By: Carol Weinrich Helsel, contributing writer

Department stores’ financial woes have led to the nationwide shuttering of large anchor retail outlets such as Sears, Bon-Ton, and Macy’s. Coresight Research estimates that roughly 25% of American malls will close in the next three to five years, and Moody’s Analytics expects some 135 million square feet of mall space to become available during that period. Because of their convenient locations and high visibility, anchor retail structures have attracted adaptive reuse projects including gyms, entertainment venues, libraries, college satellite campuses, and even churches. Joining this list are self-storage facilities.

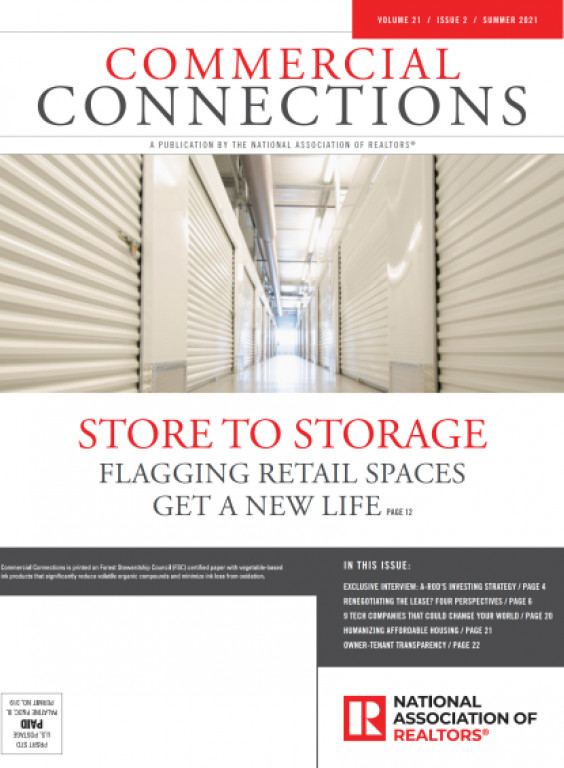

© CHRIS HACKETT/GETTY IMAGES

“Several factors make the timing right for the conversion of mall retail to self-storage,” says Blaze Cambruzzi, partner with TRUE Commercial Real Estate in Lancaster, Pa. “There’s a lot of aggregated capital seeking placement in underutilized value-add assets. Properties can be purchased below replacement costs, and most retail centers.

Include parking ratios that, when converted to storage ratios, yield excess land and additional opportunity. Add to this the growing consumer demand for storage and increasing supply of large vacant retail space, and you can see opportunity.”

More than one in 10 U.S. households (an estimated 13.5 million) rent a self-storage unit, according to the Self Storage Association. Demand stems from the high cost of housing, which is driving new homeowners to buy smaller homes, and from baby boomers who are downsizing but having trouble parting with possessions.

Also, the nature of storage has changed. People used to store things they might need someday. Now, people use self-storage as an extension of their home space, routinely accessing their units once a month, according to Cambruzzi. “Retail locations work well for storage because they are oriented toward recurring trips.” Aside from ease of access, repurposed retail space is attractive as self-storage because it provides a clean, secure, climate-controlled environment—a must-have for today’s consumers.

Cost of Retail Conversions Attracts Developers

The floor plan and ceiling height of mall anchor stores are well-suited to self-storage conversion, according to Barry Johnson, vice president of investments for Fairway America, a private equity and advisory firm specializing in commercial real estate asset–based investments. “They can accommodate a mezzanine and two levels of units, and most include a loading dock.” Johnson cited a project in Michigan that offers a “drive-thru” option, allowing users to unload their car in a warm and dry environment.

“Buying at $60 per square foot and retrofitting at $20 is cheaper than building from the ground up—especially given the rising cost of construction, which has doubled in some markets since 2018,” says Johnson. The lower cost of conversion has increased competition for use of the space.

“Brokers have become much savvier about potential uses. They no longer market vacant retail as ‘distressed’ but instead as ‘opportunity development.’ We’ve lost deals to buyers who put in offices, health care facilities, and a trampoline park,” says Johnson.

Overcoming Conversion Challenges

While a vacant Macy’s may be ideal for a self-storage conversion, it’s often a hard sell to local municipalities. Self-storage as an asset class is not covered in all zoning codes. If covered, retail locations are typically not zoned for self-storage, requiring a text amendment. “For some of the deals we’ve structured, we brought in existing owners with the buyer, and even former listing brokers, to advocate for a zoning change, because there has been zero interest in the property,” says Johnson. “Still, just one council member objection can kill a deal. Of the 30-plus deals we have underwritten over the past year, only one moved forward—all because of zoning issues.”

Municipality objections are largely twofold. First is concern about lost tax revenue. A self-storage facility typically employs just a few people and produces no sales tax revenue. City councils are reluctant to let go of possible future revenue associated with retail. Secondly, for many, self-storage evokes images of metal garage doors opening to the exterior—a far cry from today’s modern facilities. “Most self-storage conversions are as nice as or nicer than any other similar-sized construction today,” says Johnson.

Adjoining tenant leases also complicate mall store conversion. Some have exclusions regarding the type of business that can occupy an adjacent space—for example, restaurants—but few retailers had the foresight to name self-storage. Like city councils, neighboring tenants may object based on outdated perceptions. “Most will be happy if the repurposed space doesn’t bring in a competitor,” says Cambruzzi. “If you have a Walmart at one end and bring in a grocery store to occupy a former Sears at the other, you’ve introduced competition. Self-storage won’t be a competitor to existing retail.”

Brokers can overcome conversion objections by helping municipalities see storage as complementary to a growing community and responsive to residents’ needs. Cambruzzi says people will solve their storage problems one way or another. Lacking good self-storage options, communities risk unsightly storage on residential properties and increased safety hazards from overfilled basements, blocked hallway doors, and so on.

Investor Interest Remains Strong

Inside Self Storage, a self-storage industry group, reports continuing acquisitions and strong investor interest. Despite last year’s economic disruptions, self-storage sales totaled $7.7 billion in 2020, up a third from 2019 levels, according to Real Capital Analytics. Large self-storage REITs, such as Public Storage and CubeSmart, account for only about 20% of the market. The other 80% of facilities are owned and operated by individual investors, including mom-and-pop owners.

Johnson says a conversion strategy is best suited to a local buyer. For brokers willing to work with the owner to address zoning challenges, conversions can deliver high returns because the properties can typically be converted for a fraction of new ground-up construction costs. “Once there is a clear path for redevelopment, you’ll see that reflected in the price,” says Johnson.

Regardless, projects already zoned for self-storage are attractive to buyers. Such is the case with a Bon-Ton conversion Cambruzzi settled in April. “Once the zoning text amendment was in place, we received seven letters of intent within 60 days, adding to a buyer already at the table.”

For the investor-owner, the self-storage sector is strong. Yardi Matrix reports that 2021 is off to a good start with street-rate rental performance positive in 87% of the markets tracked. Top markets include San Francisco and the East Bay; the Inland Empire of California; Washington, D.C.; San Jose, Calif.; Phoenix; and Miami. Some of the growth is attributed to the pandemic—for example, college students returning home and needing to clear out dorms, workers carving out space for home offices, and restaurants storing unused tables and chairs to accommodate social distancing—but the American appetite for acquiring “stuff,” combined with smaller homes, suggests this sector will continue to perform well.

Further contributing to the strength of the self-storage sector is consumers’ tolerance for rent increases. “Owners can increase rents as much as 10% to 15%, often multiple times a year, and receive limited pushback from renters,” says Johnson. “Rates will be comparable elsewhere, so there’s no incentive to move, especially given the time and effort involved.” Cambruzzi agrees: “Self-storage provides a level of inflation protection other commercial real estate investments lack.”

Conversions Not Right for Every Market

Cambruzzi warns against being the broker with no experience in these conversions who sees an empty retail store and tags it “perfect” for self-storage. There are many considerations, including the local housing market. “If there’s not a lot of growth, it may not make sense,” says Cambruzzi, who had discussed multiple scenarios with the Bon-Ton property owner before hitting on the idea of self-storage.

It was only after extensive market research that self-storage was deemed right for the two-story space, located in an operational mall. The storage conversion joins a casino and a gym (formerly a Sears and JCPenney, respectively).

The exact location of the anchor store is also a factor, especially in a dying mall. Successful conversions rely on drive-by traffic for marketing. “Stores located on the backside of a mall, or too far off the street due to parking areas, will not be as successful,” says Johnson.

Brokers can counter inexperience by doing their homework. Cambruzzi suggests going to the investor relations sections at websites of publicly traded firms such as Amerco (U-Haul) to track the self-storage sector. “Download reports, listen in on earnings calls, and educate yourself.”

Given the growing supply of vacant retail, including department store anchors, adding self-storage to the list of possible adaptive reuses is good for local commercial markets.

And while nothing lasts forever, industry experts and investors view self-storage as a stable sector that will continue to provide high yields with low declines and default ratios compared to other asset classes.