rent momentum, though lower-tier properties showed greater resilience. Retail softened modestly as demand weakened and new supply added pressure, yet it remained comparatively resilient, thanks to stronger pricing power and steadier performance across general retail formats. Industrial continued to cool as elevated supply weighed on demand, pushing availability higher and slowing rents, signaling a broader shift from rapid expansion toward normalization.

Below is a summary of the performance of each major commercial real estate sector in November of 2025.

Office Properties

The office market showed tentative improvement in November, with annual absorption losses narrowing sharply from last year, though demand remained slightly negative. Vacancy held near 14.1% while rent growth slowed to 0.7%, reflecting continued reliance on concessions. Class A continued to anchor demand despite elevated vacancy, Class B saw gradual improvement with rents still outperforming the national average, and Class C remained under pressure but retained the lowest vacancy in the sector.

Multifamily Properties

The multifamily market remained largely steady in November, with absorption softening modestly as new deliveries continued to slow and the sector worked through prior overbuilding. Vacancy edged up to 8.3% while rent growth eased further to 0.2%, reflecting a weaker winter leasing season. Across property classes, pricing momentum cooled in Class A and B, while Class C continued to face tenant losses but maintained the lowest vacancy and the strongest relative rent performance.

Retail Properties

The retail sector softened in November, with annual absorption turning negative and rent growth easing to 1.9%, though it still leads all major property types in pricing gains. Vacancy held at 4.3%, but rising deliveries and limited removals point to mild upward pressure ahead. Performance diverged by segment, with general retail remaining the most resilient, while neighborhood and power centers saw weaker demand but continued to post the fastest rent growth.

Industrial Properties

The industrial sector continued to cool in November, as new supply remained well ahead of tenant demand, with net absorption down 30% year over year. This imbalance pushed vacancy higher, reinforcing the loss of momentum that has taken hold since the sector's peak. As availability increased, rent growth slowed to 1.4%, reflecting softer pricing power across most markets. Logistics properties still anchor demand, but overall conditions point to a normalization phase as the market works through elevated supply levels.

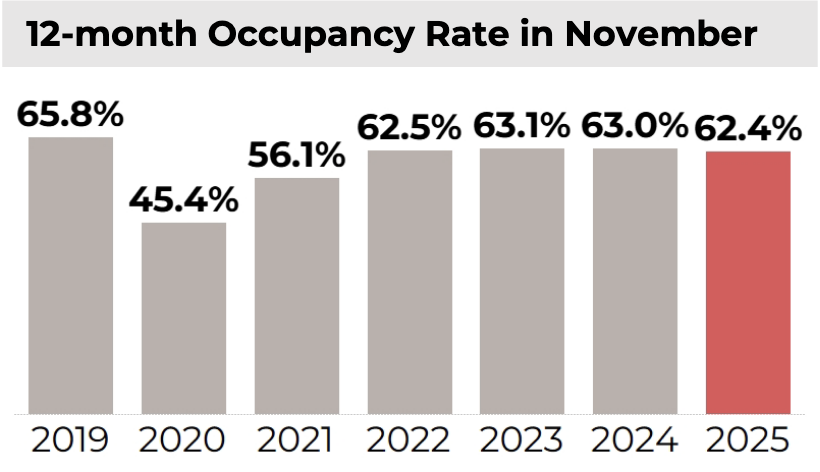

Hotel Properties

The hospitality sector held steady in November 2025, with occupancy at 62.4%, still about 3% below pre-pandemic norms as remote work trends and softer corporate travel continue to limit demand in major business markets. Despite this, hotel revenues have improved, with ADR and RevPAR now well above 2019 levels, supporting solid profitability. At the same time, transaction activity has slowed as higher financing costs and economic uncertainty make investors more cautious.