")

Please note: The data visualization embeds on this page are best viewed on a laptop or desktop computer.

Purchasing a home is one of the most important financial decisions individuals and families make in their lifetimes. The process is not easy; from saving for the down payment to securing a loan, home purchasing can pose challenges along the way. According to NAR's recent report on the Profile of Home Buyers and Sellers (HBS), 11% of all buyers cited that saving for a down payment was the most difficult step in the home-buying process. Despite that, the median down payment in the U.S. has increased over the last year, and many households have achieved the American dream of owning a home.

In this analysis, let's dive into the details of down payments in the country's major metropolitan areas. Using 2024 data from the Home Mortgage Disclosure Act (HMDA) , we are able to identify the areas with the highest and lowest down payment shares, which can give us insight into households' financial abilities and help us identify markets with potential.

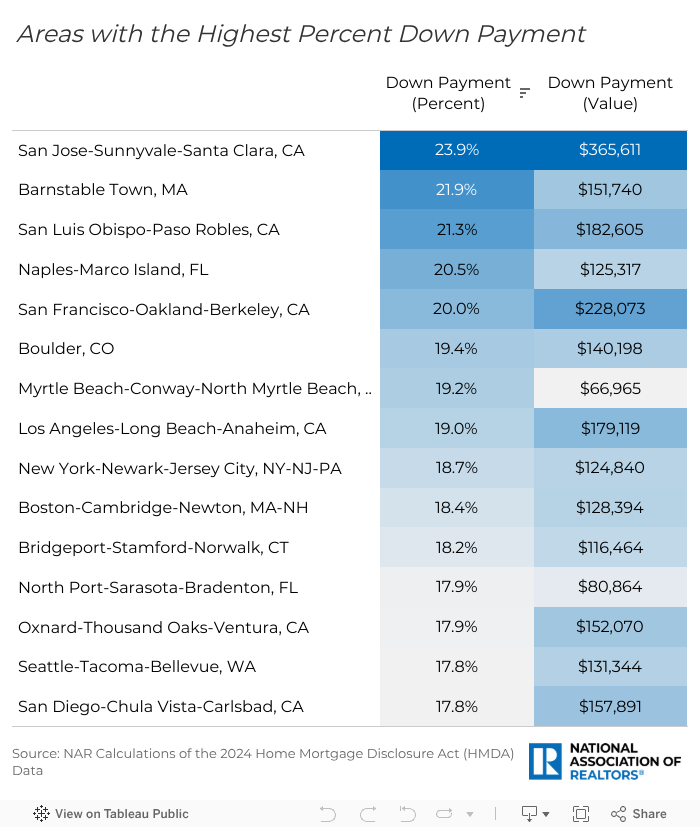

Areas with the Highest Percent Down Payment

We analyzed 216 of the country's largest metropolitan areas to determine where home buyers contribute the highest percentages of their down payments. Among those:

- The area with the highest percent down payment in 2024 was San Jose-Sunnyvale-Santa Clara in California, with nearly a 24% (or $365,611) down payment.

- San Jose was followed by high percent down payments in Barnstable Town, MA (21.9%), San Luis Obispo-Paso Robles, CA (21.3%), and Naples-Macro Island, FL (20.5%).

- Overall, 6 of the top 15 areas were in California, most notably including the San Francisco-Oakland-Berkeley (20.0%) and the Los Angeles-Long Beach-Anaheim (19.0%) areas.

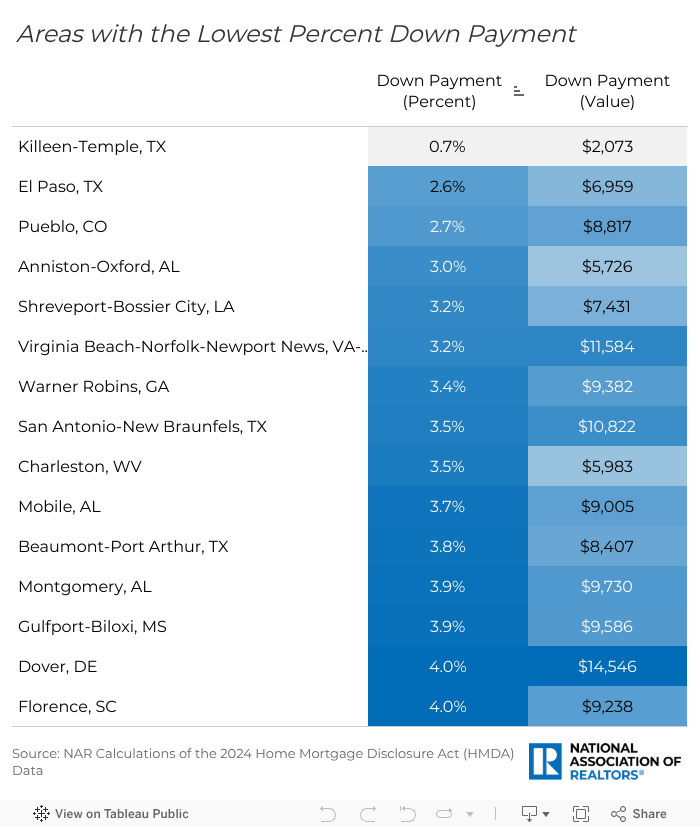

Areas with the Lowest Percent Down Payment

- The area with the lowest percent down payment was Killeen-Temple in Texas, with only 0.7% down payment (equivalent to $2,073).

- It was followed by El Paso, TX (2.6%), Pueblo, CO (2.7%), and Anniston-Oxford, AL (3.0%).

- Notably, 4 of the top 15 areas were in Texas, and another 4 were in Alabama.

- Many of the metro areas on this list, such as Virginia Beach-Norfolk-Newport News, VA-NC (3.2%), are areas with prominent military and oil industries, as well as university towns. Many households in those areas use FHA or VA-guaranteed loans, which, under certain criteria, don't require a down payment at all or have flexible credit requirements.

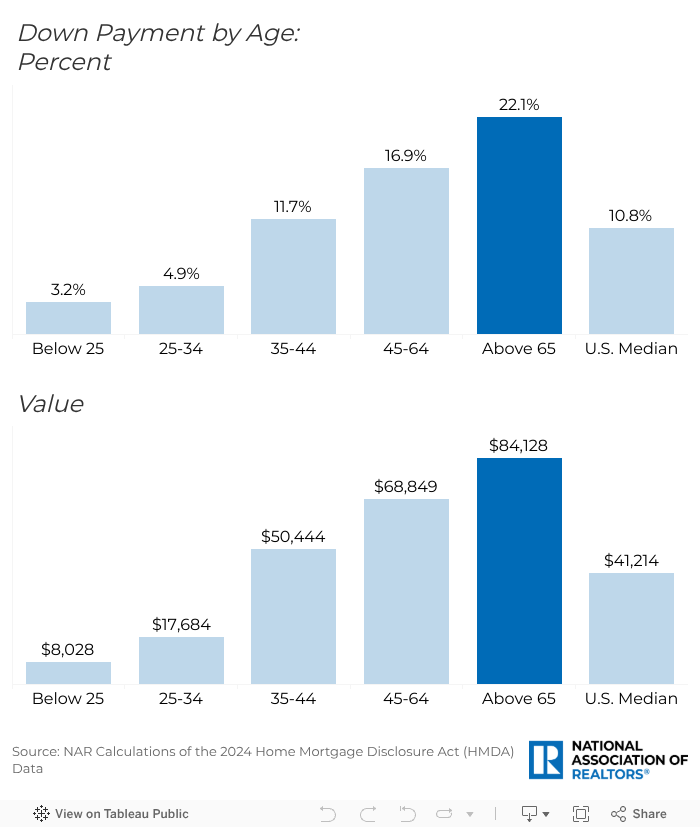

Age Distribution

Saving for a down payment can delay homeownership for many first-time home buyers. In fact, the data point out that older home buyers were able to put down a larger share of the property's value as an initial investment:

- In 2024, the highest down payment share was put down by home buyers 65 years old or older. This age group put down a median of 22.1% of the property's value when purchasing a home, or equivalently, $84,128.

- Right below them were home buyers 45-64 years old who put down almost 17% or $68,849 as a down payment.

- In contrast, buyers aged 25-34 put down approximately 5% (or $17,684), and buyers aged 35-44 put down 11.7% (or $50,444).

- The smallest group, buyers below the age of 25, put down only 3.2%, equivalent to $8,028.

- In comparison, the typical American borrower in 2024 provided a 10.8% down payment (or $41,214) when purchasing a home.

- According to NAR's HBS, the median home buyer age increased to a peak of 56 years old in 2024. That year, the average age of all buyers, both first-time and repeat, reached an all-time high.

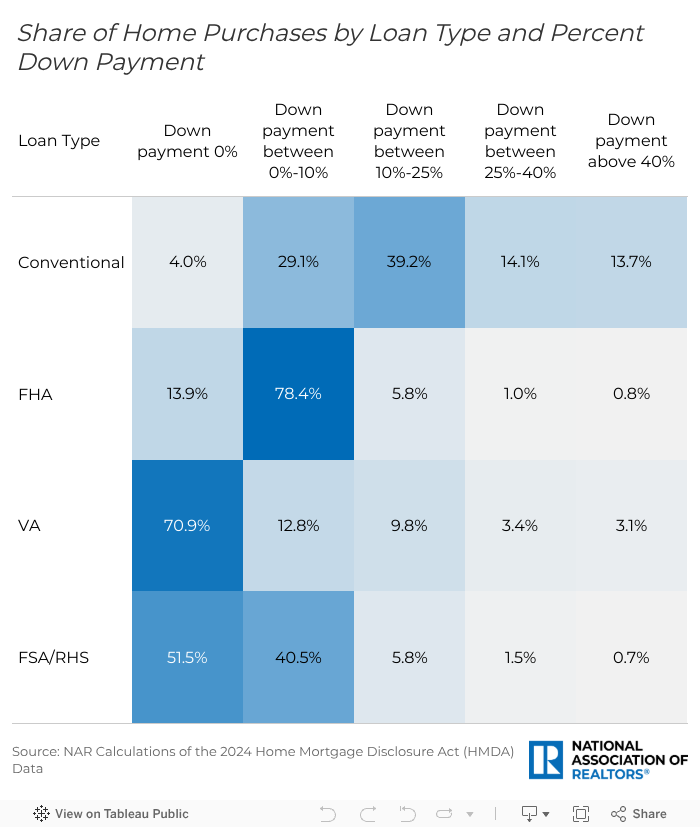

Share of Home Purchases by Loan Type and Down Payment

The size of the down payment that borrowers provide depends on a multitude of factors, such as income, years of saving, and property values in desired areas. In addition, it can be affected by the type of financing a home buyer is eligible for. Intuitively, loans with flexible down payment and credit score requirements are popular in areas where buyers put down a smaller share. In an analysis of home purchases by loan type and down payment, we see that:

- For home purchases that were financed using conventional loans, about 29% of borrowers made a down payment between 0%-10%, while approximately 39% of borrowers made a down payment of 10%-25%.

- 78.4% of FHA-backed loans had a down payment of 0%-10%.

- Notably, for VA-guaranteed loans, nearly 71% of home purchases didn't have a down payment at all (VA loans don't have a required down payment amount).

- 51.5% of FSA/RHS-backed home purchases had a down payment amount between 0%-10% of the property's value, and 40.5% of borrowers in this category put down between 0%-10%.

Ultimately, the size of the down payment varies significantly across metropolitan areas and among home buyers. Saving for the initial investment can be one of the most difficult steps in purchasing a home, especially for younger and first-time buyers. Nonetheless, certain life events, such as relocating for a new job or growing a family, often require individuals and families to purchase a home.

As REALTORS®, we want to guide our clients through this challenging process in the best way possible. Understanding trends in down payments and how they are influenced by geographic and demographic changes can help us assess local real estate market conditions and better prepare clients for their expectations regarding upfront costs. In addition, down payment trends often reflect broader economic fluctuations. Staying informed can help REALTORS® anticipate changes in their markets and adjust strategically.

To see down payment details in your market, select a metropolitan area on the map below:

Advertisement

Anat Nusinovich

Anat Nusinovich is an economist for the National Association of REALTORS®.