")

In the third quarter of 2024, the U.S. housing market was still struggling with housing affordability, as median home prices nationwide remained elevated compared to last year. In September, the 3% increase in median existing-home sales prices marked the 15th consecutive month of year-over-year price gains.

The primary factor driving housing prices is low supply. In areas where housing availability is constrained by factors such as a limited workforce, insufficient building permits or zoning restrictions, the demand exceeds the supply of homes. Although construction jobs are on the rise—growing about three times faster than overall employment since before the pandemic—many large metropolitan areas with strong job markets and growing populations continue to face housing shortages as demand outpaces housing supply. As a result, these areas remain unaffordable for many potential home buyers.

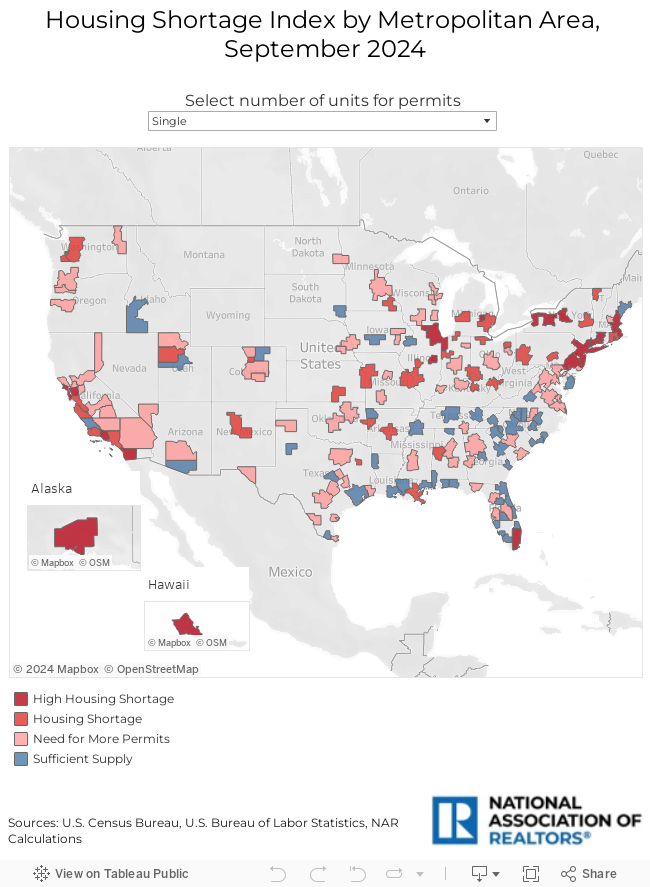

NAR identifies areas with the highest deficit of homes using the quarterly Housing Shortage Tracker index. The index computes how many new permits are issued for every new job in 172 of the major metropolitan areas in the country. A high index indicates that more jobs are being created than homes in a specific area. In a balanced market, one single-family permit is issued for every two new jobs. However, this was not the case for nearly 80% of the selected areas in the last quarter.

At the end of September 2024, the New York-Newark-Jersey City, NY-NJ-PA metro area experienced the most significant shortage of single-family housing units, with one single-family permit issued for every 23 new jobs. However, this represents a notable decline from September 2023, when the index stood at 32, meaning there was one single-family permit for every 32 new jobs. Similarly, the index for Urban Honolulu, HI, declined from 35 in 2023 to 18 in 2024. Among the top 10 areas with the highest housing shortages, three were in Connecticut: New Haven (18), Bridgeport-Stamford-Norwalk (14), and Hartford (14).

Conversely, the lowest shortages were observed in Ocala, FL, Myrtle Beach-Conway-North Myrtle Beach, SC-NC, and Memphis, TN-MS-AR, where the ratio was equal to 1. Several areas approached the balanced ratio of one single-family permit per two new jobs, including Spartanburg, SC, Crestview-Fort Walton Beach-Destin, FL, and Shreveport-Bossier City, LA.

By the end of the third quarter, only 35 major metropolitan areas had a housing shortage index at or below the historical average of 2. Nevertheless, 87% of the observed areas saw a decrease in their index from September 2023 to September 2024, indicating a trend toward an improved inventory of single-family homes.

Head to NAR's Housing Shortage Tracker page or use the visualization below to see how many permits are issued for every new job in your area: