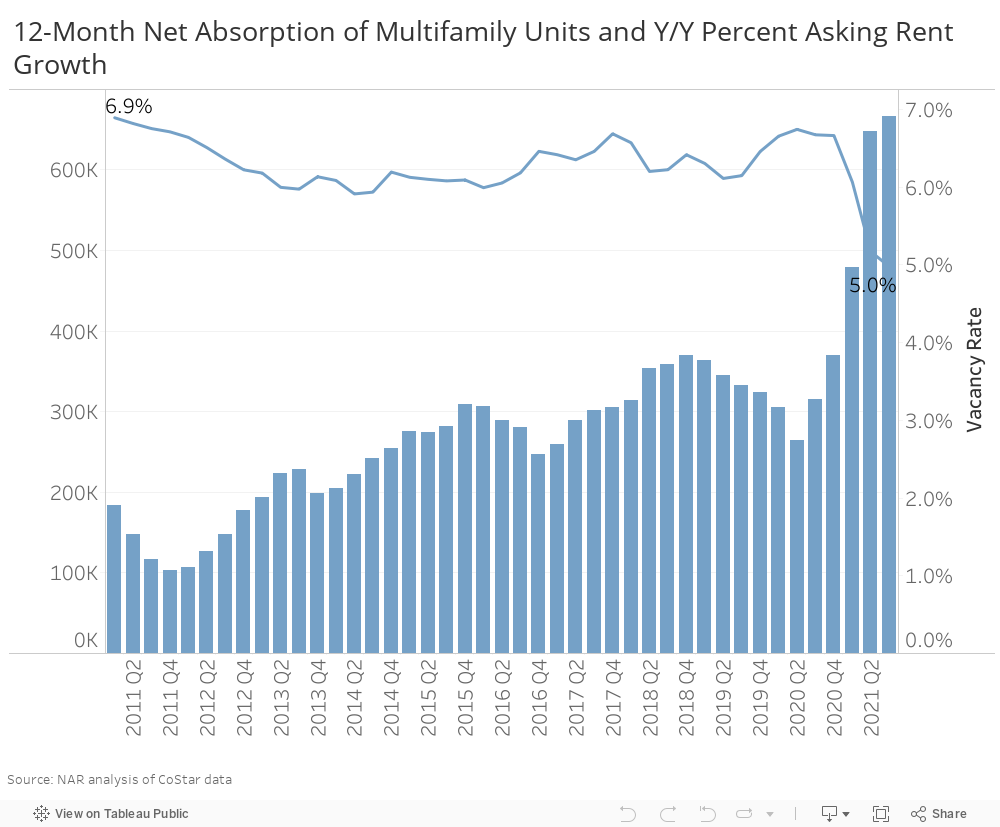

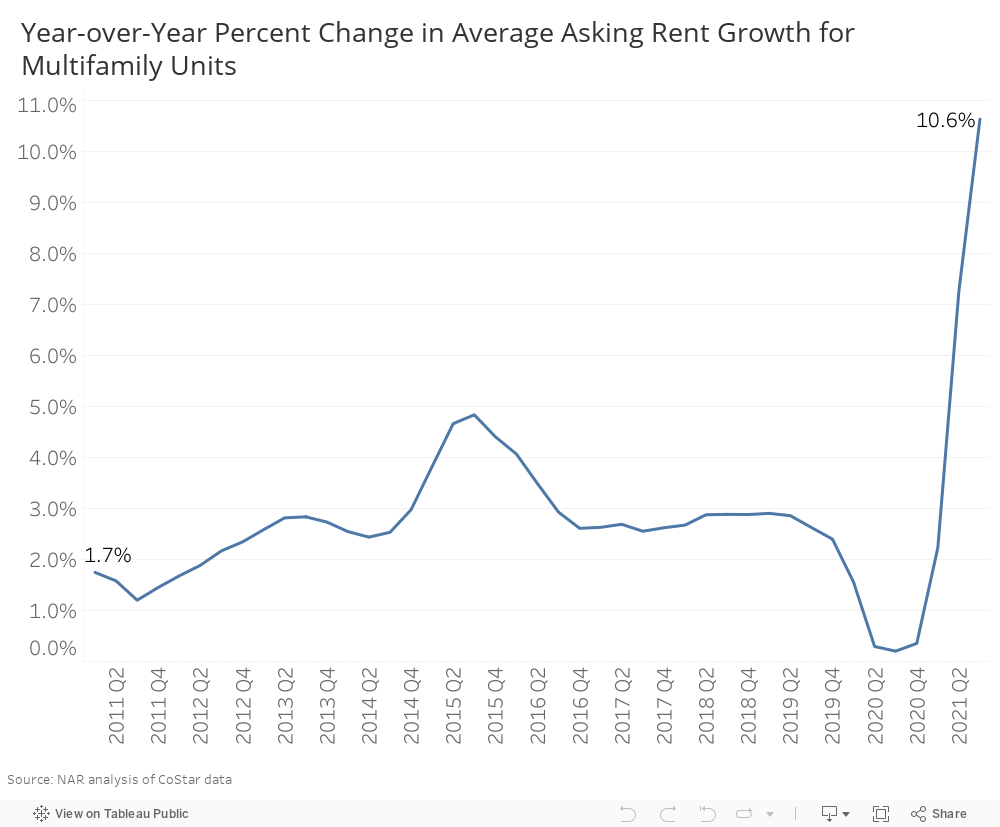

The demand for apartments continues to heat up, marked by record-high absorption and rent growth and low vacancy rate. During the past three months ending September 7, there was a net occupancy gain in 666,255 apartment units (net absorption), which is double the 12-month net absorption prior to the pandemic (2020 Q1) of 304,623 units. With demand for apartments soaring, the vacancy rate has dropped to 5% from 6.7% in 2020 Q1. With falling vacancy rates, average asking rents during the 3-month rolling period ending September 7 rose 10.6% year-over-year, up from just 1.6% prior to the pandemic (2020 Q1).

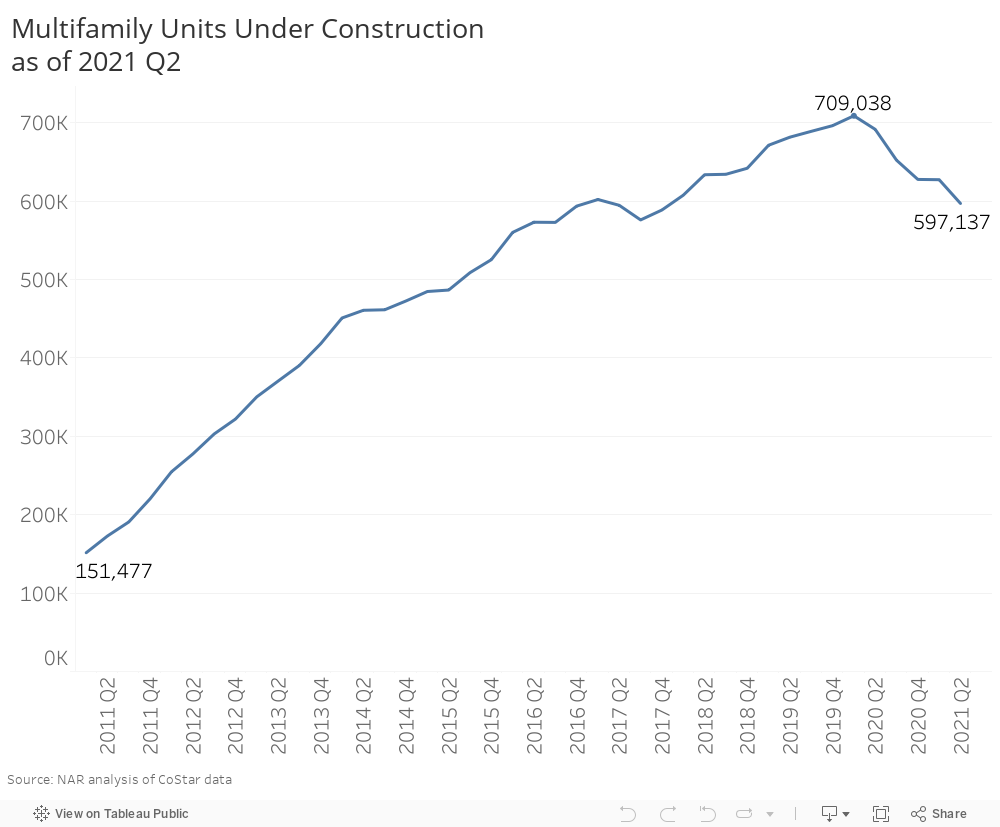

Rent growth has surged due to the massive increase in net absorption while construction activity has declined compared to pre-pandemic levels. As of 2021 Q2, CoStar reported 597,137 multifamily units under construction, or 111,901 fewer units compared to 709,038 units prior to the pandemic.

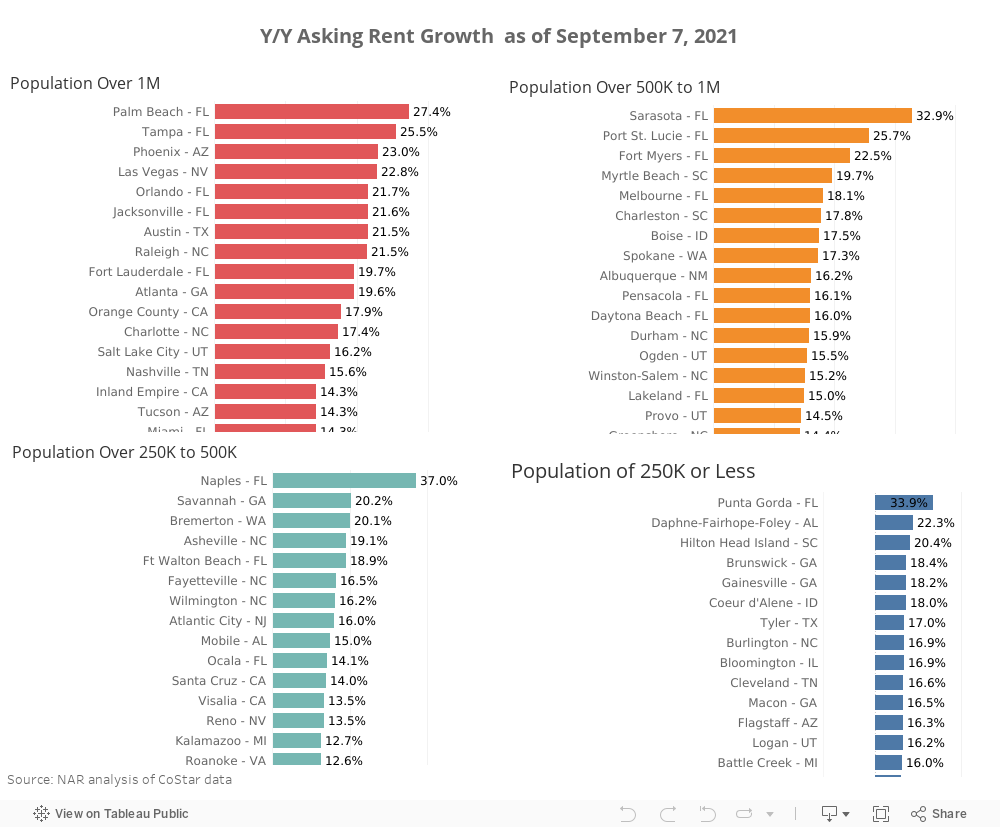

Stronger Demand for Apartments in Metros with Population of Over 1 Million

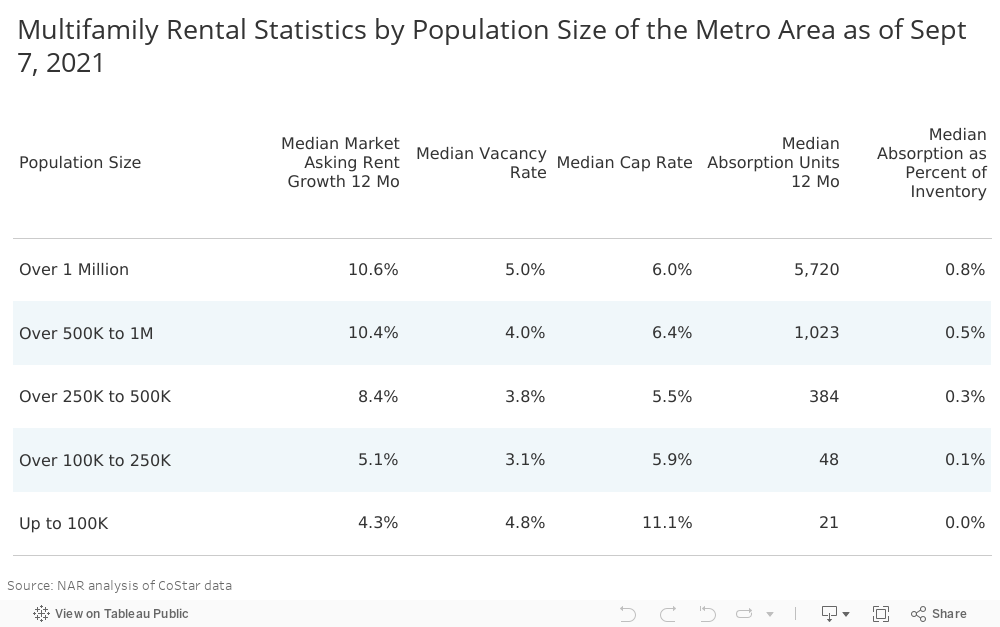

Metro areas with population of over 1 million are exhibiting stronger demand than metros with smaller populations based on analysis of the CoStar market data by population sizes of the metro areas. The table below shows that the median of the average year-over-year asking rent growth in metro areas with population of over 1 million was 10.6% as of the 3-month rolling period ending September 7. Rents in metro areas with population sizes of over 500,000 to 1 million were growing at a slightly smaller pace of 10.4%, while metro areas with up to 250,000 had rent growth of 4% to 5%. Vacancy rates were tight across all market sizes although metros with 100,000 to 500,000 people had the lowest vacancy rates.

Among the top 10 metro areas with populations of over 1 million, five of the 10 metro areas with the strongest rent growth were in Florida, with rent growth of at least 20% (Palm Beach, Tampa, Orlando, Jacksonville, and Fort Lauderdale). In San Francisco, where rents fell the most by 11% in 2020, rents are now up 7% year-over-year. In New York, rents are also up 3.9% year-over-year.

Among the top 10 metro areas with a population of over 500,000 to 1 million, Florida again has 5 of the top 10 metros, with rent growth of 16% to 33% (Sarasota, Port St. Lucie, Fort Myers, Melbourne, Pensacola) as well as Daytona Beach and Lakeland.

Among the top 10 metro areas with population of over 250,000 to 500,000, Florida again has 3 of the top 10 metros, with rent growth of 14% to 37% (Naples, Fort Walton, Ocala).

Among the top 10 metro areas with population of 250,000 or less, Punta Gorda had the highest rent growth at 34%.

Overall, five Florida metros landed in the top 10 commercial markets with the strongest overall market conditions due to strong domestic migration, job growth, and generous tax incentives to attract high-tech businesses as discussed in a prior blog post.

Where is it Cheaper to Own than Rent?

Renting is an alternative to owning, so the decision to own or rent depends to a great extent on whether it is cheaper to own than to rent. The mortgage payment to rent ratio is one indicator of the comparative affordability of renting versus owning for households that are income-constrained or wealth-constrained with not enough savings to put down for a down payment. Owning has the great benefit of providing the owner with price appreciation gains that can offset the higher mortgage payment, but wealth-constrained renters won't have the down payment to buy a home and reap the price appreciation gains.

I compared the mortgage payment on a single-family home purchased at the median sales price as of 2021 Q2 with a 10% down payment to the monthly rent on an apartment unit. Because of the low mortgage rates and due to the steep growth in rents, the mortgage payment is higher than the average rent in 57 out of 179 metro areas. So, it is cheaper now to own in more metro areas (122 metros) than to rent.

The most expensive metro areas to own a home relative to renting are metro areas in California (San Jose, Orange County, San Diego, and Los Angeles). It's a toss-up in Sacramento, Fresno, and the Inland Empire, where owning is just slightly more expensive than renting. Other areas more expensive to own than rent are metro areas in the state of Washington (Seattle, Yakima) although it's a toss-up in Kennewick, where owning is just slightly more expensive than renting. It's also more expensive to own than rent in some metro areas in Colorado (Denver, Fort Collins), Oregon (Portland, Salem, Eugene), and the booming areas of Salt Lake City and Boise.

Outlook for Apartment Rent Growth

With home prices rising at double-digit pace and with some increase in mortgage rates in the offing, there is still pressure to rent than to own. Moreover, it is difficult for wealth-constrained renters to afford the down payment. Only about 30% of renter households can afford to put down a 3.5% percent down payment.

As earlier discussed, fewer apartments under construction compared to the pre-pandemic level will also push up rent growth.

Rents will also likely increase in the smaller metros and metros where rents have not yet increased at the rate that rents are rising in the large metro areas (over 1 million).

Builders are also focusing their attention the more expensive single-family rentals.

So, expect rents to remain elevated in the next 12 months, with rent growth hovering at 10%.