Including home buying and selling, commercial, international, NAR member information, and technology. Use the data to improve your business through knowledge of the latest trends and statistics.

Stay current on industry issues with daily news from NAR. Network with other professionals, attend a seminar, and keep up with industry trends through events hosted by NAR.

America's largest trade association, representing 1.5 million+ members, including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries.

Review your membership preferences and Code of Ethics training status.

Research & Statistics

Including home buying and selling, commercial, international, NAR member information, and technology. Use the data to improve your business through knowledge of the latest trends and statistics.

Academic opportunities for certificates, associates, bachelor’s, and master’s degrees.

News & Events

Stay current on industry issues with daily news from NAR. Network with other professionals, attend a seminar, and keep up with industry trends through events hosted by NAR.

America's largest trade association, representing 1.5 million+ members, including NAR's institutes, societies, and councils, involved in all aspects of the residential and commercial real estate industries.

Dozens of REALTORS® made a special trip to Washington this week to make a forceful case for protecting homeownership as lawmakers advance sweeping reforms to the tax code.

“I’m going to pay $7,230 more in taxes.” Cynthia Carley of Lake Arrowhead Properties in Blue Jay, Calif., federal political coordinator for Rep. Paul Cook of California

"Members of Congress are not able to fully absorb every issue they have to deal with, so the more they hear from us, the more they'll understand how the legislation they're voting on will affect homeowners and their communities," said Cynthia Carley of Lake Arrowhead Properties in Blue Jay, Calif.

Carley, a politically active REALTOR® who serves as the federal political coordinator for Rep. Paul Cook of California, was one of the REALTORS® participating in a special fly-in to meet with members of Congress. Her message to Cook: most middle-income homeowners, like she and her husband, face a tax hit if either of the reform bills under consideration in the House and the Senate pass without changes.

Notice: The information on this page may not be current. The archive is a collection of content previously published on one or more NAR web properties. Archive pages are not updated and may no longer be accurate. Users must independently verify the accuracy and currency of the information found here. The National Association of REALTORS® disclaims all liability for any loss or injury resulting from the use of the information or data found on this page.

Contact Your Representatives

Reform our tax code AND protect middle-class homeowners.

"I calculated my own taxes under the provisions in the House bill and I'm going to pay $7,320 more in taxes than I did in 2016," she said.

Christian Schlueter of RE/MAX at Barnegat Bay in Toms River, N.J., and the federal political coordinator for Rep. Tom MacArthur of New Jersey, said he wants Congress to go back to the drawing board on tax reform. "In our district, there are a lot of homeowners that this would affect," he said.

Both the House and the Senate versions of tax reform would hurt homeowners who earn between $50,000 and $200,000 a year, NAR analyses show.

WASHINGTON (November 2, 2017) – Tax reform discussions took a major step forward this afternoon as leaders on the House Ways and Means Committee released its legislative proposal for an overhaul of the American tax code. The National Association of Realtors® believes the bill represents a tax increase on middle-class homeowners.

"This legislation closely tracks with the House Republican Blueprint for tax reform, which threatens home values and takes money straight from the pockets of homeowners," said NAR President William E. Brown, a second-generation Realtor® from Alamo, California and founder of Investment Properties. "Realtors® believe in the promise of lower tax rates, but this bill is nowhere near as good a deal as the one middle-class homeowners get under current law. Tax hikes and falling home prices are a one-two punch that homeowners simply can't afford."

Brown said that America's homeownership rate still hovers around a 50-year low today. For many middle-class families, buying a home is the single largest investment they'll ever make, and in fact, the average net worth of a homeowner is 45 times that of a renter. By eliminating or nullifying the incentive for homeownership, however, Realtors® are concerned that homeownership's wealth-building potential could be pushed out of reach.

Earlier this year, NAR released a full analysis of the House Republican blueprint for reform, finding that it would cause a 10 percent drop in home values and raise taxes on middle-class homeowners by an average of $815.

Like the blueprint, the legislation released today doubles the standard deduction, while repealing all itemized deductions, except for mortgage interest and charitable contributions. NAR noted in its comments on the "Unified Framework" for reform that such a proposal would nullify the homeownership incentive for all but the top 5 percent of tax filers.

This bill, however, goes even further by capping the mortgage interest deduction at $500,000 for newly purchased homes. The legislation also eliminates state income tax deductions altogether, while installing a new cap on property taxes. At the same time, the proposal puts new restrictions on the capital gains exemption homeowners utilize today when they sell their home. The exemption is vital to allowing homeowners to use their equity to pay for retirement and other long-term needs.

"The nation's 1.3 million Realtors® cannot support a bill that takes homeownership off the table for millions of middle-class families," Brown said. "We know this legislation is just the beginning of a much longer discussion. Our members will continue to make their voices heard as we push towards tax reform that responsibly lowers rate while protecting the dream of homeownership."

The National Association of Realtors®, "The Voice for Real Estate," is America's largest trade association, representing more than 1.3 million members involved in all aspects of the residential and commercial real estate industries.

The House tax reform proposal (HR. 1) will have large negative impacts for a wide swath of America’s residential real estate. In particular, the cap on deductible mortgage interest, the elimination of the deduction for state and local interest and sales taxes, and the change to the capital gains exclusion will impact large segments of the market. Worse, the current historically low mortgage rates mask the negative effect that these changes will have on home ownership, which will only grow as interest rates and home prices rise in the future.

Capping the MID

Currently, the mortgage interest deduction is capped at a loan balance of $1,000,000. Under the House proposal, the cap would fall to $500,000. Unlike the conforming loan limit, this cap is uniform across the country and does not adjust for high cost areas.

However, the $500,000 cap is not indexed to inflation or home price growth like the conforming loan limits, so that more homebuyers will be pushed into this category over time. If homes rise at the historic average pace of price growth, that share will rise dramatically. A more detailed analysis by NAR Economist Nadia Evangelou can be found here.

State and Local Income and Sales Taxes

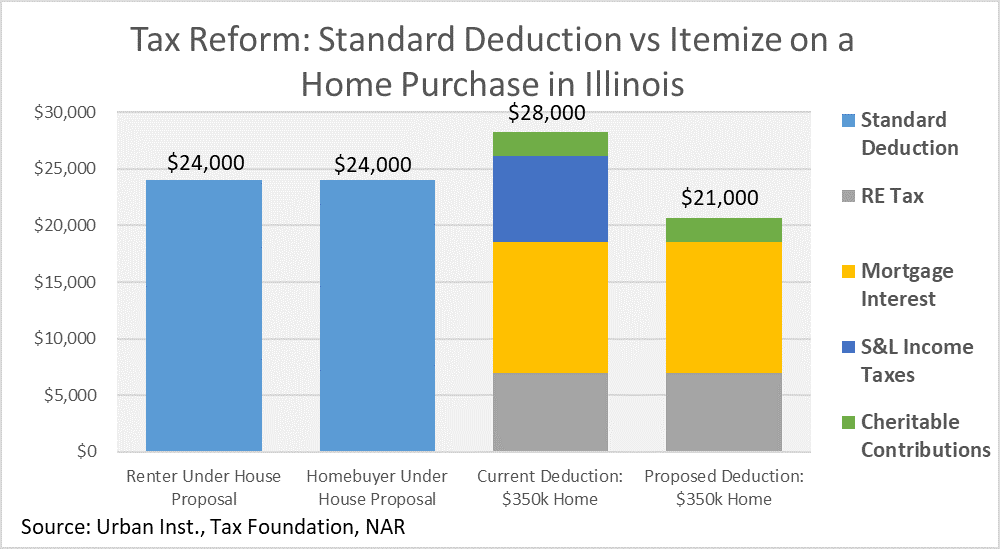

As drafted, the House proposal does allow for the deductibility of some mortgage interest and real estate taxes. However, real estate tax deductions are capped at $10,000 and that figure is not indexed to allow for growing home values or tax rates over time.

Worse, the House proposal does not allow for the deduction of state and local sales or income taxes. Typically, a homebuyer will itemize if their total deductions for real estate taxes and mortgage interest, along with the state and local income or sales taxes and charitable deductions, are greater than the standard deduction. By eliminating the state and local income taxes, which vary from 2 percent to 9 percent of income by state, and sales taxes the sum of deductions will be far less likely to be higher than standard deduction for many. While the House proposal includes a near doubling of the standard deduction, these amounts will be well below the current-law deduction for many buyers and the new law would reduce itemized deductions for many owners in higher priced markets or areas with high income or real estate taxes.

As the above example depicts, a couple in Illinois buying a $350,000 home who puts 10 percent down would currently deduct more than $28,000 in MID and state/local taxes, but these itemized deductions would fall to just over $21,000 under the proposal. The buyer would take the standard deduction of $24,000, but would be hurt by the $4,000 short fall in deductions.

Capital Gains: A Bigger Hit Than Many Realize

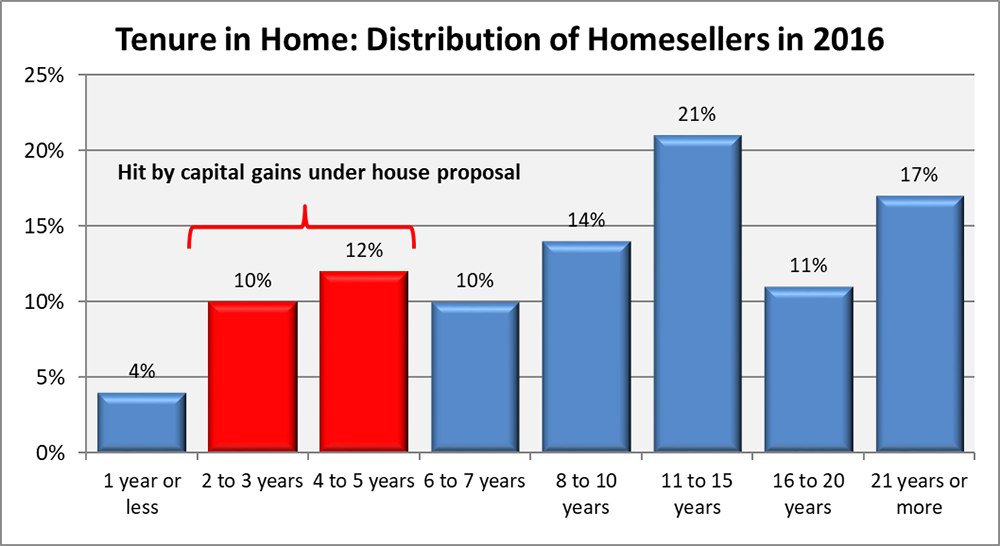

The House bill also provides for major changes to the current exclusion of capital gains that sellers make when selling their homes. In particular, it changes the tenure rule so that a home seller must have lived in the home for five of the last eight years to claim the exclusion from capital gains. That is a significant increase from the current rule of two of the prior five years.

In 2016, only 4 percent of sellers had held their homes for less than two years, while a significant 12 to 22 percent of home sellers (not investors or vacation home sellers) sold in 5 years or less. This change would be a 3 to 4-fold increase in the number of sellers hit by capital gains and would impact every market and every income bracket. This change would impact trade up buyers, job movers, divorcees, and those in the military, retarding labor mobility and exacerbating historically low supplies.

The Middle Class Tax Cut: Here Today (for some), but Gone Tomorrow

Most analysis of impacts based on current conditions can be misleading. Mortgage rates are historically low, but are forecast to rise in the coming years along with home prices. This combination will cause mortgage interest and taxes paid to rise. As a result, home buying or home owning families that might benefit from the proposal at today’s rates will be hurt in the future.

The chart above depicts the impact of the House reform on homebuyers at different income levels. Under the proposal, many families of four who buy a home would see a modest tax reduction today (blue). However, a simple sensitivity analysis shows that as mortgage rates rise, the benefits of reform decline. What’s more, the proposal temporarily allows each parent to take a $300 family credit. When this provision expires after 5 years and using the CBO’s forecast1, nearly every middle-class home buying family will lose the benefit of reform and will be hit with a tax increase (yellow).

Bottom Line

Simplification of the tax code has merit, as does the need to stimulate growth via productivity and regulatory reform. However, the House proposal will have broad consequences for middle class families, homeowners, and future homebuyers. This is especially important since real estate accounts for nearly a fifth of the economy, and changing tax preferences for real estate will have broad, long lasting consequences.

1 June 2017: this analysis incorporated the CBO’s forecast of 10-year Treasury rates, home prices, income, and CPI to adjust tax brackets, itemizations, standard deductions, and child credits

The House bill, which passed the tax-writing Ways and Means Committee recently and could go before the full House shortly, blurs the distinction between owning and renting by making it more advantageous for homeowners who itemize today to take the standard deduction instead. It does that by almost doubling the standard deduction while either eliminating or capping itemized deductions. The bill keeps the mortgage interest deduction but limits it to mortgages of $500,000, half of the limit today, and caps the property tax deduction at $10,000. The other state and local tax deduction is eliminated entirely, as are all other deductions except the one for charitable contributions. The bill also makes it harder to take the capital gains exclusion on the proceeds from the sale of a principal residence.

"The advantages they think they're providing aren't really advantages to middle-class homeowners." David Barber, GRI, ABR, of RE/MAX Unlimited, Inc., in Aurora, Colo., federal political coordinator for Rep. Mike Coffman of Colorado.

The Senate bill takes the same structure as the House bill but leaves MID at its current $1 million mortgage limit and eliminates the property tax deduction entirely, among other differences.

Although the higher standard deduction sounds like a win for many households, the increase is offset by the elimination of the personal and dependency exemptions. NAR calculates that many households will only see a small benefit from the higher deduction.

"If you're looking at it from a conceptual standpoint, sure, a tax cut is a great idea," said David Barber, GRI, ABR, of RE/MAX Unlimited, Inc., in Aurora, Colo., and the federal political coordinator for Rep. Mike Coffman of Colorado. "But how does the rubber meet the road on that? Some of the advantages they think they're providing aren't really advantages to middle-class homeowners."

"This is the biggest and scariest thing I've seen." Brian Urdiales of Madison & Co., Properties in Greenwood Village, Colo., federal political coordinator for Sen. Cory Gardner of Colorado.

"This is the biggest and scariest thing I've seen," said Brian Urdiales of Madison & Co., Properties in Greenwood Village, Colo., and the federal political coordinator for Sen. Cory Gardner of Colorado. "People don't realize that what happens here in Washington can affect their profession and affect their customers."

More on NAR's concerns with the House bill can be found here: